Get ready for a glut of liquefied natural gas.

It may sound counterintuitive. After all, the Strait of Hormuz remains blocked. The world’s largest LNG plant is idled and Qatar says repairing it will take at least three years. And yet, the contours of a long-term surplus are already starting to emerge.

The outlook for LNG prices is crucial in Europe and Asia, where the commodity is either burned to generate electricity and heat, or used as feedstock to produce chemicals and fertilisers. In those regions, where LNG prices go so goes inflation.

The war in Iran has sent benchmark LNG prices sharply higher — although far below the all-time high set after Russia invaded Ukraine. In March, the Asian benchmark known as JKM briefly rose to about $30 per million British thermal units, up from less than $11 in February. For comparison, it jumped eight-fold jump in 2022, nearing $70.

Unless the peace talks between Washington and Tehran fall apart and Hormuz remains closed beyond July, LNG prices are set to drop again — and remain low for an extended period.

To understand why, we need to delve into the plumbing of the industry. The beauty of LNG is that once the gas has been super-cooled to about minus 160 Celsius, it transforms into a liquid that can be loaded into tankers and shipped around the world, very much like oil. Thus, LNG can reach any global customer, breaking the historical limitation of gas pipelines.

Building those liquefaction plants requires huge upfront investments, with some costing between $20 billion and $30 billion. As a result, LNG companies only give the go-ahead on new facilities when they have secured enough clients to convince their banks a project is safe. That mechanism helps to keep the market relatively balanced, with supply expansion matching demand growth.

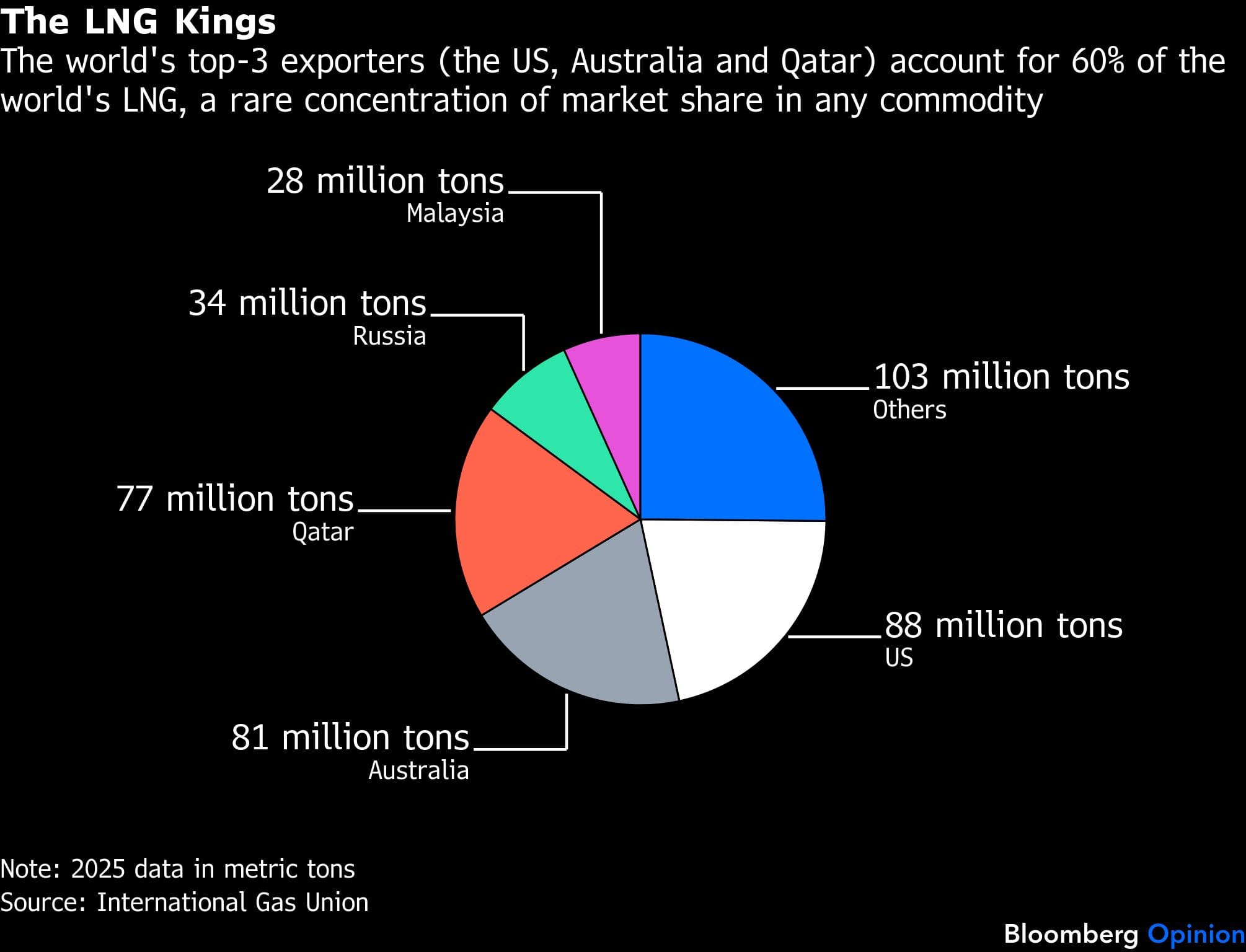

Enter the US-Israeli war in Iran. The closure of the Strait of Hormuz removed 20% of the world’s LNG supply(1), leaving some importers, particularly in southwest and southeast Asia, desperately short. They won’t forget. The most-affected nations — think India, Bangladesh or Pakistan — are the kind of price-sensitive energy importers the industry is counting on as future consumers.

Their response to the disruption will shape the LNG market for years to come. I anticipate both a supply and a demand reaction.

Let’s start with supply. Having witnessed the closure of Hormuz, no sane policymaker in Asia is likely to consider the waterway safe again. Diversifying away from Qatar and the United Arab Emirates will become a priority. Therefore, Asian LNG buyers will support projects elsewhere, financing pipe-dream ventures that only 90 days ago looked destined to fail. We can summarize this as “everything outside Hormuz gets built,” with the crisis guaranteeing a construction boom outside the Persian Gulf.

Since the turn of the millennium, the global LNG market has absorbed every supply wave fairly quickly, in two to three years. China swallowed a large amount of the 2009-2011 wave, when supply jumped by about 40% after the completion of several projects in Qatar. Europe absorbed the 2016-2019 wave, which came after a huge buildup in US export capacity on the back of the shale revolution, increasing global production by 45%. It helped that Europe had to cut its reliance on Russian gas from 2022 onward.

Before the current war broke out, the market was contending with a third wave, which was set to last from 2026 to 2030, and a likely glut. This wave is not only still in the cards — though probably delayed about a year due to the closure of Hormuz — but it should be larger and likely longer lasting. Some will come from Asian buyers’ move to finance more and more projects in North America, Africa and Latin America. But Qatar will also want to increase production, using its low cost as incentive to find buyers. That expansion is delayed — maybe six months; maybe 12; maybe even 18 months. Whatever the length, it’s largely immaterial to what happens in 2030.

Last year, the LNG industry greenlit the construction of 100 billion cubic meters of new capacity, the most ever, according to new estimates from the International Energy Agency.

“There remains a pipeline of over 700 billion cubic meters of projects globally seeking final investment decision, including around 110 billion in the US that have received regulatory approval,” according to the IEA. Last year, global LNG production stood at nearly 600 billion cubic meters. If everything that could get built does get built, the global LNG supply will more than double.

Would there be enough demand? I doubt it; or at least, I doubt it at prewar price levels. LNG costs will need to decline further to incentivize more consumption. It won’t be easy. LNG has suffered two reputational blows in four years: First Russia invading Ukraine, and now the Iran war. Again, no serious policymaker would wait for a third. For supply, diversification away from Hormuz will be key; in demand, the diversification will be away from LNG itself. Buyers have options: solar, with the help of batteries, and coal.

Back in the 1970s, the oil crisis forced industrialized nations to embrace coal. At the time, they had very few options other than nuclear. This time, Asia can turn to cheap Chinese solar photovoltaic panels — and abundant coal. As such, the dirtiest of fuels may emerge from the conflict in Iran as an energy security commodity, not only for electricity generation, but also to manufacture fertilisers and plastics via coal-to-chemicals.

It’s a story as old as the commodity market: Today’s high oil prices will sow the seeds of tomorrow’s low ones. For a short period, LNG costs may remain somewhat high as importing countries, particularly in Europe, rebuild their inventories ahead of the 2026-2027 winter heating season and everyone purchases a little more than needed, just in case the fighting in the Gulf flares up again. But a buyer’s market is around the corner.

Disclaimer: This report is auto generated from the Bloomberg news service. ThePrint holds no responsibility for its content.