Helped by a sharp global economic recovery, Indian exports are on the surge. The country recorded its highest ever Foreign Direct Investment inflows of $81.72 billion in FY2020/21. Forex reserves are at an all-time high at $620.57 billion. Most forecasts say India’s Gross Domestic Product will grow at a double-digit rate in the first quarter of the current fiscal year. Slashed corporate taxes along with low interest rates and ample liquidity have led to better profitability, and in turn, have ensured that bulls dominate India’s stock markets.

Despite this obvious exuberance, India’s economic recovery remains lopsided at best, firing on two, or more accurately, one and a half cylinders – exports and the government. There are multiple downside risks that can complicate things going forward.

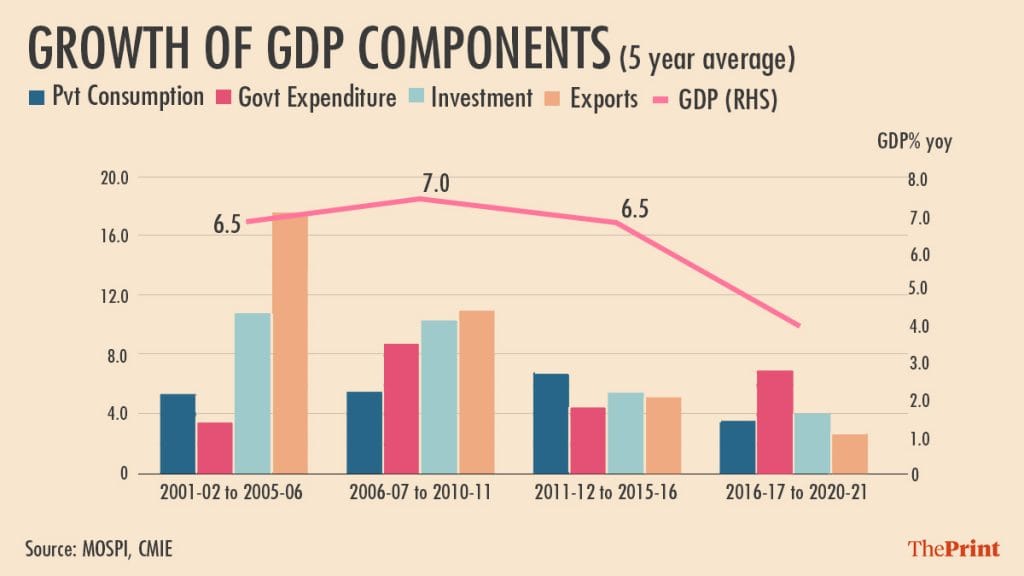

On the expenditure side, there are four components of GDP: consumption of households, investment by businesses, government spending on goods and services and net exports. Historical data would show that Indian GDP has grown much faster when investment and exports have done well. India’s investment-to-GDP ratio was 22.9 per cent in FY2000-01, which rose to 34.3 per cent in FY2011-12, growing at an average of 10 per cent. Exports rose from 11.6 per cent to 24.5 per cent of the GDP, growing at an average of 15 per cent in this period. No wonder, this is also the period of faster GDP growth except for a brief intermission in FY2008-09 due to the global financial crisis.

From FY2011-12 onwards, things started to deteriorate – double-digit inflation pushed up input costs for businesses. Together with delays in approvals (policy paralysis), it made many projects commercially unviable and led to increasing defaults on banks loans, which adversely affected their ability and willingness to finance new projects. As a result, private investments started declining. Export-to-GDP ratio after picking up at 25.2 per cent in 2013-14 started declining too, averaging just 1.4 per cent growth during 2014-15 to 2020-21. Slowing exports and investment led to moderation in GDP growth, especially after the ill-advised demonetisation, followed by badly designed and poorly implemented GST, that ruined the prospects of Small and Medium Enterprises.

To make up for sluggish investment and exports, the Narendra Modi government started spending more. Thus, the share of government spending on goods and services in India’s GDP has increased from 10 per cent in FY2013-14 to around 11.7 per cent in FY2020-21, averaging 7 per cent growth and reaching an all-time high of 16.4 per cent during Q1 of FY2020-21. The problem is that roughly 84 per cent of the budgetary support is revenue expenditure that tends to have a lower multiplier (0.99) effect on GDP growth compared to capital expenditure or private investment (2.45). Besides, there is a limit to how much government expenditure can be raised in a slowing economy when debt has crossed 90 per cent of GDP. That’s the reason why despite pressure from India Inc. for more fiscal sops, the Modi government has resisted the temptation to spend more. Instead, it has been pressuring the Reserve Bank of India to do the heavy lifting.

If that was not enough, the Indian economy got hit by the Covid-19 pandemic when it was already in slowdown mode. As a result, GDP contracted by 7.3 per cent, for the first time in decades.

Also Read: Indian economy needs to fire on 4 engines to grow. But Modi govt is betting on just 2

The unexpected export boost

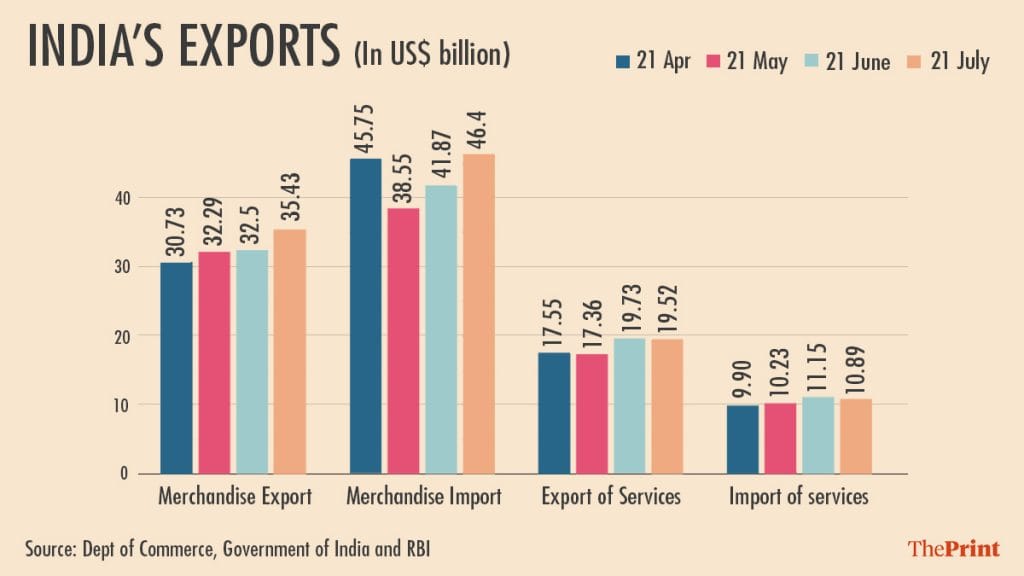

The Indian economy, however, is getting an unexpected boost from the external sector, in the form of exports and equity investment from private equity (PE) and venture capitalists. India’s merchandise exports had been hovering around $300 billion for almost a decade. However, in the first four months of the current fiscal, India’s goods export of $ 130.8 billion (as compared to an average of $100 billion or so during 2010-20) has achieved one-third (32.64 per cent) of the country’s ambitious annual target of $400 billion despite container shortages and Covid-induced supply chain disruptions. Thus, export (both goods and services) is providing the much-needed ‘demand side’ support to the Indian economy.

Along with robust exports, mostly foreign venture capital and private equity (PE) money amounting to over US$ 20 billion in the first seven months of 2021 are providing a big stimulus to the Indian economy that it badly needs.

India’s merchandise imports are also rising fast. Barring electronics and capital goods, Indian imports are mostly raw material/intermediates such as ores and concentrates, crude oil and gold, or parts and components, which are further processed into value-added products, and a substantial part of that is exported. Thus, booming exports and imports could be a signal of a quick turnaround in the Indian economy, the optimists argue.

Also Read: Why did India not fulfil its economic potential? New book outlines ‘economics of non-performance’

The fault lines

Irrespective of an increasingly supportive external macroeconomic environment, there are many domestic headwinds that may play spoilsport and derail India’s economic recovery. Although steadily progressing, vaccination remains patchy. That should be a matter of serious concern, especially when the threat of a third wave is looming.

Unlike the pandemic’s first wave, the deadlier second wave has badly impacted rural India that has negligible to no real healthcare infrastructure, especially in the poorer states of north and east India. The result is a sudden and substantial increase in out-of-pocket expenditure on healthcare, and in turn, loss of savings and increased indebtedness. This is bound to affect their demand for industrial goods and services, as well as their ability to invest in agricultural operations. To make matters worse, concerns about monsoon rains (on which roughly half of India’s gross cropped arable land depends for irrigation) remain, not in terms of the overall quantity, but their timing and distribution across different Indian states. The erratic and uneven distribution of monsoons resulted in a lower Kharif acreage by 2.36 per cent as of 6 August, which will have implications for the management of food inflation.

Moreover, weak consumer demand for discretionary goods and services and lower capacity utilisation has kept, and will keep, private investment muted for some more time. Indian companies are focusing on margin improvement by cutting all kinds of costs — employees, marketing and promotion, and wherever possible, raw material — to remain afloat. However, there’s a limit to pruning down raw material cost, amid a runway commodity price inflation. Thus, everyone is trying to squeeze the employees and smaller vendors, which, in turn, will have an adverse impact on household income and their demand for goods and services going forward.

However, there are a few exceptions here. First, the relatively affluent section of the Indian working population. Though there is some effect on salaried income due to cost-cutting in the corporate sector, and further erosion in purchasing power due to high inflation, other income, especially from investments in equity and mutual funds (which are taxed at lower rates between 10 and 15 per cent compared to income from salaries that are taxed at up to 42.77 per cent) have gone up.

Second, in India’s tech sector, including tech startups, there are neither job cuts nor salary cuts. Instead, companies are not finding enough employees despite their willingness to pay generous salaries and allowances. This can be seen in the surge in attrition rates among Indian IT companies in the first quarter of FY2022. Despite the fact that this segment of better-off Indian households is small (10-15 million), it will support the demand for discretionary goods and services, including demand for premium housing. However, demand from this segment is likely to be appropriated by large companies in the organised sector that possess pricing power. These are the companies that can also pass on a part of the rise in input costs to consumers. Thus, most of the Capital expenditure (CapEx) is happening and will continue to happen, in this segment. A broader CapEx recovery is far away in our opinion.

Overall, India’s economic recovery is lopsided but is an increasingly positive story. Lopsided because the other two major engines — consumption and investment, which make up more than three-fourths of the Indian economy — are yet to recover. Similarly, we can’t really look away from the condition of the country’s informal sector workers and SMEs — segments worst affected by disruptions caused by the pandemic. It will continue to limit India’s growth prospects going forward.

Ritesh K. Singh @RiteshEconomist is the CEO of Indonomics Consulting Private Limited. Steven Raj Padakandla @pstevenraj1 is a faculty at IMT, Hyderabad.

(Edited by Srinjoy Dey)