On 10 October, the Ministry of Finance kicked off its annual budget making exercise. This will be the last full-fledged budget of the Modi government in its second term. While there will be a temptation to roll-out big-ticket schemes with massive expenditure, the coming budget should focus on fiscal prudence.

Re-introducing a consistent medium-term fiscal policy framework is crucial. This will help the government prepare for the likely growth slowdown amid monetary tightening and the adverse consequences of global headwinds, and respond flexibly.

Fiscal consolidation will also enable the Reserve Bank of India (RBI) to focus on its mandate to control inflation. In contrast, a surge in borrowings driven by higher spending would aggravate the trade-off for the RBI between managing government’s borrowing at reasonable costs and managing inflation.

Also read: It’s Happy Diwali for economy despite inflation, recession fears. But seasonal joy must sustain

Fiscal deficit target

The government has set a target of lowering its fiscal deficit to 4.5 per cent of gross domestic product (GDP) by 2025-26. In 2020-21, the government’s fiscal deficit ballooned to 9.2 per cent of GDP. The next year (2021-22) saw the deficit reducing to 6.7 per cent of GDP. This year, the government has targeted to reduce the fiscal deficit to 6.4 per cent of GDP. While the deficit has come off the highs seen at the peak of Covid, it is still elevated.

This year, the direct and indirect taxes have been robust, but they may not be sufficient to offset the surge in food and fertiliser subsidies. To adhere to the fiscal deficit target of 6.4 per cent of GDP, the government is looking at cutting non-priority spending.

The government is also looking at more efficient utilisation of funds through the Single Nodal Agency (SNA) dashboard. The SNA dashboard facilitates better tracking of funds such as the Centrally Sponsored Schemes (CSS) related funds. These reforms help in containing the fiscal deficit in challenging times.

Glide path for fiscal consolidation

Achieving the medium-term deficit target of 4.5 per cent of GDP implies a reduction of 2 per cent of GDP in the next three years. This would be a daunting task given the difficult and uncertain economic environment. Achieving this target would be further complicated if the government chooses to announce populist measures in the coming budget.

Rise in populist spending would require higher market borrowings which would lead to rise in interest burden. With rise in interest payments, the ability of the government to spend on capex would suffer.

In a welcome move, despite increase in its expenditure commitments and taking comfort from the buoyant revenue receipts (direct tax collections registered a growth of 24 per cent to Rs 8.98 lakh crore till 8 October), the government has announced a marginal reduction in its gross borrowing target for the current year 2022-23 by Rs 10,000 crore to Rs 14.21 lakh crore. Out of this, it plans to borrow Rs 5.92 lakh crore through government bonds during October-March.

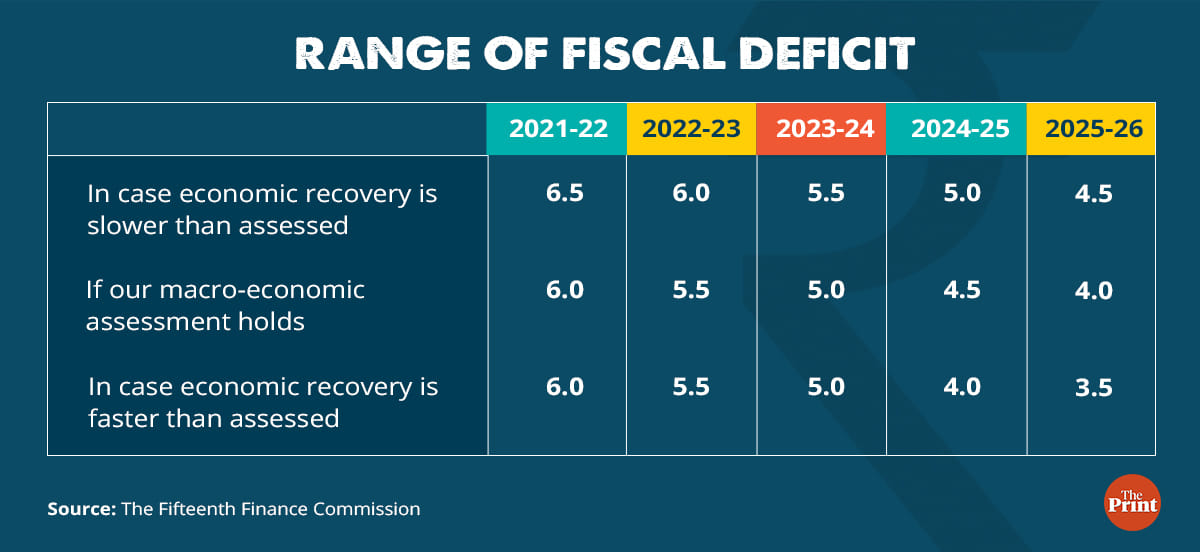

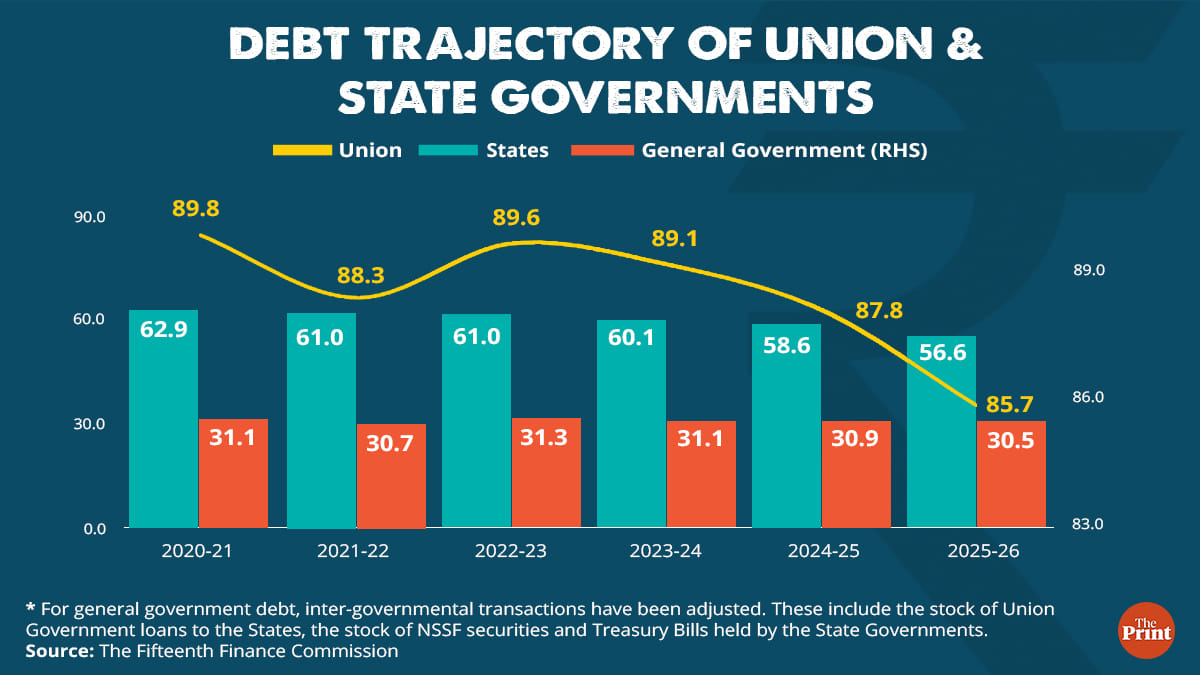

Announcement of a glide path towards the target of 4.5 per cent of GDP by 2025-26 would lend greater credibility to the government’s fiscal consolidation initiatives. While the 15th Finance Commission has given some likely scenarios of fiscal deficit and debt, they did not take into account the disruption due to the Russia-Ukraine war. The upcoming budget should introduce the medium-term projections for deficit and debt indicators.

The Finance Bill should also propose an amendment to the Fiscal Responsibility and Budget Management Act (FRBM) to reflect the revised fiscal targets. During the budget presentation for 2021-22, the finance minister announced she will be proposing an amendment to the FRBM Act towards achieving the central government fiscal deficit along the medium-term goal of 4.5 per cent by 2025-26. The amendment to the legislation is pending.

Also read: RBI’s digital rupee concept has many pros, but also some risk to India’s financial stability

Budget setting in backdrop of a challenging growth environment

The International Monetary Fund (IMF) has lowered India’s growth forecast for this year to 6.8 per cent compared to 7.4 per cent estimated in July owing to global headwinds. For the next year, the forecast for growth is retained at 6.1 per cent. Also, the report warned that a third of the global economy will contract in 2023. In other words, the worst is yet to come in 2023. The Economic Survey 2022-23, is reported to project India’s GDP growth between 6 to 7 per cent for the next year.

Given the uncertain environment, the government needs to prudently manage its finances to be able to respond to emerging contingencies in an effective manner and at the same time address debt vulnerabilities.

Lessons from the UK economic crisis

Britain’s economic chaos that followed the announcement of the biggest tax cuts since 1972 has important lessons for emerging economies like India. The announcement of tax cuts, including the elimination of the top 45 per cent income tax on the rich led to an unprecedented fall in the pound against the dollar, fall in government bond prices and rise in yields. If implemented, it would have resulted in a reduction in government revenue and surging of debt.

At a time when the Bank of England had moved aggressively to counter rising prices through interest rate increases, a cut in taxes and expansion of government spending would have interfered with the conduct of monetary policy, risking raising inflation and mounting debt. This is an important take-away for a country like India which traditionally has elevated debt levels.

Focus on macro-stability

Markets need stability, durable growth needs an environment of macro-economic stability and policy credibility. The budget should try to balance the imperatives of macro-stability and growth in the immediate term amid the uncertain backdrop, the focus should be on ensuring macro stability.

Macro stability implies that while the budget should focus on fiscal consolidation, monetary policy should focus on moderating inflation. This will also have the desired impact of calming the markets.

Radhika Pandey is a consultant at National Institute of Public Finance and Policy.

Views are personal.

Also read: Real estate, IT, gig jobs, MNREGA: Making sense of India’s roller-coaster unemployment crisis