Desperation is creeping into India’s economic policy-making. Having lost the fiscal plot, bureaucrats are trying to marshal resources by squeezing taxpayers, foreign investors, firms planning buybacks and even the central bank. Such overreach never ends well.

Tax collections last year were a full 1 percentage point of GDP lower than the 7.9% the government had hoped to obtain. Rathin Roy, director of the New Delhi-based National Institute of Public Finance and Policy, describes the situation as an “unstated fiscal crisis.” Instead of confronting the sober reality, revamping a flawed goods and services tax, and taking steps to pull the economy out of a synchronized slowdown in consumption and private investment, bureaucrats are trying to make up the revenue shortfall by taxing everything that moves.

What else can explain an increase to 42.7% from 35.8% in the tax rate on annual earnings over Rs 50 million ($730,000)? Such a steep jump sends a damaging signal to globally mobile professionals. Why should they put up with Mumbai’s poor infrastructure, New Delhi’s unclean air and Chennai’s acute water shortage when they can just as easily ply their skills from low-tax Singapore? The chilling effect won’t stop with individuals. Since many foreign funds investing in India are structured as non-corporate trusts or associations, they, too, will get caught unless they can lobby their way out.

Even if investors get a reprieve, the companies they buy won’t. Cash-rich firms looking to buy back shares will be subject to a 20% tax that until now was applicable only to dividend distributions. The Indian government may be patting itself on the back for closing a loophole, and for nudging firms to invest more in the real economy. But if the viability of new projects is doubtful, then those investments will still prove elusive. Or they will be wasteful. Embedding a valuation discount in some of the country’s most successful firms is hardly a sensible strategy to boost capacity creation.

Also read: Budget 2019 shows how India can not only become $5 trillion economy, but can also do it fast

Then there’s the Rs 1 trillion the government expects to collect in dividends from financial institutions, a staggering 43% increase from last year. Since an undercapitalized state-owned banking system can’t reasonably be expected to contribute much, the bulk of the demand will fall on the central bank. If the monetary authority’s current profits are insufficient to meet the bureaucrats’ target, they will again clamor for a return of its “excess” capital, even if that means weakening the institution’s operational independence.

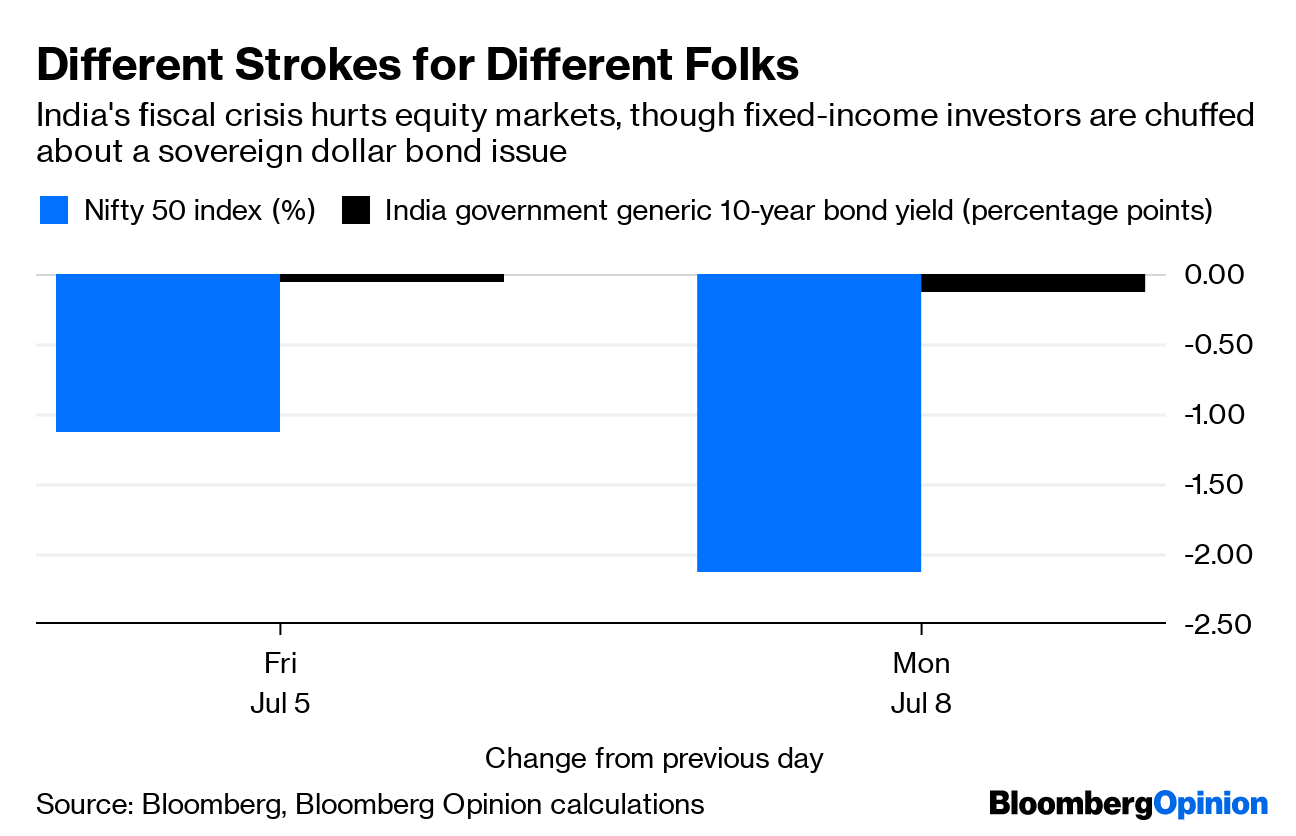

While the equity market is nervous, bond investors are ironically chuffed. Their happiness stems from New Delhi’s decision to issue dollar-denominated sovereign debt, giving up a long-held aversion to subjecting fiscal policy to foreign-currency risk. To the extent such dollar bond sales are strictly capped at a low and stable ratio of India’s overall borrowing, they will help set up useful benchmarks for the private sector to tap overseas investors. However, a more important priority is for India to emulate China and seek inclusion of its local-currency bond market in global indexes. The government should not lose sight of that goal.

As with its tax grab, India’s desperate focus on short-term fiscal fixes risks doing greater damage in the long term.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

Also read: Budget 2019 is fiscally responsible with a reforms thrust, but protectionist

This is the most critical juncture for Indian economy, where aspirations are sky high and businesses are faltering.

Four companies, AGAF (Apple, Google, Amazon and Facebook), which basically raising after 2000, have a market cap of $3 trillion.

You need to let businesses build revenues first, before raking brains on innovative ways to “tax”. Tax targets do not mean anything, if the businesses cannot improve business. And those revenues and margins will not be built in India, unless they are product and IP driven. Innovation, startups and tech MSME are so narrowly viewed, while killing the spirit of entrepreneurs. Ask how many new ones, including new unicorns, are moving out/staying out of India.

Now that the elections are over, the budgets should focus on helping ‘businesses’ build revenues, fairly. And govt should stop tech imports, and let those be built in India.

I think taxing share buybacks was a long time coming and the proof of the pudding is yet to be seen. All this talk about criticising taxes in other areas such as income tax on the elites or buy backs fails to recognise that India is one of the few growing economies or the worth investing in. If higher than normal tax rates aren’t levied now, when will they ever be? At the point that the US economy grew in the post-war period corporate tax rates were at 90% and yet, the US economy grew. India is somewhat similar only we didn’t need a global conflict to get there. Individuals who want to park their money abroad in investments are welcome to do so, but that is to assume the extra money they are now expected to pay as taxes were going to be invested in the domestic economy! Who are we kidding? The Reagan-era adage, ‘a rising tide lifts all boats’ has been proven to be bunkum and we are seeing this now with Trump’s tax cut for the rich. India’s rich can afford to pay more despite the infrastructure in Mumbai or wherever, bec they know this is the only place where there is potential for growth! So, let’s stop cribbing.

Why rich farmers are not taxed?