")

In the Union Budget for 2022-23, the government announced that it will be issuing sovereign green bonds as part of its overall market borrowings to mobilise resources for green infrastructure. The government plans to invest the funds raised through the issue of green bonds in environmentally sound and sustainable projects that would help in reducing the carbon intensity of the economy.

The RBI will issue green bonds worth Rs 16,000 crore in two tranches of Rs 8,000 crore each. The green bond issuance accounts for 1.1 per cent of the government’s gross market borrowing of Rs 14.21 lakh crore.

The issuance of green bonds will foster India’s commitment towards its Nationally Determined Contributions (NDC) targets and build credibility in the global green finance ecosystem. Transparent disclosure norms, reporting frameworks and specific screening criteria of green projects will attract sustained investor interest in India’s maiden sovereign green bond market.

Also read: What do the latest GDP estimates for 2022-23 tell us about the health of the Indian economy?

Framework for green bond issuance

In November 2022, the government issued a document outlining the framework for issuance of sovereign green bonds. The framework draws from the International Capital Market Association’s (ICMA) Green Bond Principles. In the absence of any binding legal framework, the world follows the ICMA principles as a guidepost to benchmark their green bond frameworks.

The principles provide voluntary best practise guidance on the use of proceeds, process for project evaluation and selection, management of proceeds and reporting. The principles provide a broad list of project categories, which could be supported through the issuance of green bonds.

Drawing on the principles, the government’s sovereign green bond framework document provides a list of eligible categories of projects. These include renewable energy projects, projects that promote energy efficiency, projects towards pollution control etc.

The government intends to allocate funds within 24 months following issuance. The devolution of funds will be in tranches subject to achievement of targets specified in the project document.

The Ministry of Finance has constituted a Green Finance Working Committee to facilitate the process of project evaluation and selection. Under the supervision of the Committee, an annual report on the allocation of proceeds to the eligible projects, the description of projects financed, status of implementation and unallocated proceeds will be brought out.

The funds raised through the issuance of green bonds will be deposited in the Consolidated Fund of India (CFI). Funds will be made available through the CFI. The Public Debt Management Cell (PDMC) will keep a track of proceeds and monitor the allocation of funds towards eligible green expenditures.

Motivations for issuing and investing in green bonds

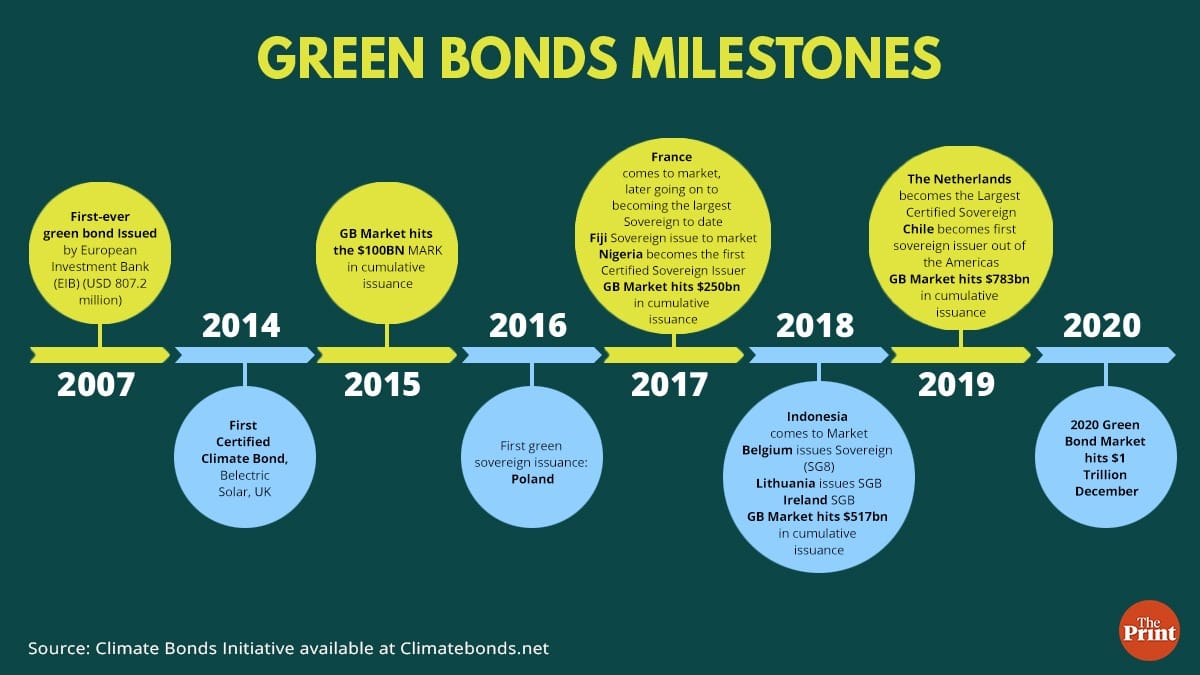

While companies have been issuing green bonds, sovereign green bond issuance is a relatively new phenomenon. The first sovereign green bonds were issued by Poland as recently as 2016. By end December 2020, the green bond market hit USD 1 trillion.

As of June 2022, 25 countries have issued sovereign green bonds. The most recently issued sovereign green bond was by Singapore. The Singapore government has indicated a pipeline of up to S$35 billion of sovereign and public sector green bonds that will be issued by 2030.

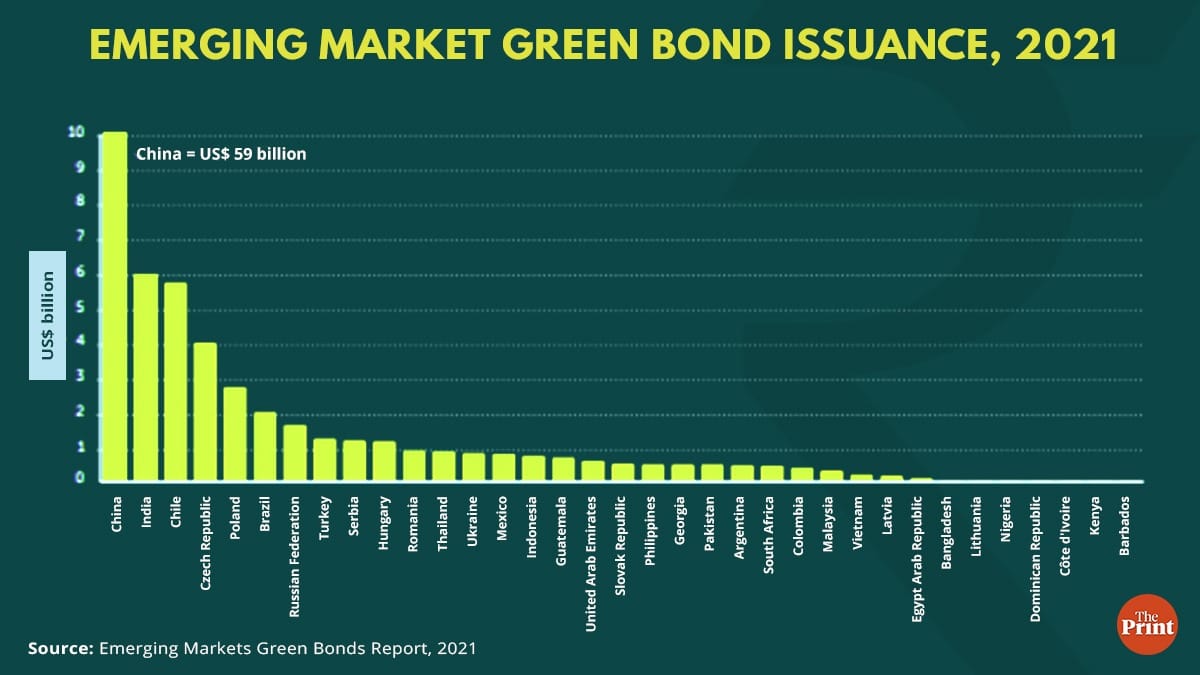

As far as emerging markets are concerned, 2021 was one of the strongest years with USD 95 billion issuance of green bonds. After China, India was the second largest issuer of green bonds amongst the emerging economies.

India entered the green bond market in 2015 with YES Bank issuing the first green bond for financing renewable and clean energy projects, particularly for wind and solar. The issuance was in the form of a green masala bond.

Gradually, the green bond market has expanded to several public sector undertakings, state-owned commercial banks, state-owned financial institutions, corporates, and the banking sector. The entry of sovereign to the green bond market signals commitment to low-carbon growth strategies, and helps crowd-in the private sector.

If an entity (sovereign or a company) chooses to issue a green bond, it may attract new investors interested in green investment, thereby increasing demand for the bond. If the enhanced demand pushes the green bond’s yield lower than that of a comparable bond, this yield difference is called the green premium, or “greenium”. An investor will be willing to sacrifice immediate financial returns in terms of lower yield for larger environmental benefit.

Other motivations for issuing green bonds include longer maturity and access to a new segment of investors. Green bonds attract new socially responsible investors and asset managers with green investment mandates. For instance, Poland experienced significant investor diversification, almost none of whom had previously invested in sovereign bonds from Poland. Sovereign green bond issuance also helps grow private green bond markets.

Guard against risk of greenwashing

The ICMA Green Bond Principles contain general principles but not clear and detailed definitions. The use of broad eligibility criteria creates uncertainty as it leaves scope for subjectivity on determining the “green” eligibility of projects.

Though work in this direction is already underway, it would be desirable to adopt a more granular taxonomy which defines eligible “green” projects.

The definitions should be aligned with globally accepted taxonomies, such as the European Union’s taxonomy or that prescribed in the Climate Bonds Standard (CBS). Foreign investors would like to invest in projects that align with globally established taxonomies due to their regulatory requirements. Alignment to a globally accepted taxonomy will foster certainty and comparability. This will ensure a steady flow of investments and reduce the risk of “green washing”.

External verification is a welcome step

An independent second-opinion provider, Center for International Climate and Environmental Research (CICERO), Oslo, has reviewed India’s green bond framework and has approved its alignment with the ICMA green bond principles. However it has raised some concerns and has categorised the framework as medium green as part of their Shades of Green methodology.

While some of the sectors such as renewable energy and adaptation have received medium to dark green shading, some sectors such as sustainable water and waste management, pollution prevention and control have received light or light to medium green shading. The light green shading reflects the broad nature of the category and the absence of any specific thresholds.

Reap the benefits of greenium

The government can reap the benefits of greenium by engaging with investors. Regulatory changes may also be needed to ensure better domestic institutional participation. RBI through its discussion paper on climate risk has nudged banks to scale up green finance. The Insurance Regulator has also encouraged its regulated entities to invest in sovereign green bonds.

Since PDMC will play a critical role in the issuance, the agenda of transitioning the cell to a statutory public debt management agency will be another favourable step in this direction. A diversified investor participation for sovereign green bonds can pave the way for developing a deep and liquid bond market in India.

Radhika Pandey is Senior Fellow at National Institute of Public Finance and Policy.

Views are personal.

Also read: Stronger revenue, lagging capex — why states need to start spending more, and soon