New Delhi: The analysis of India’s economy should not be constrained by the examination of a single unfavourable quarter, fluctuations in the rupee, or tariff announcements from Washington.

The Reserve Bank of India’s Annual Report for 2025-26 necessitates a more comprehensive approach: an acknowledgement of an economy that not only withstood one of the most challenging external environments in recent history but also experienced acceleration.

For those anticipating a decline in India’s economic trajectory, this report presents a challenging narrative.

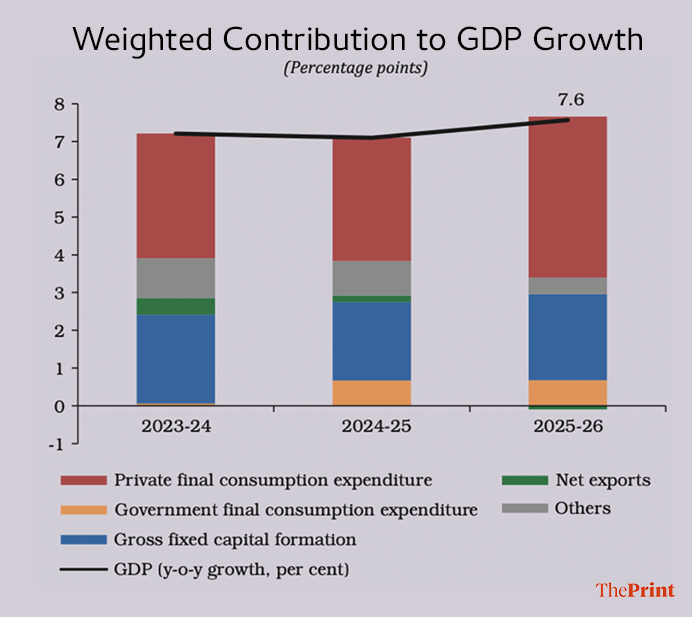

India achieved a real GDP growth rate of 7.6 percent in 2025-26, up from 7.1 percent the previous year, thereby maintaining its status as the fastest-growing major economy globally.

This chart illustrates the nature of the current economic growth: private final Consumption expenditure has increased to 7.7 percent, gross capital formation at 6.5 percent, services Gross Value Added (GVA) surging to 8.7 percent, and manufacturing GVA has achieved a remarkable 11.5 percent, marking its best performance in recent years.

This growth is not characterised by isolated economic expansion or government expenditure compensating for private sector weaknesses. Instead, it represents a broad-based, multi-faceted growth, akin to the models discussed in development economics literature.

This achievement is particularly noteworthy given the context of the year, an increase in geopolitical tensions from Ukraine to West Asia, and the IMF revising its 2026 global growth forecast downward to 3.1 percent, significantly below the long-term average of 3.7 percent.

Also Read: How budgets made investing in India unaffordable for middle-class savers

The inflation surprise nobody saw coming

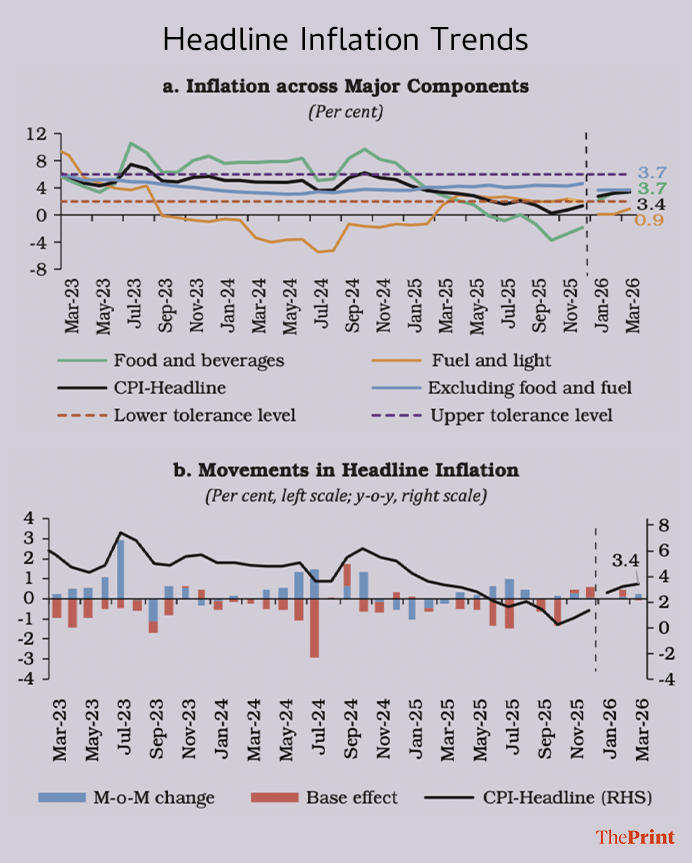

In the fiscal year 2025-26, the headline CPI inflation declined significantly to 2.1 percent, compared to 4.6 percent in the preceding year, approaching the lower threshold of the RBI’s inflation target range.

The chart’s panel (b) vividly illustrates a significant shift: a trend line that had persistently remained near or above 4 percent for several years experienced a marked decline. This outcome was influenced by food price deflation, a substantial base effect, softened global commodity prices, and, notably, an exceptionally favourable monsoon season.

The southwest monsoon arrived eight days earlier than anticipated in 2025, marking the earliest occurrence since 2009; reservoir levels reached a record high of 91.4 percent of full capacity by October; and total foodgrain and horticulture production achieved unprecedented levels across both the kharif and rabi seasons.

However, the analytically intriguing aspect is that the agricultural GVA still decelerated to 2.4 percent from 4.2 percent the previous year. Weather-related disruptions during the kharif season were sufficiently severe to suppress value-added, despite record-breaking production volumes.

The discrepancy between abundant harvests and subdued agricultural GVA is primarily a matter of pricing and procurement, rather than climate, and warrants significantly more policy attention than it currently receives.

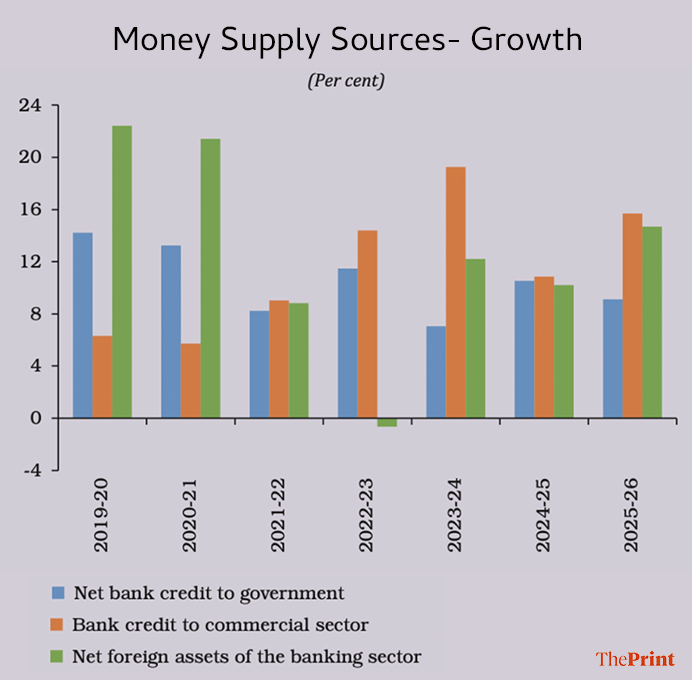

The Monetary Policy Committee (MPC) addressed the decline in inflation by reducing the repo rate by a total of 100 basis points. As a result, liquidity increased significantly, with the average daily net absorption under the Liquidity Adjustment Facility (LAF) rising to Rs. 1.86 lakh crore, compared to a mere Rs. 1,605 crore in the previous year.

This chart illustrates a 15.7 percent increase in bank credit to the commercial sector, indicating that the easing measures have effectively permeated the real economy rather than remaining confined within the financial system.

The quiet fiscal discipline that changed the story

The external sector experienced significant stress, as evidenced by 9.9 percent depreciation of the rupee against the dollar, an expansion of the merchandise trade deficit to US$ 333.2 billion, net FPI outflows amounting to US$ 16.5 billion, and a reduction in foreign exchange reserves by US$ 30.8 billion.

Nevertheless, the current account deficit was maintained at a modest 1 percent of GDP, and by the end of March 2026, reserves stood at US$ 691.1 billion, equivalent to approximately 11 months of import cover and covering 90.3 percent of external debt. India’s external vulnerability metrics remain among the most favourable within the emerging market context.

The fiscal narrative is where the report’s core argument is situated. The central government’s gross fiscal deficit was recorded at 4.4 percent of GDP, aligning with its consolidation target, while capital expenditure was sustained, and revenue expenditure controlled.

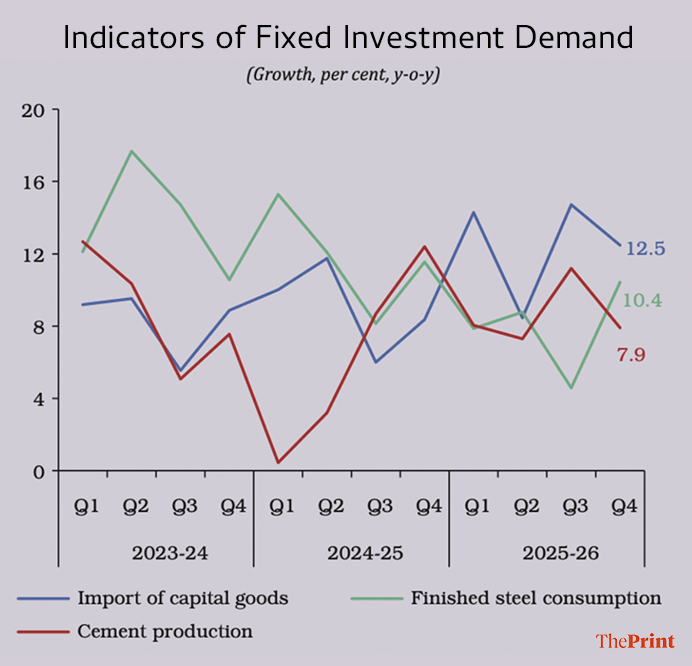

This chart shows that sustained public capital expenditure has facilitated an increase in private investment, rather than diminishing it. Direct taxes are projected to constitute 6.9 percent of GDP in the fiscal year 2026-27, marking the highest level in over a decade.

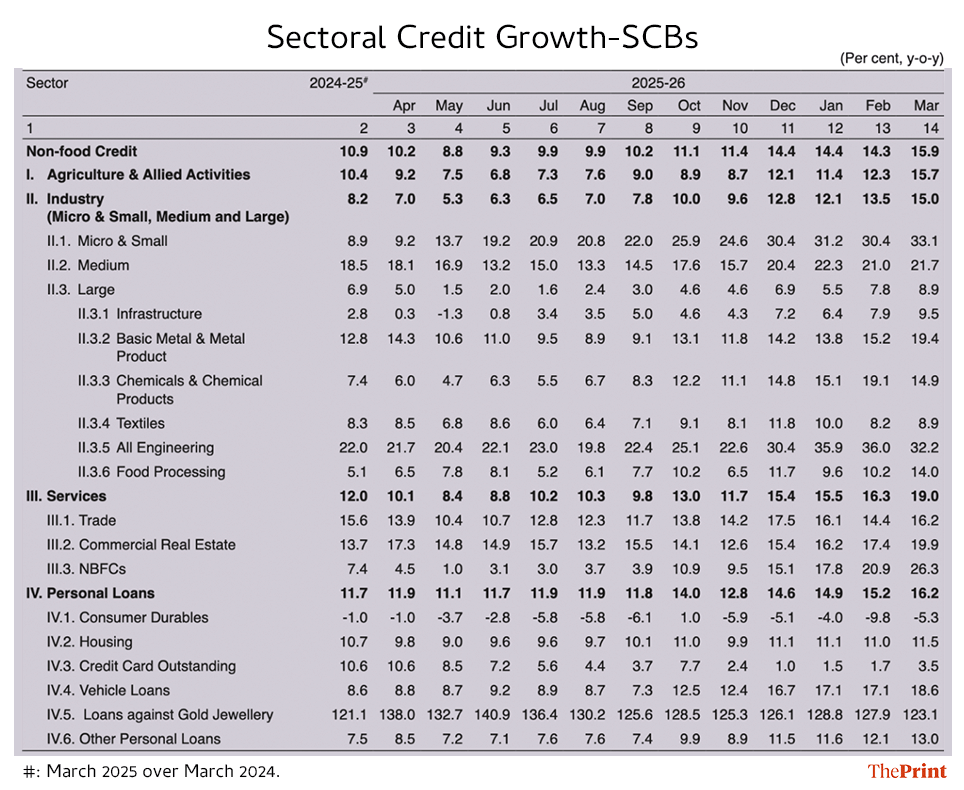

The sectoral credit growth data indicate that non-food credit has increased by 15.9 percent, with micro and small enterprises experiencing a substantial credit growth of 33.1 percent. This trend suggests that the financial system is effectively directing capital towards sectors with the highest employment multipliers.

Additionally, the gross NPA ratio has decreased to a multi-decadal low. A decade ago, the banking system was dismissed as a stagnant institution; however, it has now emerged as a driving force in India’s investment cycle.

The Reserve Bank of India (RBI) forecasts a growth rate of 6.9 percent for the fiscal year 2026-27, with potential risks predominantly oriented downward due to factors such as the conflict in West Asia, the possibility of an El Niño event, and volatility in trade policy.

Nevertheless, the report acknowledges that India’s agricultural vulnerability to rainfall fluctuations has diminished over time, attributed to increased irrigation intensity and advancements in farm-level technology.

The economy, which previously experienced significant disruptions due to monsoon delays, has evolved.

The MPC decision in April 2026 to maintain the repo rate at 5.25 percent, while adopting a neutral stance, remaining vigilant without being overly reactive, represents an appropriate strategy for a central bank operating in a global environment where geopolitical shocks, rather than monetary policy errors, have emerged as the primary sources of macroeconomic instability.

India continues to face substantial structural challenges: the agricultural GVA paradox highlights unresolved issues related to procurement and market access, while the dominance of the services sector, accounting for approximately 69 percent of real GVA growth raises pertinent questions regarding the employment benefits of the manufacturing sector.

However, a candid assessment of this report indicates that India is entering a period of heightened global uncertainty with more robust macroeconomic foundations than at any comparable point in the past three decades.

The banking sector is now stable, the fiscal framework is disciplined, and the inflation management system has been rigorously tested and proven effective. The current challenge is not to manage decline but to sustain economic acceleration and ensure that its benefits are distributed to those who have been waiting the longest.

This presents a more complex problem than pessimists have anticipated, yet it is, for the first time in a considerable period, a favourable challenge to confront.

Also Read: The rupee does not need a defender. It needs an economy worth defending