")

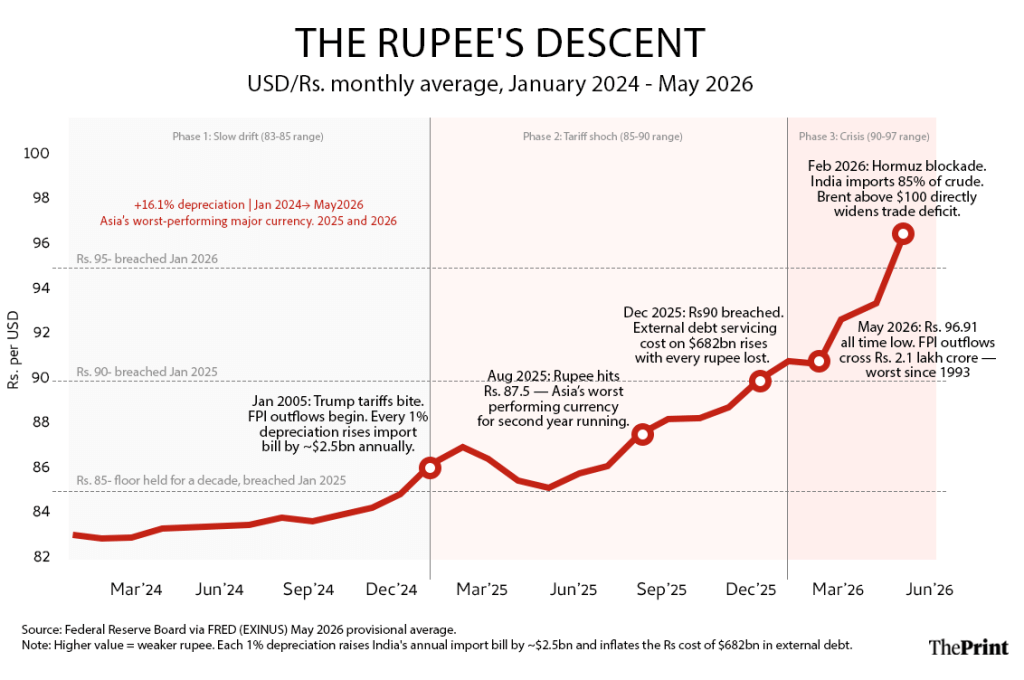

The rupee reached a value of 96.91 against the dollar on 20 May, marking a 16.1 per cent depreciation over 18 months, thereby rendering it Asia’s worst-performing major currency for two consecutive years. The underlying causes of this phenomenon are now well understood.

Gita Gopinath recently explained that the rupee should be allowed to function as a shock absorber and that intervention is counterproductive. Her assertion is valid. However, the efficacy of a shock absorber is contingent upon the robustness of the vehicle in which it is installed. The more important question, one that this analysis seeks to address, is not the current state of the rupee, but rather what structural measures India must implement so that the rupee never finds itself in this situation ever again.

A close examination of the intervention data reveals that India’s foreign exchange reserves peaked at $728 billion in February this year. It now stands at $692 billion. The Reserve Bank of India (RBI) had expended more than $30 billion in three months in an attempt to stabilise the rupee, yet the currency still reached an unprecedented low of Rs 96.91. This is not a critique of the RBI; rather, it illustrates a fundamental truth: structural issues cannot be resolved through intervention alone. The $30 billion spent to slow down the depreciation did not address why the decline was happening in the first place.

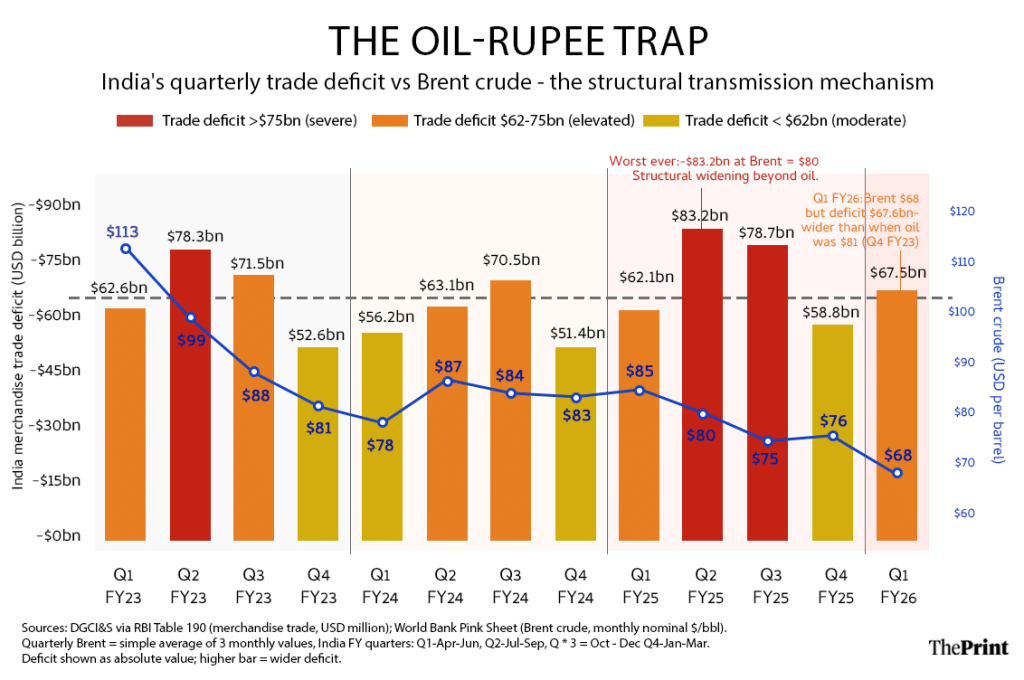

The data indicate that India’s quarterly trade deficit reached its highest level, $83.2 billion, in the second quarter of the Financial Year (FY) 2024-2025, despite Brent crude averaging just $80 per barrel. In the first quarter of FY23, with oil priced at $113 per barrel, the deficit was a comparatively modest $62.6 billion. The oil-rupee conundrum has intensified even as oil prices have moderated. India’s trade deficit has structurally expanded beyond the crude oil cycle, driven by escalating imports of electronics, gold, and capital goods, which have increased at a faster rate than merchandise exports. This situation is not an external shock but rather an architectural failure.

Funding model that must change

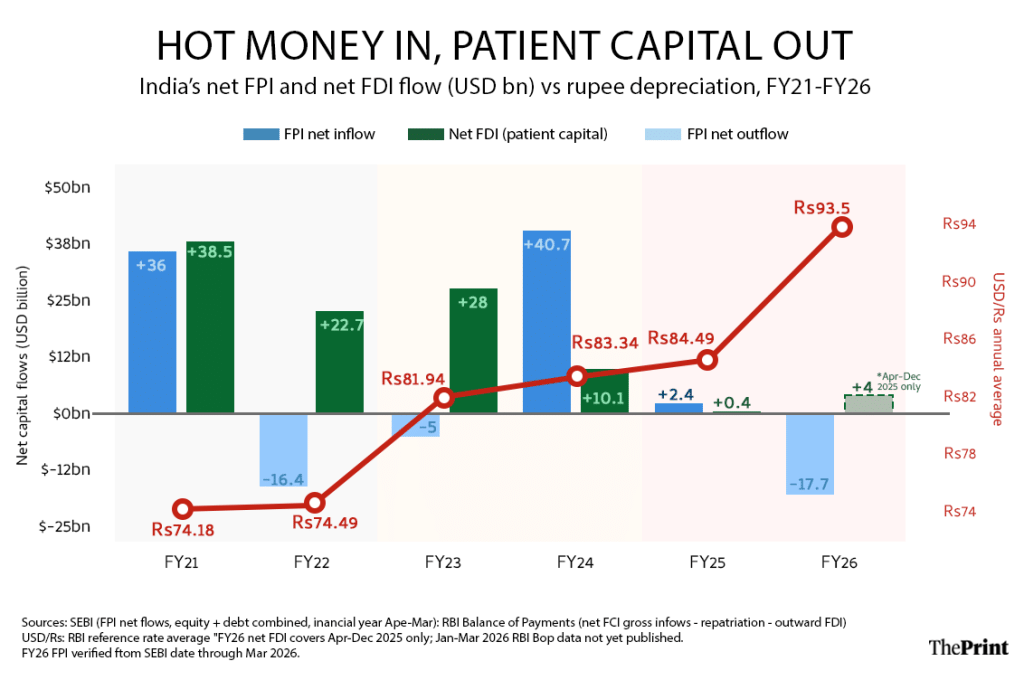

Before prescribing, it is essential to accurately comprehend the underlying issues. In FY21, India’s external account was supported by two strong pillars: Foreign Portfolio Investment (FPI) inflows amounting to $36 billion and net Foreign Direct Investment (FDI) of approximately $38-39 billion. Together, patient capital and portfolio capital not only financed the deficit but also provided a surplus.

By FY24, a significant and potentially hazardous shift had occurred in India’s capital inflows. FPI had escalated to $40.7 billion, driven by enthusiasm surrounding index inclusion, while net FDI had plummeted to a mere $10.1 billion. This shift replaced stable, productive capital with volatile, sentiment-driven flows that were susceptible to rapid reversal.

Indeed, by FY26, FPI experienced a net outflow of $17.7 billion, marking the most substantial withdrawal since India opened to foreign portfolio investors in 1993. Notably, March 2026 alone witnessed outflows amounting to Rs 1.26 lakh crore. At the same time, net FDI had dwindled to a negligible $0.4 billion in FY25.

This substitution, characterised by the influx of transient capital and the exodus of patient capital, constitutes a central structural vulnerability that future policy initiatives must address. The good news is that this issue is addressable. India remains an attractive destination for long-term capital. However, its unpredictability poses a challenge. This challenge is resolvable, contingent upon the presence of political will.

Regarding the RBI intervention, a nuanced approach is imperative. The RBI spent $30 billion between February and May, yet the rupee continued to depreciate. The lesson is not to stop managing the exchange rate altogether, but to recognise that opaque, reactive interventions lacking a structural foundation are both costly and ineffective.

A constructive path forward involves establishing a transparent, rules-based intervention framework that clearly communicates the RBI’s actions and rationale. Countries such as Chile, Brazil, and Indonesia have demonstrated that credible communication of intervention objectives, aimed at preventing disorderly market conditions rather than targeting specific exchange rate levels, can coexist with genuine exchange rate flexibility while mitigating speculative pressures.

India’s substantial reserves amounting to $692 billion, even after the recent drawdown, provide the necessary resources. The next step is to develop a robust framework and to refrain from depleting reserves on issues that cannot be resolved by reserves alone.

Also read: RBI’s defence of the rupee has its limits. Tough calls may lie ahead

3 decisions India cannot postpone

The future trajectory of the Indian rupee is contingent upon three pivotal structural decisions that policymakers in India have postponed for an extended period.

The first decision involves a national commitment to rectifying the current account. India must establish a formal, public objective to reduce its goods trade deficit as a proportion of GDP. This should not be achieved through import restrictions, which are counterproductive and may provoke retaliatory measures, but rather through an export-driven approach in manufacturing that mirrors the ambition of the 1991 economic reforms.

The Production-Linked Incentive (PLI) represents an initial step, not a comprehensive strategy. The critical question that must be addressed at the highest echelons of government is straightforward yet challenging: what products can India manufacture that are in demand globally at scale, and what measures are necessary to increase their production? Until this question is credibly answered, the rupee will remain structurally vulnerable to fluctuations in commodity cycles and shifts in global financial sentiment.

The second decision concerns restructuring the external financing framework to prioritise FDI over FPI. This is fundamentally a governance issue rather than a regulatory one. Every instance of retrospective taxation, abrupt sector-specific policy reversals, and regulatory shocks that disadvantage foreign investors contributes to a risk premium on India’s cost of capital, which is subtly and persistently reflected in the exchange rate. India cannot maintain an unpredictable policy environment while ensuring currency stability.

The forthcoming budget and regulatory decisions should be assessed not only for their domestic implications but also for the message they convey to the $10-15 billion in annual net FDI that India requires to structurally replace the volatile capital it is losing.

The third decision involves providing the RBI with a clearer mandate and a more transparent framework for exchange rate management. While setting a target is not advisable, a published set of intervention principles that markets can anticipate, coupled with a long-term commitment to developing domestic bond and derivatives markets, is essential. These markets would enable Indian companies and investors to hedge currency risk efficiently.

A more robust onshore hedging market would mitigate the rupee’s susceptibility to FPI fluctuations by equipping domestic participants with the tools to absorb external volatility without directly impacting the spot rate. Although this decision is the least glamorous and the most technically challenging, it holds the potential for the most enduring long-term impact.

The rupee’s latest valuation is not the end of the story, as India’s economic fundamentals remain robust. However, each additional percentage point of depreciation increases the import bill, fuels inflation, increases the rupee-denominated cost of $682 billion in external debt, and constrains the RBI’s capacity to reduce interest rates when the economy most requires it.

The global context may yet offer a respite, potentially through an agreement with Iran, a de-escalation in the Strait of Hormuz, or a Federal Reserve that identifies opportunities to lower rates. The critical question is whether India will utilise this opportunity to strengthen its economic framework or merely revert to the status quo that precipitated the current crisis.

The RBI has expended $30 billion over three months, reaffirming a principle well-established in structural economics: intervention provides temporary reprieve but does not ensure long-term stability. This period must now be leveraged, not to defend the rupee, but to reconstruct the economy that underpins it.

The rupee does not need a defender; it needs an economy worthy of defending.

Bidisha Bhattacharya is ThePrint Consulting Editor (Economics) and an Associate Fellow, Chintan Research Foundation. She tweets @Bidishabh. Views are personal.

(Edited by Saptak Datta)

Support MSMEs in creating goods for local consumption.

Create a group of experts to study the economies and social structures of countries we have signed an FTA with (per country).

Exploit this knowledge and inform local companies to create these goods for export.

The Indian govt. should subsidies and prioritise small companies by providing logistical support for export.

Break monopolies up in any sector to boost confidence of businessmen. To ensure everyone has a chance and they invest in industries.

Use these same MSMEs and local companies to produce most goods India needs instead of importing. We have a lot of people here there is no need to hand off work to foreigners.

Invest in R&D of new and renewable sources of energy which doesn’t need to be imported.

Invest in R&D of dual use technologies.

A speculative cabal assembled a war chest of $ 10 billion and attacked the Thai baht, because they felt it was overvalued in relation to fundamentals. Setting off the 1997 Asian financial crisis. Malaysian PM Mahathir Mohamed blamed George Soros for his country’s economic troubles. 2. I doubt if there is a speculative group attacking the Indian Rupee. However, if the RBI starts flaring forex reserves to protect it, expect short sellers to get active.