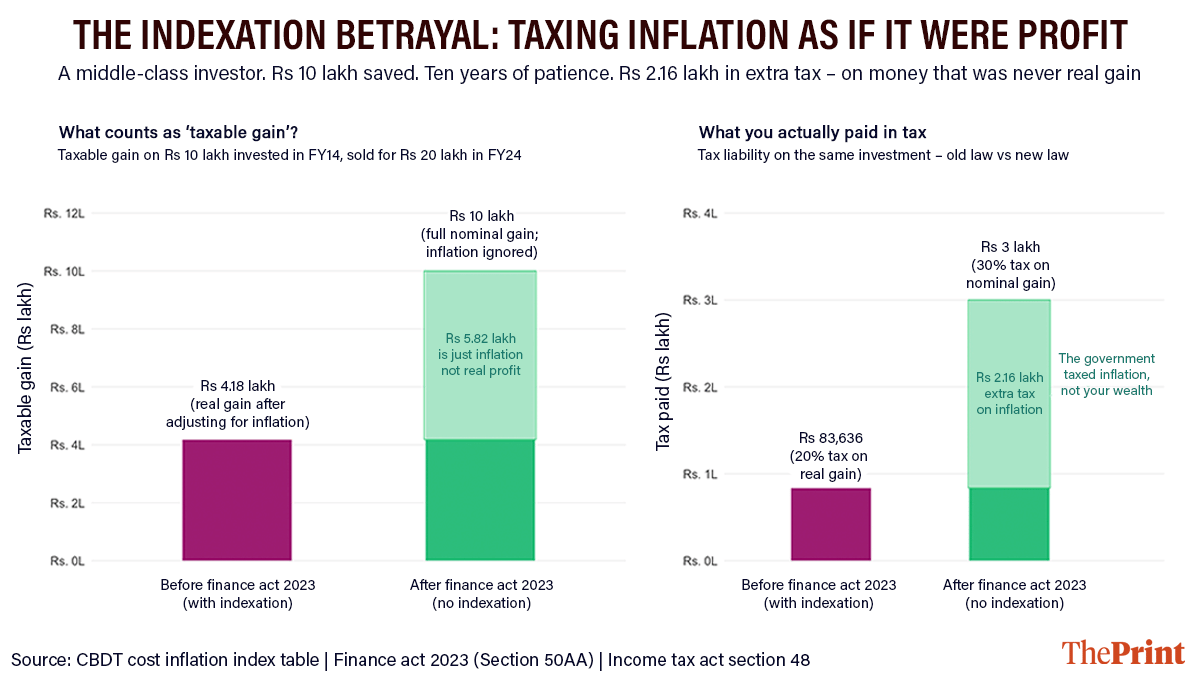

Consider the case of a schoolteacher in Pune. In 2013, she adhered to the advice of financial advisers, government campaigns, and the mutual fund advertisements by investing Rs 10 lakh of diligently saved funds into a debt mutual fund. She maintained this investment for a decade. In 2023, she liquidated it for Rs 20 lakh, believing she had doubled her initial capital.

However, this was not the case.

Inflation over the 10-year period had eroded Rs 5.82 lakh of the apparent gain. Her actual profit—the amount by which her wealth had genuinely increased—was Rs 4.18 lakh. Under the legal framework in place at the time of her investment, she would have been liable to pay tax on this real gain, amounting to Rs 83,636.

However, the Finance Act 2023, which eliminated the indexation benefit that protected investors from taxation on inflation, required her to pay a tax of 30 per cent on the entire nominal gain of Rs 10 lakh, totalling Rs 3 lakh. The discrepancy, Rs 2,16,364, is not a tax on profit, but rather a tax on the inevitable rise in prices during the investment period.

This situation is not an isolated instance of injustice; it rather represents the culmination of a 20-year policy trajectory in which each successive budget identified new aspects of the investor’s financial ladder to tax, with the ratchet mechanism operating unidirectionally.

How this is calculated — using the government’s own Cost Inflation Index (CII), notified by CBDT:

Investment: Rs 10 lakh in FY 2013-14 | Sale: Rs 20 lakh in FY 2023-24 | Nominal gain: Rs 10 lakh

CII in FY 2013-14 = 220 | CII in FY 2023-24 = 348 | Inflation-adjusted cost = Rs 10 lakh x (348/220) = Rs 15.82 lakh

Real gain after indexation = Rs 20 lakh – Rs 15,82 lakh = Rs 4.18 lakh | Tax OLD (20% with indexation) = Rs 83,636

Tax NEW (30% slab rate, no indexation) = Rs 3 lakh | Extra tax on inflation = Rs 2,16,364

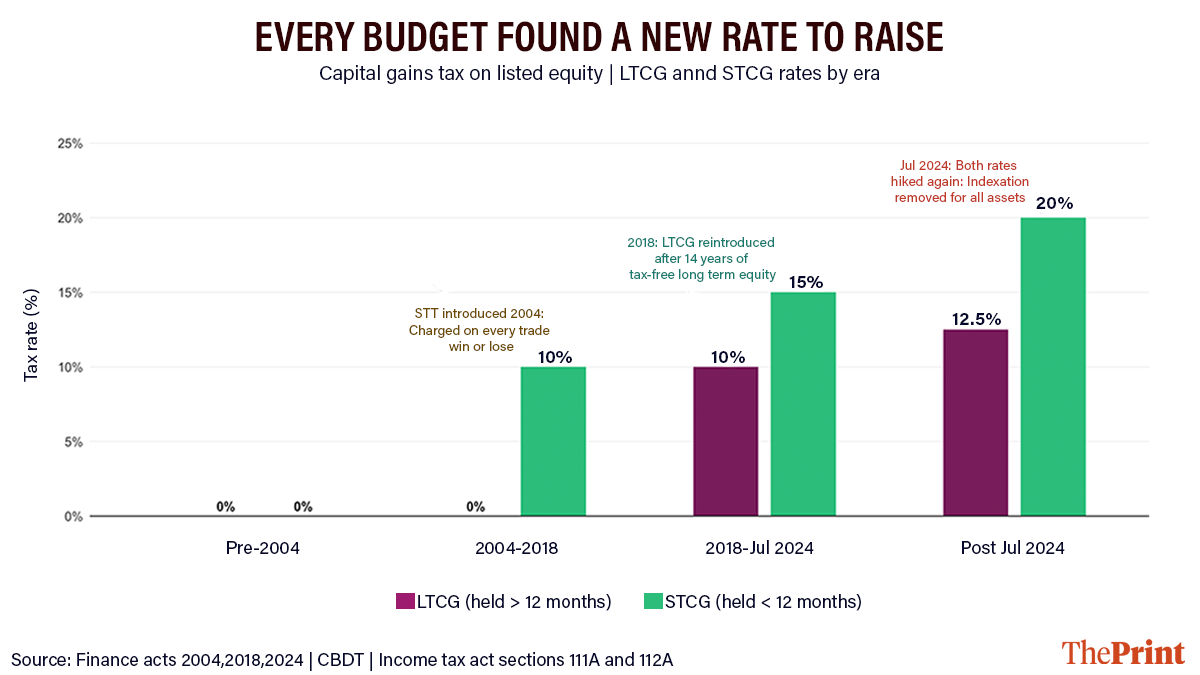

How every budget found a new rate to raise

Prior to 2004, long-term capital gains on listed equities were exempt from taxation. The government’s message to the middle class was unequivocal: embrace risk, invest in enterprises, and engage in India’s economic growth. In 2004, the Securities Transaction Tax (STT) was introduced—a minor procedural change, yet one that embodied a principle with potentially detrimental effects.

The STT was levied irrespective of whether profits were realised or losses incurred, akin to a toll that charged every vehicle equally, regardless of destination. For the next 14 years, investors were reassured that gains from long-term equity holdings would remain untaxed. This assurance was disrupted in 2018, when the budget reinstated a 10 per cent tax on long-term capital gains. By July 2024, these rates were further increased: long-term gains were taxed at 12.5 per cent and short-term gains, 20 per cent. At the same time, indexation benefits were removed from most asset classes. The progression of these changes never once turned back.

What these rate changes mean for a middle-class investor:

Pre-2004: Zero tax on both short and long-term equity gains. Government signal — invest, take risk, participate in growth.

2004: STT introduced. A small tax on every transaction regardless of profit or loss. You lose money? You still pay STT.

2018: LTCG reintroduced at 10% after 14 years of exemption. The promise of tax-free long-term investing — broken.

Grandfathering clause protected gains up to Jan 31, 2018 only.

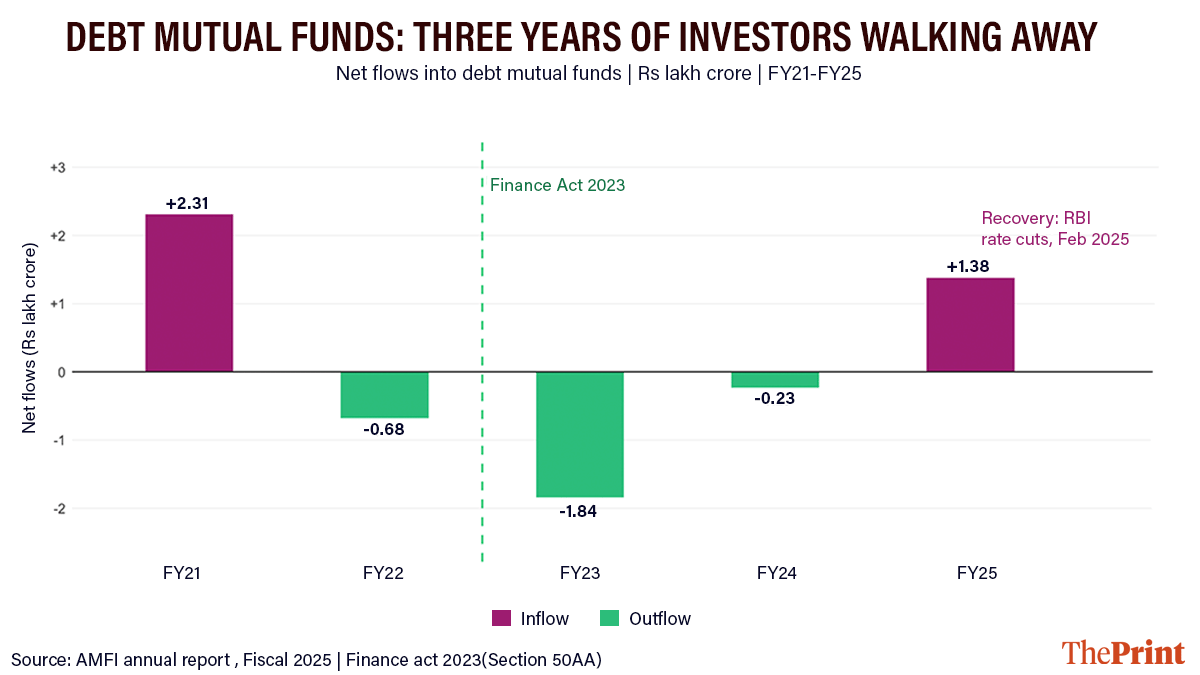

The debt market exhibited a similar, although more pronounced, narrative. Before April 2023, a patient debt fund investor could hold investments for three years, adjust for inflation through indexation, and incur a 20 per cent tax on the real gain. The Finance Act 2023 ended this overnight, by introducing Section 50AA to the Income Tax Act. All gains from debt funds acquired after 1 April 2023 became taxable at the investor’s income slab rate, up to 30 per cent, irrespective of the holding period.

As a result, the instrument became, in tax terms, equivalent to a bank fixed deposit, a kind that is prone to market risk. Investors responded accordingly: they withdrew investments. Net outflows from debt mutual funds amounted to Rs 2.75 lakh crore across FY22, FY23, and FY24. In FY23 alone, Rs 1.84 lakh crore was withdrawn, marking the most significant single-year outflow on record. The modest recovery in FY25 was not attributable to any policy reversal but rather to the Reserve Bank of India’s rate cuts in February 2025, which temporarily enhanced the attractiveness of debt investments despite the onerous tax implications.

What Finance Act 2023 did — and why it matters:

Debt mutual funds taxed at the investor’s income tax slab rate (up to 30%), regardless of holding period. This made debt funds identical to bank FDs in tax terms — but FDs carry no market risk. Rational investors left.

Indexation benefit removed: previously, investors could adjust their purchase price for inflation before computing taxable gain. A real gain of Rs. 42,000 could now be taxed as Rs. 1,00,000 in nominal terms.

Also read: Households are saving less and borrowing more, but that’s not necessarily a bad thing

What the money did instead

The implications extend significantly beyond any singular asset class. According to the RBI Handbook of Statistics on the Indian Economy, the gross household financial savings as a percentage of GDP declined from 11 per cent in FY21 to 5.3 per cent in FY24, effectively halving over three years. As of FY24, Indian households allocated 71.5 per cent of their savings to physical assets such as gold, real estate, and land, while only 28.5 per cent were invested in financial assets. Of that 28.5 per cent, a mere 8.4 per cent was directed toward mutual funds.

The ratio of India’s mutual fund assets under management (AUM) to GDP is 19.9 per cent, in contrast to a global average that, in developed markets, surpasses 100 per cent. Each percentage point of this disparity signifies capital being invested in gold and real estate rather than being utilised to fund enterprises, enhance bond markets, and contribute to retirement security for the families that saved it.

The concept of tax elasticity of savings is well established in the field of public finance. It refers to the degree of sensitivity with which households modify their saving and investment behaviours in response to variations in anticipated after-tax returns. India’s middle class exhibits high elasticity and rationality. When priced out of debt funds, they revert to fixed deposits. When indexation is removed, they realise that gold has never necessitated filing a capital gains return. When equity gains become costly, they reconsider venturing beyond the security of bank branches.

The government has spent two decades making productive financial investing more expensive, while also expressing concern over the low retail participation in capital markets. The situation is not paradoxical; it is a clear instance of cause and effect.

Also read: India spooks investors instead of calming them

The case for turning the ratchet back

The path forward is neither enigmatic nor revolutionary. It requires that the government candidly address a question it has persistently evaded: what is the cost of each capital gains amendment in terms of foregone investment, underdeveloped bond markets, and unfunded enterprises? The responses unequivocally suggest the need to reinstate meaningful indexation for long-term investors and rationalise debt fund taxation to accurately reflect the risks borne by investors. They also demand the acknowledgement that the STT, the LTCG tax, the dividend tax, and the slab-rate treatment of bonds are not isolated decisions but rather cumulative layers of friction affecting the same middle-class saver. While each measure may be defensible in isolation, collectively, they form a system that penalises patience, incentivises passivity, and diverts India’s household savings away from the productive economy.

India’s demographic dividend also represents a potential savings dividend awaiting to be unlocked. In a global context characterised by conflict in the Middle East, uncertainty regarding US interest rates, and disruptions in international trade, India’s inability to effectively channel its domestic household savings into productive financial assets renders it perpetually susceptible to economic vulnerabilities. A nation where households voluntarily transition funds from gold to bond markets, from fixed deposits into equity, and from physical assets to financial ones is a nation capable of financing its own growth without reliance on foreign capital, which can be withdrawn abruptly. Such a nation is entirely attainable.

The forthcoming Budget does not require a comprehensive new framework; rather, it requires the honesty to acknowledge that incremental policy adjustments over two decades have culminated in an unintended outcome that is now measurable by all.

The schoolteacher in Pune saved diligently, invested patiently, and waited for a decade. The least the Budget can do is meet her halfway.

Bidisha Bhattacharya is ThePrint Consulting Editor (Economics) and an Associate Fellow, Chintan Research Foundation. She tweets @Bidishabh. Views are personal.

(Edited by Prasanna Bachchhav)

Unfortunately middle class don’t form a vote bank.

Earning money through financial instruments apart from FD is still considered as gamble and a sin in this country. Hence the sin tax!

Kudos to theprint and Ms Bidisha Bhattacharya. What a incisive analysis. This is called journalistic excellence. Iam very sure at the very financial helm of affairs, this article has raised eyebrows and constraints. Hopefully, remedial measures will be implemented once major ongoing external crisis gets over. Thank you Ms Bhattacharya, for the pointer.