As of late last year, official data suggested India was the fastest growing major economy in the world. But serious doubts have begun to emerge about the true state of the economy. The head of the government’s own think tank has expressed alarm at a liquidity crisis that he called “unprecedented in the last 70 years,” and analysts are debating the causes and depth of an ongoing economic slowdown.

Nobody was surprised earlier this month when the World Bank lowered its 2019 growth projection for India to 6 per cent from 7.5 per cent just four months earlier, and the IMF followed suit, dropping its 7 per cent forecast from July down to 6.1 per cent.

But given the state of affairs in India’s economy to date in 2019, the immediate question for the World Bank and IMF isn’t why they lowered their forecasts, but why they still remain so high.

The dramatic slump in non-GDP indicators

We looked at the growth of leading economic indicators from official Indian government sources for April to September 2019, which corresponds to the first six months covered by the IMF’s new forecast.

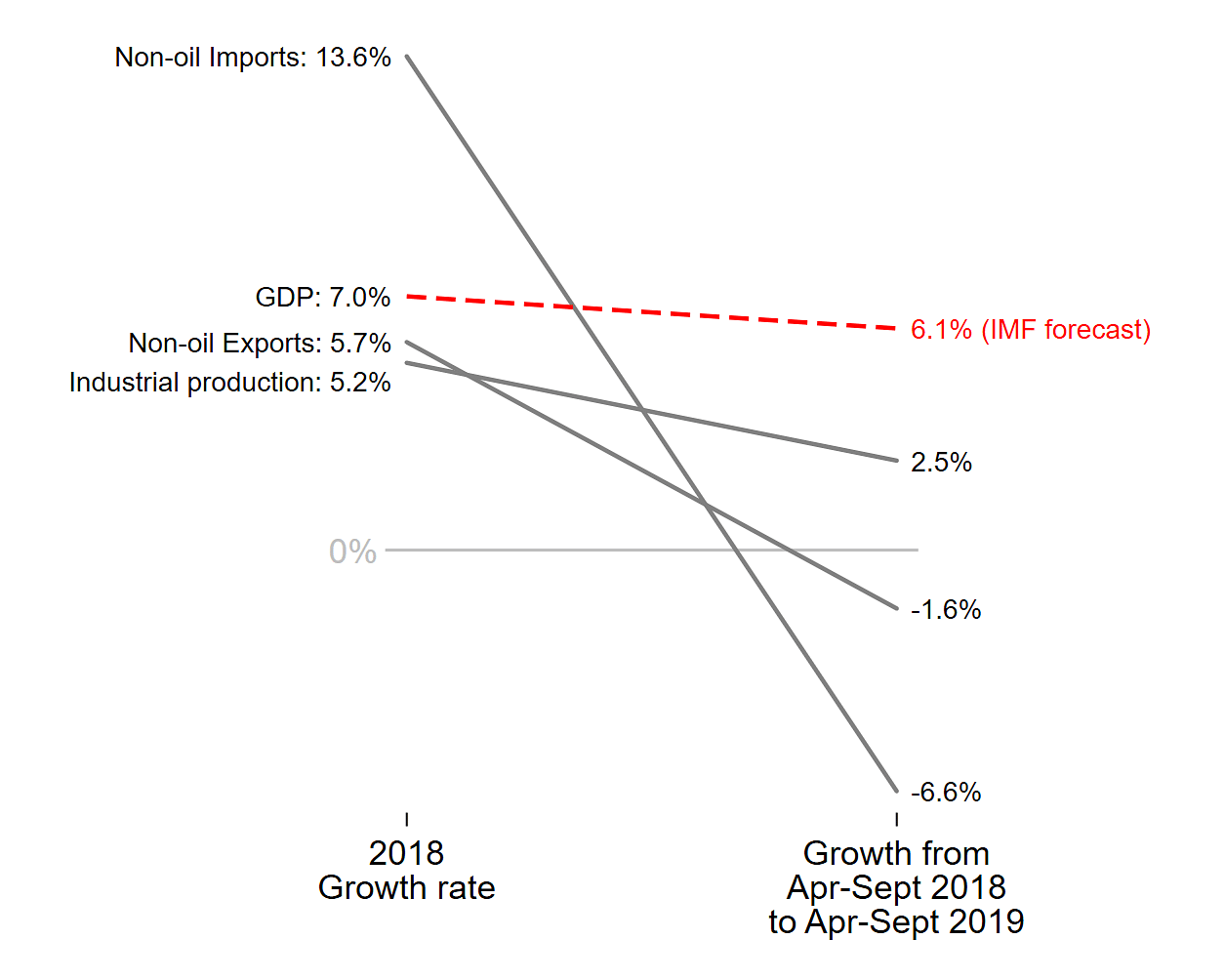

Several key indicators are not just slowing, but in absolute decline, including non-oil imports (-6.6 per cent in current dollars), non-oil exports (-1.6 per cent in current dollars), and the index of production of capital and infrastructure goods (-3.5 per cent up to August 2019).

Other indicators show positive growth, but far below the 6 per cent benchmark that the World Bank and IMF project for the economy as a whole: the aggregate index of industrial production is up just 2.5 per cent, the index of manufacturing output up just 2.1 per cent, and receipts from the goods and services tax are up just 1.6 per cent in real terms. Growth in toothpaste sales is slowing, car sales have declined for 11 consecutive months, and reports suggested declines in underwear sales.

India: IMF growth forecast versus early 2019 indicators

The IMF’s 2019 growth forecast for India looks optimistic given other key indicators for the first half of the fiscal year

The failure of GDP to track imports has been cited as evidence of manipulation of official growth rates, particularly in the case of China. A recent paper by John Fernald, Eric Hsu, and Mark Spiegel of the San Francisco Fed shows that the correlation between GDP and imports is higher in countries with better statistical systems (0.9 for the US), and that imports—which can be verified using the export data of third parties—are a better predictor of other leading economic indicators than is GDP in China’s case.

In India’s case it is not just imports, but also exports, industrial production, tax revenues, and the banking system all pointing in the same downward direction.

Also read: India’s economic slump is structural, not just cyclical

New data, new doubts

The latest indicators from April to September 2019 reinforce doubts about India’s official GDP that made a big splash in Delhi earlier this year.

In June, Arvind Subramanian, former Chief Economic Advisor to the government of India and our former colleague here at the Center for Global Development, published a Harvard working paper (and a follow-up paper) suggesting that technical changes in national accounts methodology in 2011 had led India to significantly exaggerate its official GDP growth rate ever since. Rather than 7 per cent growth from 2011-12 through 2016-17, Subramanian suggested the true rate might have been closer to 4.5 per cent. That discrepancy is, as they say, big, if true.

Official government of India sources dismissed Subramanian’s analysis out of hand, and some independent analysts have questioned whether the recent divergence of GDP growth from growth in other indicators was a sufficient basis to abandon the official figures. But other analysts have looked at the data and reached broadly similar conclusions as Subramanian. Whichever numbers you believe, the core mystery posed by Subramanian remains: How is India growing so fast if, as the government’s own statistics show, a long list of other major economic indicators have slowed or even reversed?

Also read: Trade deal or no deal, India’s economy needs systemic changes to stop under-performing

Any errors in India’s data are baked into IMF and World Bank forecasts

Suppose, just for the sake of argument, that Subramanian’s concerns are justified, and that actual growth has been considerably slower than reported growth. Wouldn’t independent analysis by the World Bank and IMF serve to ’fact check’ the government of India’s numbers?

It seems not.

The problem is that, rather than examining independent indicators of economic activity, the Bretton Woods’ forecasts appear to be based primarily on (a) extrapolation of the official growth figures, and (b) some subjective adjustment based on staff’s assessment of policy changes.

The details of the IMF’s growth forecast methodology are not publicly documented, but in response to a query, the IMF noted that the India forecast takes into account data from the first quarter of 2019—i.e., an official growth rate of 5 per cent—combined with the IMF staff’s assessment of recent policy moves, including more accommodating monetary policy from the Reserve Bank of India and a cut in the corporate income tax rate.

While reasonable on its face, this approach is extremely vulnerable when confronted with erroneous official numbers. If the growth series up to 2019 is mismeasured, then all those errors are going to be directly baked into the IMF forecast as well.

With trade volumes shrinking and indicators of real economic activity slowing to a crawl, it might be time for the IMF and World Bank to ask some harder questions. India no longer relies on the Bretton Woods institutions for any meaningful share of its financing needs, but if these DC institutions have one thing to offer Delhi, it should be an impartial, technically sound perspective on economic reality.

That reality suggests that Indian growth is in barely positive territory, while the IMF-World Bank forecasters appear too timid to tell the emperor he has no clothes—not to mention cars, toothpaste, or underwear.

Justin Sandefur is a senior fellow and Julian Duggan is a research assistant at the Center for Global Development (CGD), Washington DC. Views are personal.

This article has been published with permission from Center for Global Development.