In 2016, India adopted a flexible inflation targeting framework. The Finance Act of 2016 amended the Reserve Bank of India Act to provide price stability as the primary objective of monetary policy, Consumer Price Index (CPI) as the anchor, and an institutional framework in the form of a Monetary Policy Committee (MPC) to set the policy rate to achieve the inflation target.

Before the amendment, the RBI did not have clearly defined objectives and accountability mechanisms.

A key feature of the inflation targeting regime is the enhanced transparency and accountability of central banks. Transparency enables the government and the public to assess whether the central bank has achieved its objectives. A host of transparency and accountability measures were introduced through amendments to bolster the credibility of the inflation targeting regime.

Also read: Prudence over populism — why Modi govt must resist rolling out big-ticket schemes in Budget 2023

Failure to achieve inflation target

In the event of failure to achieve the inflation target, Section 45ZN of the Act lays down that the RBI will inform the central government of the reasons for failure to achieve the inflation target, the remedial actions it proposes to take and an estimate of the time within which the inflation target shall be achieved after the implementation of the remedial actions.

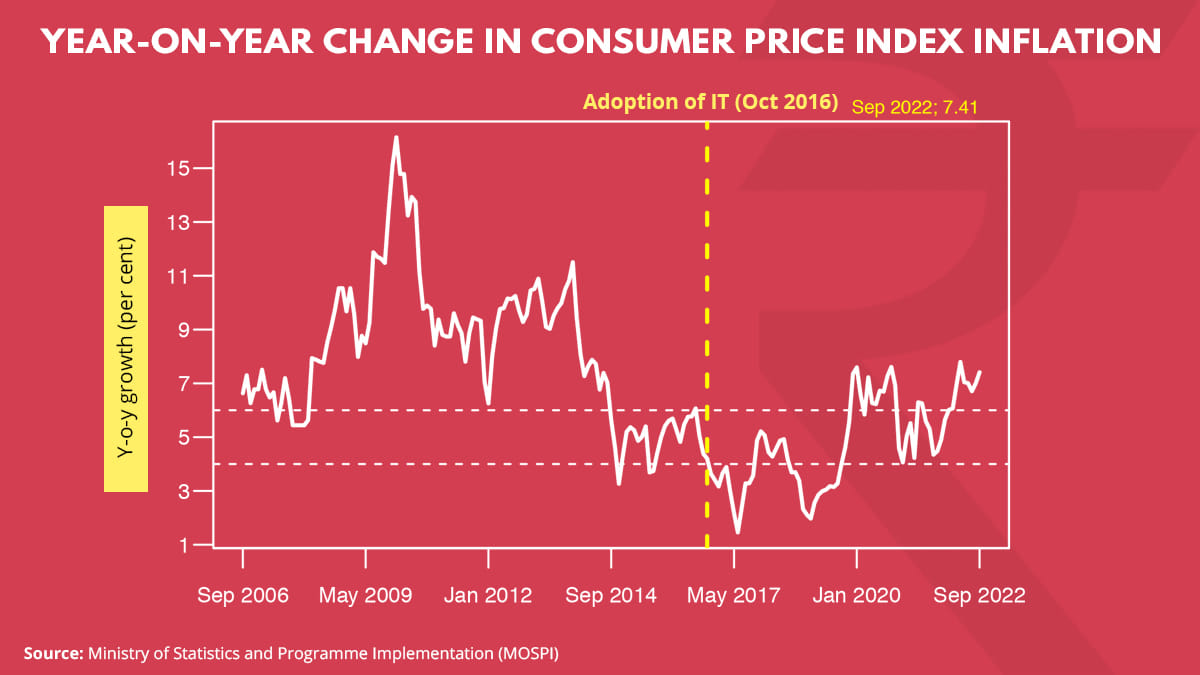

The central government has notified the factors that constitute failure to achieve the inflation target — namely, if the average inflation is more than the upper tolerance level of the inflation target (6 per cent), or is less than the lower tolerance level of the inflation target for any three consecutive quarters. CPI-based inflation was 6.34 per cent in the March quarter, 7.28 per cent in the June quarter and 7.04 per cent in the September quarter.

According to the RBI MPC and Monetary Policy Process Regulations, 2016, a separate meeting of the MPC is scheduled to discuss and draft the report to be sent to the central government. The report is to be sent within one month from the date on which RBI failed to meet the inflation target.

As the September 2022 inflation data was released on 12 October, the RBI has to submit the report by 12 November. The meeting on 3 November was scheduled to formulate a response to the government.

Global accountability mechanisms in the event of breach of inflation target

Inflation-targeting countries have adopted specific measures to efficiently communicate their actions to the central government, as well as the general public. Open letters and parliamentary hearings are the main instruments of accountability to parliament.

Open letters are usually written by the governor on behalf of the MPC, in the event of missing the inflation target. Parliamentary hearings, wherein the governor appears before parliament and provides testimony on monetary policy, is another accountability mechanism practised in some countries (for example, in Australia, Canada, South Africa).

Open letters are more prevalent in central banks with MPC as the institutional framework to set the policy rate. For instance, in the UK, there is an exchange of open letters between the governor of the Bank of England and the chancellor of the Exchequer.

As of end September 2022, there have been five consecutive exchanges of open letters.

Inflation trajectory in the post inflation targeting regime

The trajectory of the CPI inflation pre and post the adoption of the inflation targeting regime shows that despite the policy shocks and external headwinds, inflation has been reasonably range-bound within the 4 +/- 2 per cent since the adoption of the inflation targeting regime in October 2016 till before the pandemic.

Before adoption, we have seen bouts of inflation in the range of 8-12 per cent. There have been periods of sustained double-digit inflation in 2009-10 and again during 2012-13.

Post the adoption of the inflation targeting framework, in December 2019, for the first time, the CPI inflation breached the upper end of the target as it accelerated to 7.35 per cent, driven by a sharp rise in food inflation. The next two months also saw inflation above the upper end of the target band. In March, inflation eased to 5.84 per cent. From April 2020 to November 2020, inflation was above the upper tolerance band of 6 per cent.

The question of failing to meet the inflation target did not arise at that time as inflation numbers during Covid could not be relied on.

Just before the Russia-Ukraine war (January-February 2022), inflation was just above 6 per cent. However, since March 2022, inflation has been hovering at above 7 per cent.

Policy response during Covid

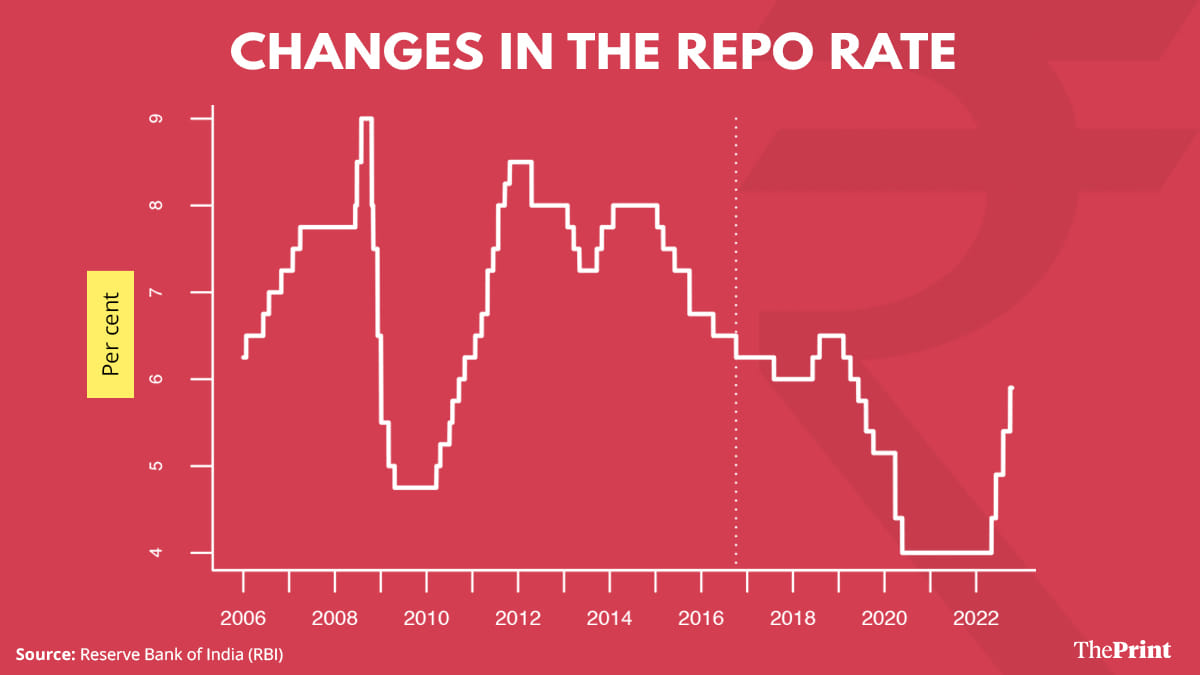

The inflation targeting framework that India has adopted gives flexibility to the RBI to also focus on growth without undermining its inflation control objective. Since the onset of the Covid-19 crisis and even before, the RBI had been focussing on growth — it had cut interest rate by 115 basis points, maintained an accommodative stance, and made a commitment to maintain the stance as long as necessary to revive growth, even though inflation had been inching up due to supply side constraints.

In addition to the conventional measures, the RBI also introduced unconventional measures to boost liquidity and incentivise banks to lend to specific sectors. Loan moratorium, asset classification standstill, easing of working capital financing, were some of the initiatives to provide relief to borrowers affected by the pandemic.

Rate hiking cycle and inflation focus

Till February of this year, the RBI’s focus was on reviving growth. Since then, there has been a change in the policy direction. In the April policy, the RBI began talking about withdrawal of accommodation while remaining accommodative.

In the June policy, the MPC statement dropped its ‘commitment to remain accommodative’. The focus has since shifted to ‘withdrawal of accommodation’ to ensure that inflation remains within the target.

Central banks including the RBI are often accused of falling behind the curve. However, these are challenging times for central banks. Rate hikes operate with a lag. They also lead to growth slowdown. Central banks have to walk a tightrope to balance growth-inflation dynamics. The accountability measures incorporated in the inflation targeting framework ensure that the focus on inflation management is not lost.

Radhika Pandey is a consultant at National Institute of Public Finance and Policy.

Views are personal.

Also read: It’s Happy Diwali for economy despite inflation, recession fears. But seasonal joy must sustain