Last month, I wrote that the incoming Congress government in Kerala would encounter “the most structurally challenging legacy” among the three states that had recently undergone a change in administration. This challenge pertains to a productive structure whose welfare obligations have long surpassed its capacity for revenue generation. While I had the relevant data to draw this conclusion, I lacked specific numerical details. Now, I have access to several pertinent figures, with one in particular warranting significant attention. No, it’s not the headline debt figure.

And with Chief Minister VD Satheesan set to present his first Budget on 19 June, all eyes are on the UDF government.

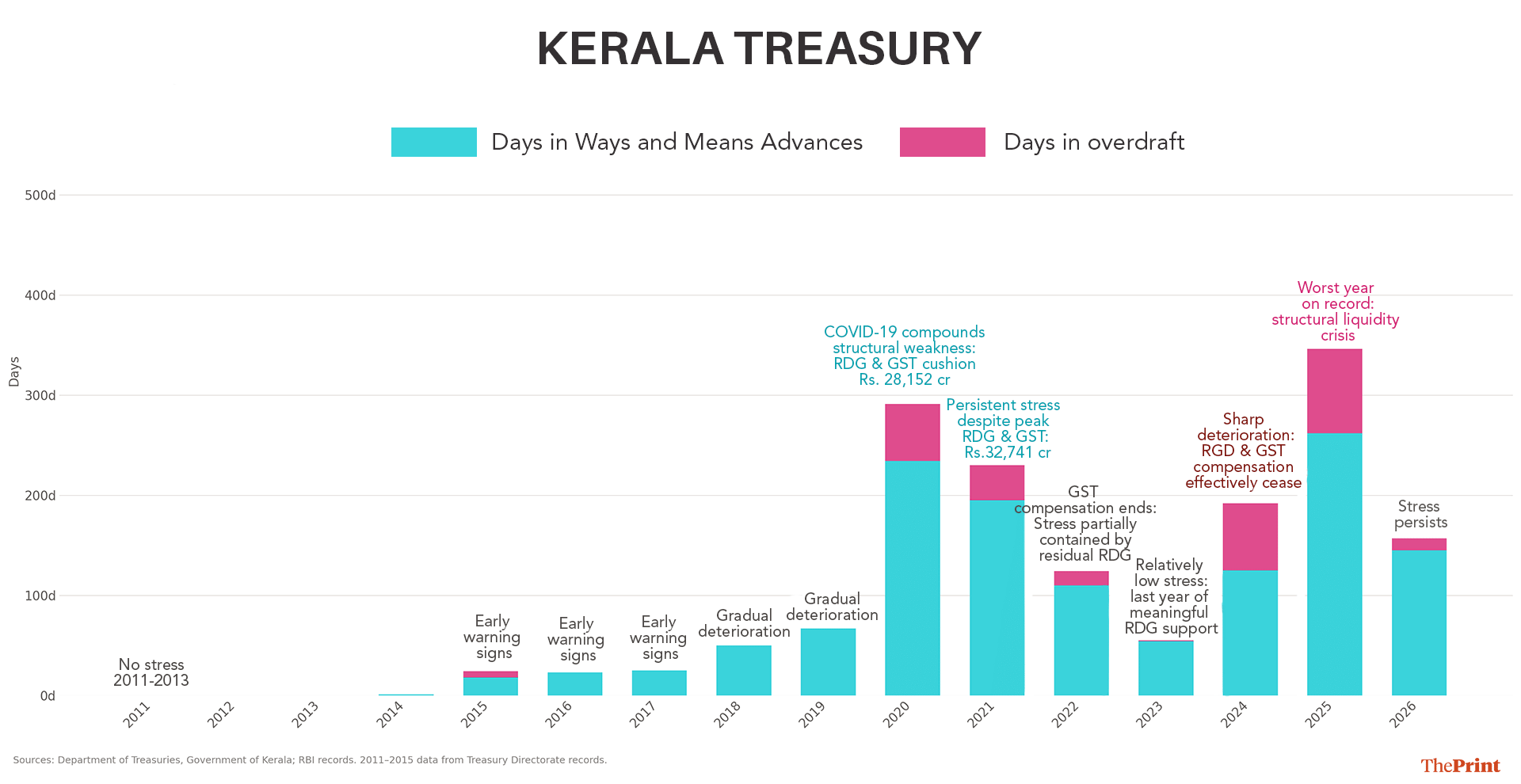

According to its report, “Kerala’s Fiscal Health: A Status Report,” the state’s outstanding liabilities amount to Rs 5.07 lakh crore. Although this figure has dominated media coverage, it should not be the primary concern for economists. The critical figure is as follows: In 2025, Kerala engaged in borrowing from the Reserve Bank of India under the Ways and Means Advances for 262 days and was in outright overdraft for 84 days—a total of 346 days. Given that there are 365 days in a year, the state was, by any reasonable definition, cash-insolvent for the majority of the year. This situation resulted in the state incurring interest rates ranging from 7.25 per cent to 10.25 per cent per annum, in addition to the interest already embedded in its market borrowings.

When the borrower can’t stop borrowing

To understand the implications of this, one must consider a fundamental concept in public finance: The Domar condition. Named after the economist Evsey Domar, this condition posits that a government’s debt remains sustainable only if the economic growth rate surpasses the effective interest rate on its borrowings. When this condition is met, the economy expands sufficiently to generate revenues that adequately service the debt. Conversely, if borrowing costs exceed growth, the debt accumulates more rapidly than the capacity to repay it.

Kerala exemplifies a severe failure of the Domar condition. The state is not only borrowing at rates that surpass its growth but is also primarily borrowing to finance consumption, such as salaries, pensions, and increasingly, interest on existing debt, rather than investing in productive assets that would foster the necessary growth to service the debt. The debt is essentially self-consuming.

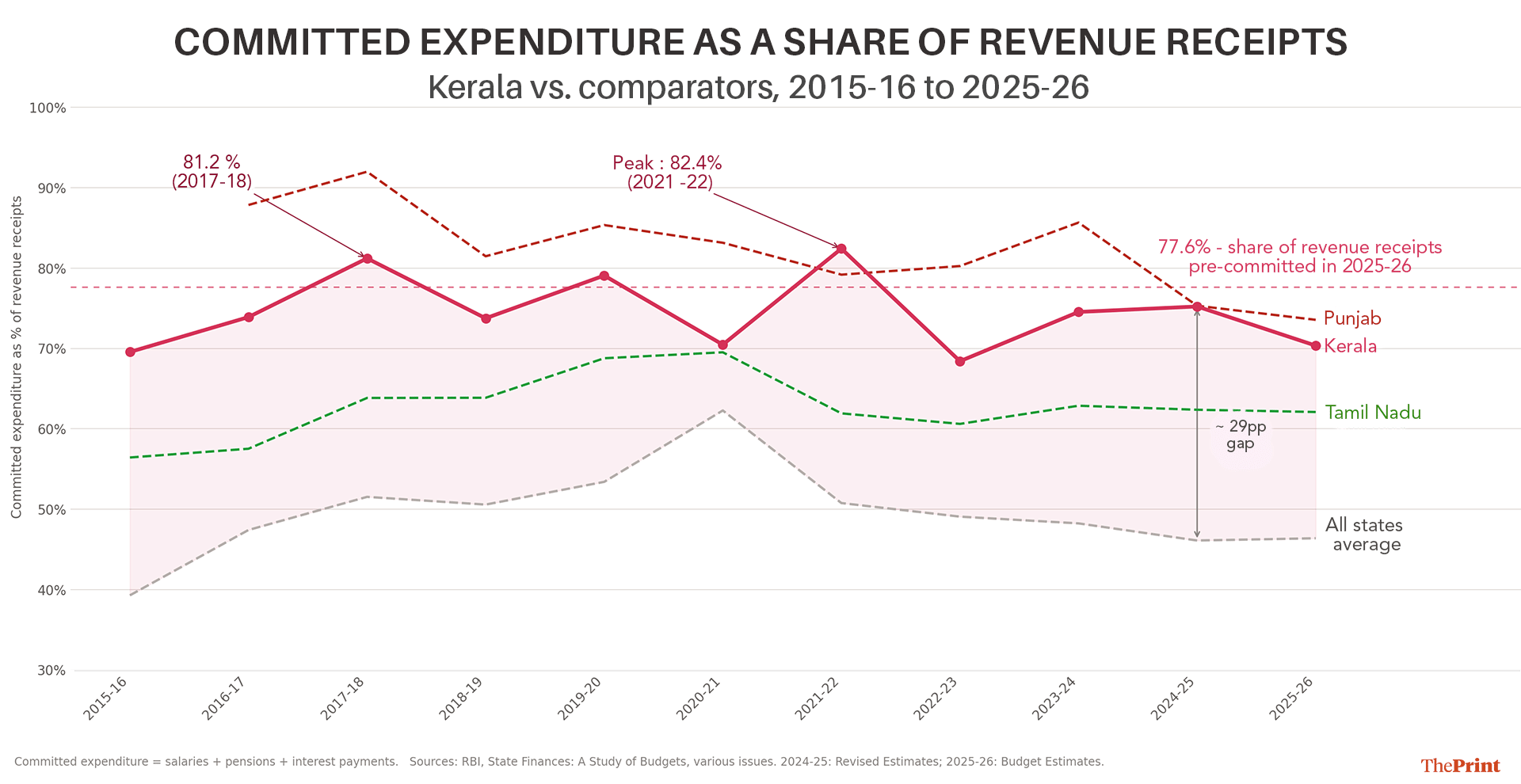

The data clearly illustrates that for every Rs 100 in revenue received by Kerala, Rs 77.60 is allocated to pre-committed expenses such as salaries, pensions, and interest payments, prior to any discretionary decisions. In contrast, the average pre-committed expense for all states is Rs 46. This 30 percentage point disparity has remained consistent over the past decade, irrespective of economic conditions, governmental changes, or Finance Commission awards, and has never been bridged.

Within this 77.6 per cent, the most concerning element is not salaries, which have decreased as a proportion of revenue receipts from 34.5 per cent in 2015-16 to 30.1 per cent in 2025-26. Rather, it is the interest payments. That has increased from 16.1 per cent to 20.9 per cent over the same period, while the average for major states has remained stable between 11 and 12 per cent. The gap between Kerala and the national average for interest payments alone has more than doubled, from 4.3 percentage points in 2015-16 to 8.5 percentage points in 2025-26.

The white paper succinctly states: “Every year of large open market borrowing adds permanently to the interest obligation in subsequent years. This is the mechanism through which today’s borrowing becomes tomorrow’s committed expenditure—and tomorrow’s committed expenditure becomes the next year’s treasury stress. The consequence is a government with almost no room to govern. The Rs 23 left in every Rs 100 after committed expenditure must cover the entire range of public services.” This statement does not constitute fiscal commentary; rather, it describes the functioning of a debt trap.

Also read: There’s a problem with UP’s trillion-dollar economy dream

The cushion that was hiding the crisis

Overlaying the WMA data reveals significant trends in Kerala’s treasury management. From 2011 to 2013, the treasury was entirely self-sufficient, requiring no support from the RBI. However, by 2019, the state was under WMA for 67 days, increasing to 262 days by 2025.

This deterioration was not linear; it was interrupted by a period of apparent improvement between 2020 and 2023. This period is crucial to understanding the situation.

During these years, Kerala received Rs 48,388 crore in Revenue Deficit Grants and Rs 28,813 crore in GST compensation from the Centre, totalling Rs 77,201 crore. Despite this substantial support, Kerala still spent 234 days under WMA in 2020-21, indicating that the transfers were not resolving the underlying issue but merely concealing it. The discontinuation of all categories of post-devolution revenue deficit grants by the 16 th Finance Commission, which amounted to Rs 37,814 crore received under the 15th FC over five years, exposed the true extent of the problem.

The 262 days under WMA in 2025 reflect the underlying fiscal structure without central support. This situation does not represent a new crisis, but rather the unmasked continuation of an existing one.

Also read: Growth, inflation & the gaps in between: What latest RBI annual report says about where India stands

KIIFB and the off-budget illusion

KIIFB, the Kerala Infrastructure Investment Fund Board, initially lauded as an exemplar of innovative federalism, deserves a paragraph of its own. Established to facilitate infrastructure investment beyond the conventional budget and borrowing limits, it aimed to address the capital expenditure shortfall caused by the burden of committed expenditures. The concept was theoretically sound: If budgetary investment is unfeasible, establish an alternative mechanism.

However, the white paper indicates that KIIFB has accrued Rs 56,000 crore in total obligations, comprising Rs 21,000 crore in unmet loan liabilities and Rs 35,000 crore in pipeline project commitments, with the productivity returns on these investments remaining unverified.

This approach did not resolve the Domar problem; rather, it worsened it off-budget. The LDF may challenge the white paper’s portrayal, and they are politically justified in doing so.

Nonetheless, the 262-day figure is sourced from the RBI, as is the interest payment trajectory from the RBI’s State Finances publication. The Domar arithmetic remains unaffected by the ruling party.

The Satheesan government faces a more challenging task than merely commissioning an honest assessment; it must govern contrary to four decades of political-economic trends. Kerala’s constituencies have been built on the implicit assurance of continued state commitments. The white paper, with technical precision, asserts that the mathematics underpinning this assurance is unsustainable.

Each year corrective measures are postponed, the interest burden increases, the share of committed expenditure rises, and the days of borrowing from the RBI to meet payroll obligations lengthen.

The solution to this problem has always been industrial deepening, and the opportunity to achieve this cost-effectively was during the decade Kerala did not pursue it. Between 2015 and 2023, when Revenue Deficit Grants and GST compensation were abundant, the state had a fiscal respite readily available. This was the opportune moment to utilise borrowed funds for their sole legitimate long-term purpose: Constructing a productive base whose tax returns would eventually render the borrowing self-liquidating.

Tamil Nadu did exactly this, with its secondary sector contributing over 30 per cent of Gross Value Added, and manufacturing consistently exceeding 20 per cent, generating tax buoyancy and private investment multipliers that maintained debt serviceability despite comparable welfare commitments. In contrast, Kerala’s manufacturing share has barely surpassed 13 per cent even in its best recent year. The transfers were received and expended, yet the underlying structure remained unchanged.

The white paper documents not merely a fiscal crisis but the fiscal outcome of a thirty-year industrial policy failure. Unlike interest payments, this is not a liability that can be refinanced.

The data foreshadowed this development, confirmed by the RBI, one overdraft day at a time. The white paper has now formalised it. The question is not whether Kerala faces a fiscal crisis; that has been established. The pertinent question is whether the government that identified the crisis possesses the resolve to resolve it.

Bidisha Bhattacharya is ThePrint Consulting Editor (Economics) and an Associate Fellow, Chintan Research Foundation. She tweets @Bidishabh. Views are personal.

(Edited by Theres Sudeep)