")

New Delhi: Every state budget conveys two narratives. One narrative is articulated in the speech, encompassing welfare schemes, increases in dearness allowance, and announcements of new infrastructure projects. The other is embedded in the balance sheet, shaped by a decade of borrowing decisions that no single budget speech can entirely reverse or elucidate.

The maiden BJP budget of West Bengal, presented on 22 June, should be interpreted in the line of this second narrative, as the underlying data indicate a state undergoing a genuine, albeit partial, fiscal transition.

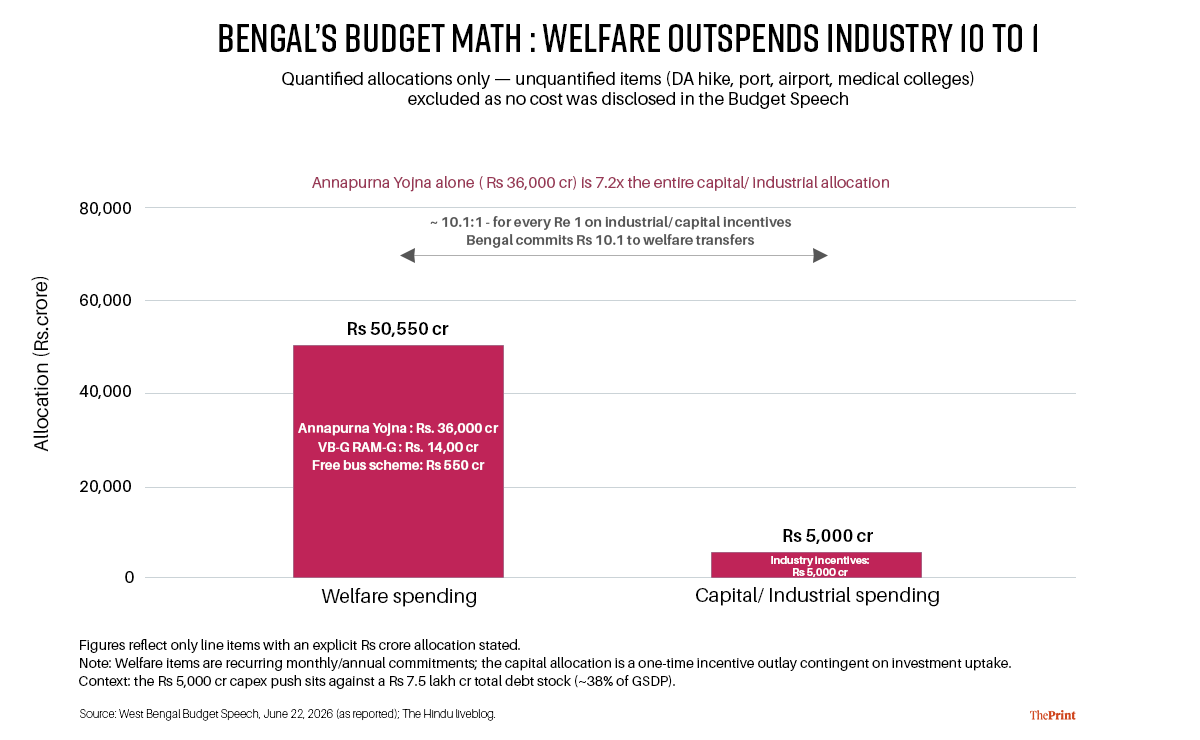

Finance Minister Swapan Dasgupta announced allocations of Rs 36,000 crore for the Annapurna Yojna, a 20 percent increase in dearness allowance, the creation of one lakh new government jobs, Rs 14,000 crore for the VB-G RAM-G employment scheme, and various sectoral measures, including scholarships and salary revisions for frontline workers.

At the same time, the government indicated an industrial focus: proposing are-evaluation of the Urban Land (Ceiling and Regulation) Act, Rs 5,000 crore in new incentives, the establishment of a greenfield airport at Kalyani, and a deep-sea port at Dadanpatrabarh.

Thus, the budget aims to simultaneously uphold welfare commitments and demonstrate industrial ambition. The data elucidate the relative magnitude of each objective.

Also Read: BJP’s maiden budget in West Bengal has big announcement. 5 new districts, including Kolkata

The arithmetic behind the announcements

Excluding announcements lacking disclosed costs, such as the DA hike, the port, the airport, and the medical colleges, which are significant yet unquantified in the speech, two comparable figures remain. The quantified welfare allocations, including the Annapurna Yojna, VB-G RAM-G, and the free bus scheme, amount to Rs 50,550 crore. In contrast, the quantified capital and industrial allocations total Rs 5,000 crore, resulting in a ratio of approximately 10:1.

Notably, the Annapurna Yojna alone exceeds the entire disclosed industrial incentive package by more than sevenfold. This distribution warrants analysis from an economic perspective rather than a political one. Welfare transfers of this nature typically represent recurring commitments; once initiated, a monthly transfer becomes a nearly permanent component of the expenditure base, implying that this year’s Rs 50,550 crore effectively establishes next year’s minimum.

Conversely, industrial incentives are generally one-time expenditures, with their ultimate impact contingent upon the extent of private capital they mobilise. Both types of spending are valid policy instruments; however, they exhibit distinct behaviours over a multi-year horizon.

A state evaluating these options is essentially deciding which policy lever to pull harder this year.

What longer debt data series shows

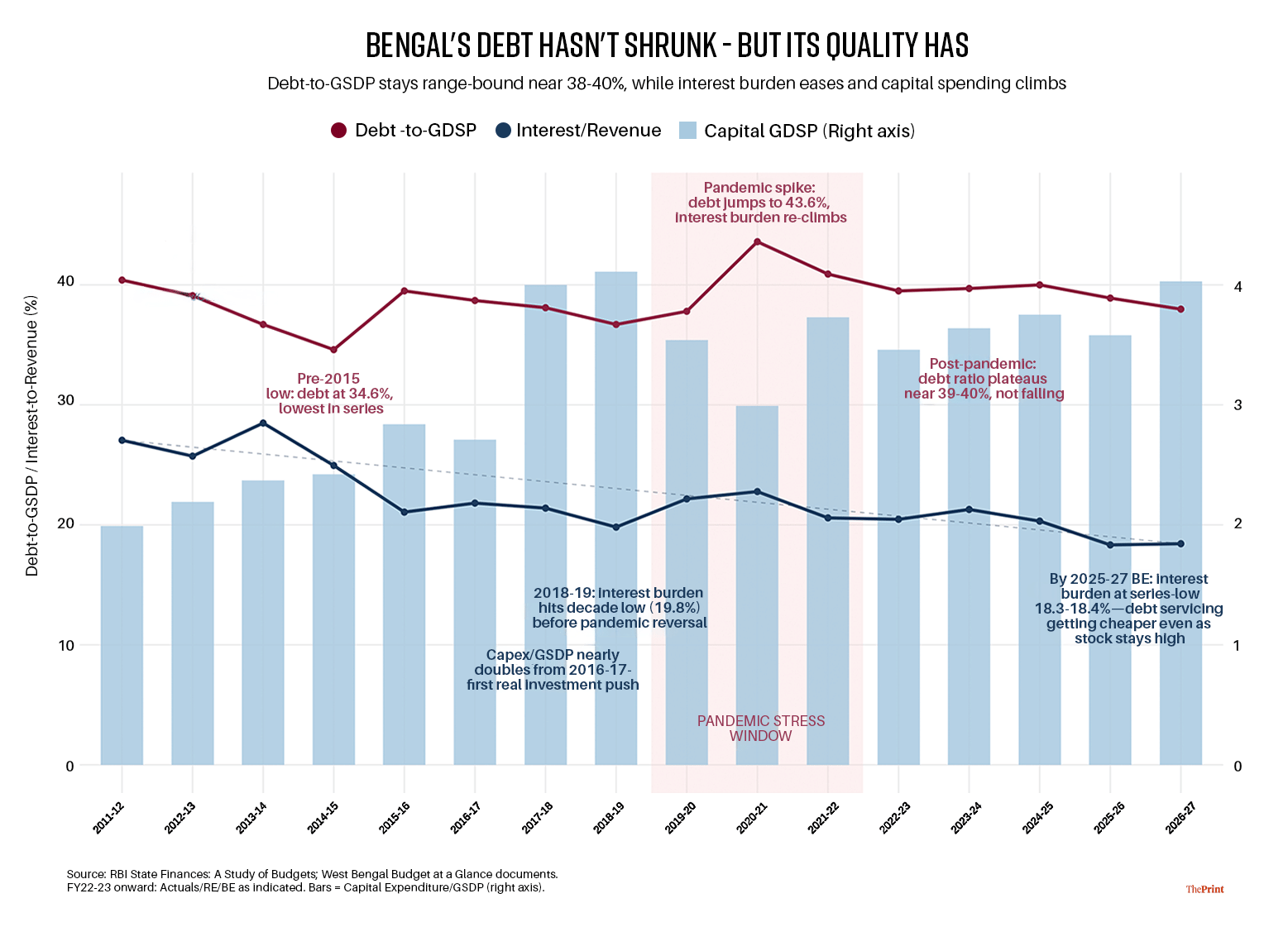

A 15-year perspective provides valuable context. The debt-to-GSDP ratio of West Bengal has remained within a specific range, fluctuating between 34.6 percent in 2014-15 and a pandemic-induced peak of 43.6 percent in 2020-21, and is projected to be 38.0 percent for 2026-27 (BE), which is comparable to its level in 2011-12 (40.4 percent).

Based solely on this metric, the debt stock has not significantly decreased over the decade. However, two additional indicators on the same chart present a more optimistic scenario.

Interest payments as a proportion of revenue receipts, which arguably provide a more direct measure of fiscal stress by indicating the extent to which debt actually constrains annual spending, have consistently declined from 27.1 percent in 2011-12 to a series-low 18.3-18.4 percent by 2025-27 (BE), with only a temporary, anticipated increase during the pandemic years. Furthermore, capital expenditure as a percentage of GSDP has more than doubled during the same period, rising from below 2 percent to over 4 percent.

In the field of development economics, this distinction between the quantity and quality of debt is standard: sustainability is determined less by the size of the debt stock and more by the trajectory of the servicing burden and the proportion of borrowing allocated to productive capacity.

By this measure, Bengal’s fiscal position has genuinely improved, despite the largely unchanged headline debt ratio.

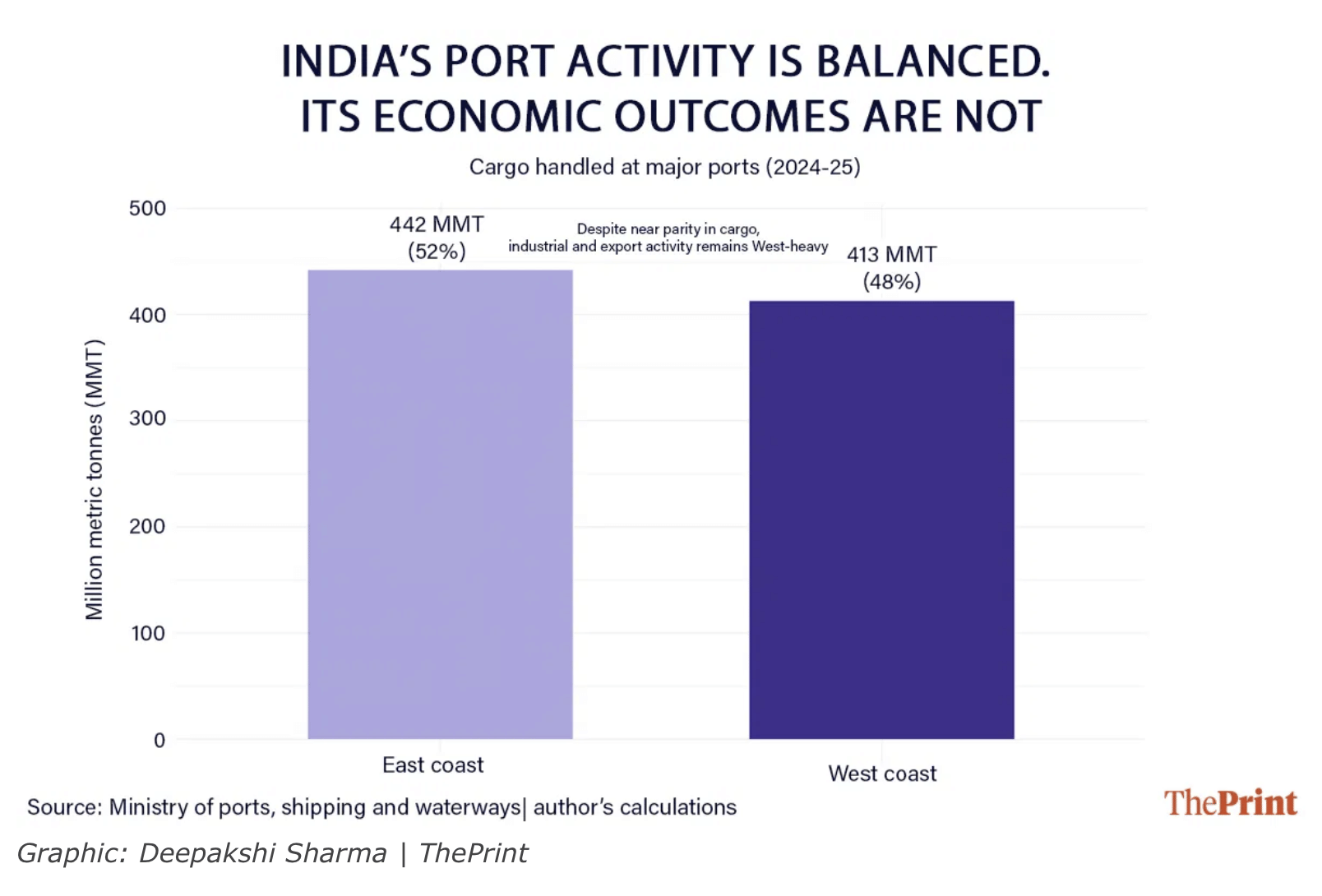

The port announcement deserves a note of caution from elsewhere on the coast. The proposed deep-sea port at Dadanpatrabarh exemplifies a recurring pattern observed in the broader context of India’s eastern seaboard.

Although eastern ports manage a cargo volume comparable to that of the western ports, they capture a smaller share of economic value. This discrepancy is primarily due to the fact that port capacity, when not integrated with industrial corridors and last-mile connectivity, tends to underperform.

Modelling of the East Coast Economic Corridor clearly demonstrates this: road upgrades alone contribute approximately 1.6 percent to the state GDP, special economic zones alone contribute 3.4 percent, and reductions in non-tariff barriers alone contribute 2.6 percent.

When these interventions are combined, they collectively enhance GDP by 7.65 percent. The instinct is directly applicable to Dadanpatrabarh: the eventual economic contribution of a new port will rely more on its integration with industrial clustering and connectivity investments within the same budget cycles, rather than being announced as an isolated infrastructure achievement.

Reading it together

The notable tension within this budget arises at the convergence of these findings. Bengal enters the current fiscal year with significantly reduced debt costs, experiencing a lower interest burden than at nearly any previous point in the series.

The state proposes to allocate some of this fiscal capacity towards a substantial expansion of welfare programs, while simultaneously initiating a relatively modest, yet symbolically significant, effort in the industrial sector.

The review of the Urban Land Ceiling and Regulation Act (ULCRA) serves as a significant structural indicator: Bengal’s manufacturing share of GSVA has only recently increased to 17-18 percent following decades of industrial decline, and the release of urban land directly addresses a persistent supply-side constraint.

The critical question remains whether the allocation of Rs 5,000 crore and the announcement of a single port are sufficient to translate this signal into tangible private investment. This uncertainty arises not from the isolated magnitude of these figures, but from their juxtaposition with a welfare commitment ten times larger and a well-documented pattern of standalone infrastructure projects underperforming on the east coast.

The more pertinent evaluation of this budget, therefore, lies not in the speech itself but in the subsequent two to three fiscal cycles. Key indicators will include whether capital expenditure as a proportion of GSDP continues its upward trajectory, whether the welfare expenditure aligns with the growth of the revenue base rather than outpacing it, and whether the port and industrial incentives are complemented by the necessary connectivity and clustering investments that determine the conversion of such announcements into economic growth.

Bengal has spent the past decade quietly enhancing its debt management practices. This budget represents the first substantial indication of whether this improved fiscal discipline will be accompanied by a similarly strategic approach to expanding the economic base that the debt is intended to support.

(Edited by Ajeet Tiwari)

Also Read: ADR-NEW analysis shows why women’s reservation bill must be delinked from delimitation