With polls due next year, and opposition attacking Modi govt for rescuing IL&FS, scope to utilise state-run institutions’ funds may be limited.

Even before it went belly up, India’s IL&FS Group was a strange fish: A private infrastructure financier that lent to risky projects it also owned, while throwing around the weight of nonexistent state connections to mask a multiyear liquidity squeeze.

It was only when the creature was dead to the markets that the authorities took note of the risk to Indian finance. As investors were repelled by the lender’s insolvency, New Delhi moved decisively Monday to clean up the mess. Unless the government-supervised rescue comes unstuck for some reason, it’s safe to say that India’s mini-Lehman moment has been averted.

IL&FS isn’t being nationalized, at least not yet. Existing shareholders, including India’s Life Insurance Corp., Japan’s Orix Corp. and Abu Dhabi Investment Authority, continue to own Infrastructure Leasing & Financial Services Ltd., the unlisted parent. However, the old board has been replaced by new government-nominated directors. Among them is banker Uday Kotak, who’ll most likely lead the unscrambling of a group that has 169 subsidiaries, associates and joint ventures.

When New Delhi says it aims to “immediately stop further financial defaults and also take measures to resolve defaulted dues to the claimants,” it’s hoping taxpayers’ money won’t actually be needed. The commitment alone should be enough for the debt market to treat IL&FS’s obligations as implicitly sovereign-backed.

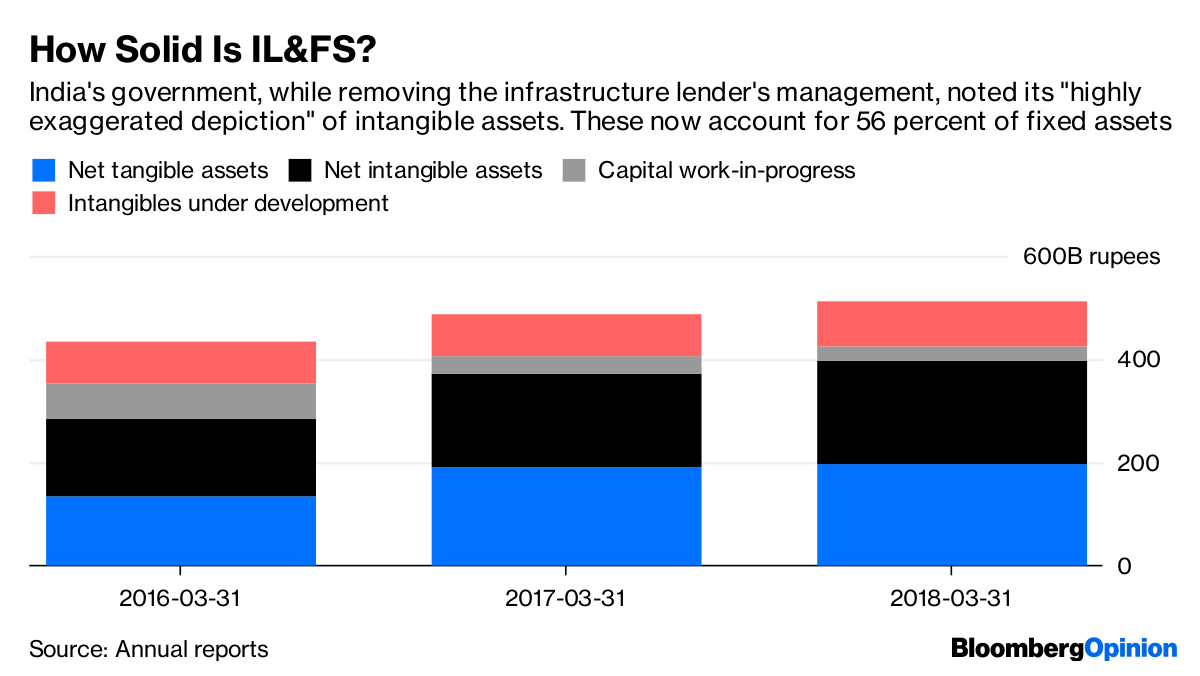

That assumption may get tested. Before the government stepped in, it was pretty clear that IL&FS wasn’t going to be trusted by the markets with even a cent in new loans. As for a 45 billion-rupee ($600 million) rights issue, proposed by the old management and cleared by the shareholders on Saturday, that money would also have disappeared into a black hole, given that the equity infusion required to steady the ship is around $4 billion, according to a Sept. 27 report by REDD Intelligence.

Now that the government is backing its liabilities, IL&FS presumably can survive on a thinner layer of equity than it would have otherwise needed. There’ll be less pressure from markets to sell assets like roads, tunnels and power plants at throwaway prices, and time for the group to fix its bloated balance sheet more sensibly.

Some deleveraging will still be required, particularly for nonperforming energy and transport projects already facing bankruptcy proceedings. Writing off 20 percent of the group operating companies’ nonfinancial assets of $10 billion would mean a $2 billion hit, in REDD’s estimates, when the current equity cushion to support the infrastructure business is not even half as thick.

That raises the possibility of a bigger rights issue. If national champions like Life Insurance Corp. and State Bank of India were to play a disproportionately large role in filling that capital hole, nationalization of IL&FS would be complete.

However, with general elections due next year, and the opposition Congress Party already attacking the government over the bailout, the scope to utilize state-run institutions’ funds may be limited. Besides, forcibly diluting international investors won’t make it easy to tap them for future projects.

Keeping the market for Indian infrastructure assets open and attractive will be Kotak’s bigger task. But that must wait until the tanks are clean of the mess IL&FS has left behind. – Bloomberg

So many checks, safeguards, independent directors, professional auditors, regulators, nothing beeped a warning sign till the cheques started bouncing. Ineptitude of the highest order. ILFS’ business model is broken. It will have to be dismantled, without a sense of panic, but with as much urgency in disposal of assets, essentially projects, as a sluggish market can absorb. Most Indian corporates are too stressed out to do much buying. One more painful reminder that Indian infrastructure is a difficult space to navigate.