Glacial economic reforms, fragile banking sector, rigid labor laws and a spotty educational system are holding India back.

The world’s fastest growing major economy isn’t growing nearly fast enough.

That may seem like an absurd description for India, an economy the International Monetary Fund expects to expand 7.3 per cent in the fiscal year through March 2019 and 7.5 per cent in the next. Yet the reality is that even at its current pace, India is having trouble creating enough new jobs for its massive workforce or enough wealth to broaden its middle class.

With its demographic tailwind and massive developmental needs, Asia’s third-biggest economy should be growing at double-digit rates. Holding India back are glacial economic reforms, a fragile banking sector, rigid labor laws and a spotty educational system that imparts limited skills to the 12 million young people who enter the job market each year.

Prime Minister Narendra Modi is trying to address these challenges. He’s introduced a nationwide consumption tax, an insolvency code for companies and a program to boost domestic manufacturing under his signature Make in India campaign.

Yet analysts generally agree that more needs to be done to open up the economy, attract foreign capital and generate the kind of wealth and business opportunities that has broadened the middle class in China, whose $12.2 trillion economy is more than four times as big as India’s ($2.6 trillion).

Underachiever

“It hasn’t embraced global trade and foreign direct investments in the way China aggressively succeeded,” said Jim O’Neill, a former Goldman Sachs Asset Management chair and ex-commercial secretary to the U.K. Treasury and who coined the acronym BRIC in 2001 to describe Brazil, Russia, India and China as a group.

“India has created big wealth for a limited number of people at the highest income levels, but it hasn’t created a massive pool of consumers by creating hundred of millions of middle income class,” he said.

India’s economy has averaged 7 per cent growth since its reforms began in 1991 under Prime Minister P.V. Narasimha Rao. China, by contrast, expanded by an average of almost 10 per cent each year since its economic opening and modernization started some 40 years ago.

The latest pulse check for India’s economy comes Friday. Economists forecast gross domestic product expanded 7.6 per cent in the three months through June from a year earlier. Ahead of the data, India’s rupee dropped below 71 to a U.S. dollar, a new low that could possibly deter foreign investors, fan imported inflation and prompt intervention from the central bank – all having implications on growth in coming months.

Jobs Challenge

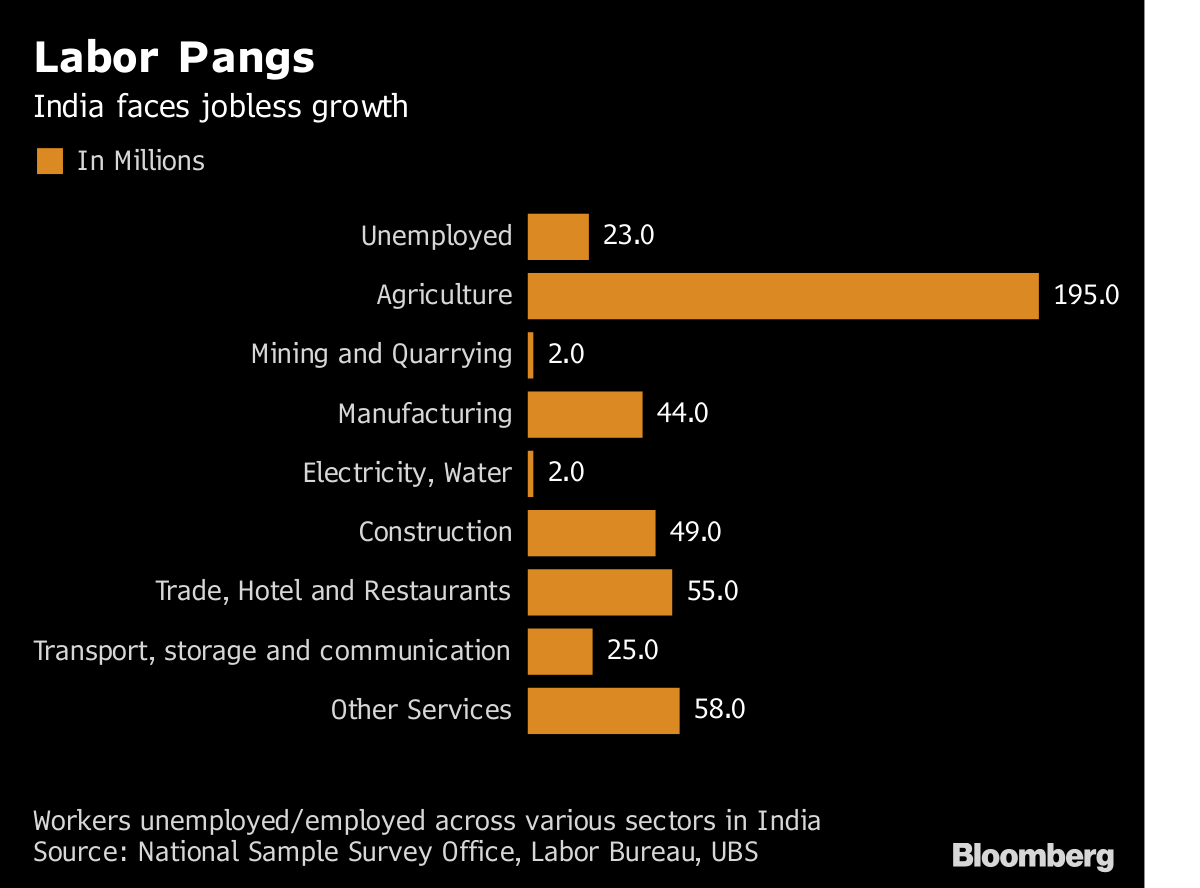

With more than 90 per cent of India’s labor force employed in the nation’s informal economy, the government has struggled to produce reliable jobs data to even get an accurate read on the level of joblessness in India. A glimpse into just how dire the job market is came in March, when the government announced 90,000 vacancies at the state-run Indian Railways, the nation’s biggest civilian employer, and a staggering 28 million people applied.

The rail jobs pay a minimum of 216,000 rupees ($3,085) per year – a princely amount in a country where per-capita income is about $1,800, versus more than $8,800 in China.

India should be enjoying a demographically powered economic dividend at this stage of its development. It’s one of the youngest countries in the world with a median age of 28, compared to China’s 37 and 47 in Japan.

Yet economic gains from favorable demographics aren’t automatic. A lot depends on whether the government can harness that dividend and overcome the population’s skill shortage. And time is ticking – in 2040 the share of the population that’s of working-age is set to start declining.

According to Ejaz Ghani, a World Bank senior economist and India expert, there’s concern that India’s job challenge will remain long into its future. One worry is that India will join the global trend toward more protectionism, limiting its manufacturing and technological progress. Another challenge is that the growing use of digital technologies would create more skilled and productive jobs while displacing less-skillful and labor intensive positions.

“Growth, education, home ownership, better economic security, and a desire for more durable goods are the cause and consequence of young demographics. But demographic dividend can also transform into a curse,” he wrote earlier this year.

What Our Economists Say… A massive, young, rural workforce could turbocharge growth, or torpedo political stability. China solved the problem by going from farm to factory. For India, entrenched global supply chains and domestic policy failures mean that path will be difficult to follow. Another is more accessible. India is going from the farm to services.- Abhishek Gupta, India economist, Bloomberg EconomicsFor more, see our India Insight

The jobs void risks tarnishing the country’s image as an investment destination, stoking social unrest and posing a threat to Prime Minister Modi’s re-election bid early next year. That explains why employment creation is a top priority for Modi after he made a campaign promise to create 10 million jobs each year. As he nears the end of his five-year term, he doesn’t have any credible numbers to show that he’s met that goal.

In his defense, Modi has said there are enough jobs and the data doesn’t properly reflect the job creation during his tenure. From commissioning fresh field surveys to using payroll data, he has tried multiple ways to measure employment generation in the country.

India’s Transition From Farm to Services

However, there is also evidence that Modi’s policies have created economic setbacks.

Data provided by private research firm, the Centre for Monitoring Indian Economy Pvt., show 1.5 million jobs were lost immediately after a ban on large-denominated money notes was imposed in late 2016. And last July’s chaotic introduction of a consumption tax adversely affected labor-intensive sectors like farming and construction.

Those twin blows dragged India’s growth to a sub-par 6.6 per cent in the financial year ended March 2018.

Eswar Prasad, a professor at Cornell University and an ex-International Monetary Fund official, says a sustained growth of 7-7.5 per cent will lead to a healthy increase in per-capita income over time. However, there is a vast gap between China and India that needs to be bridged.

“The key requirements for sustaining high growth are to develop and reform the financial system, free up labor markets, improve physical and soft infrastructure, and maintain fiscal and monetary discipline,” he says.- Bloomberg