In their attempt to tame the rising price pressures on pulses, the Ministry of Consumer Affairs, Food & Public Distribution, and Ministry of Commerce have been prolific. In less than three months since May 2021, the ministries have come up with six major policy actions to ease the pressures. Despite this, the prices do not seem to be losing steam. We track these policy actions and highlight a few gaps.

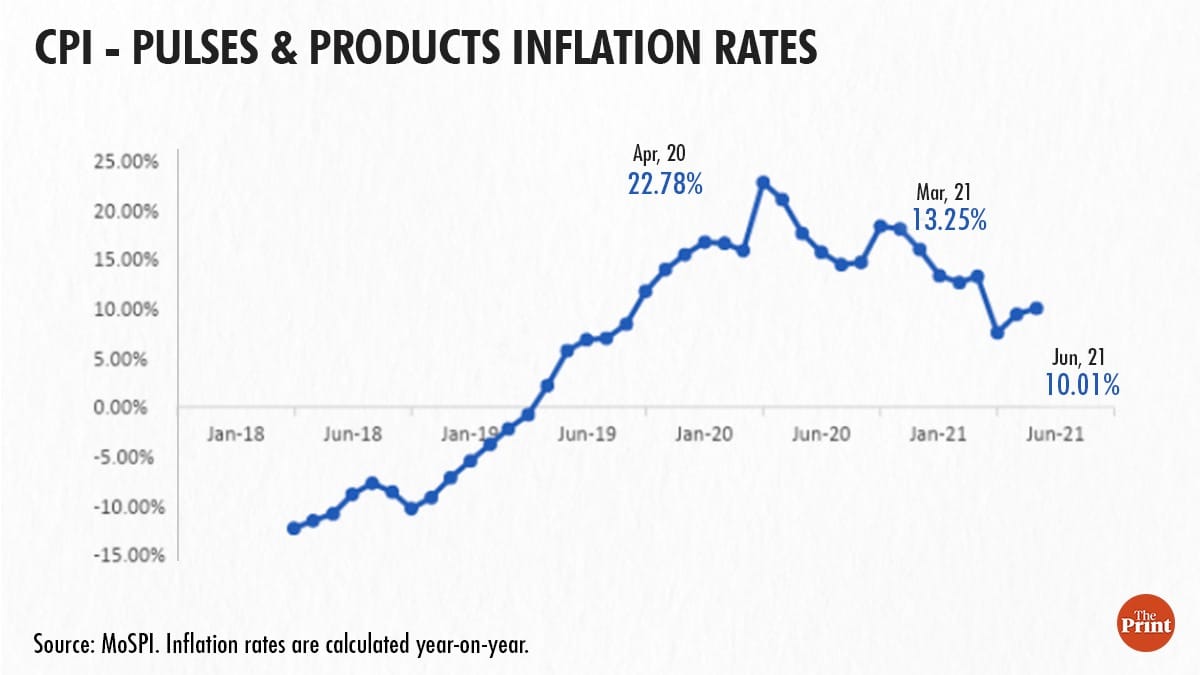

First, the background. Pulses and products (P&P) have a weightage of about 6.1 per cent in India’s consumer price index (CPI) and since October 2019, CPI (P&P) rose at double-digit rates till March 2021. The rates moderated to about 7.5 per cent in April but have again started rising since (Figure 1).

India is the largest producer and consumer of pulses in the world. In the last three years, production of most pulses has been rising. This year is no exception. As per estimates by the Ministry of Agriculture and Farmers Welfare (MoA), India produced about 26 MMTs of pulses in 2020-21 (about 2.5 MMTs higher than last year). Of this, about 49 per cent or 12.6 MMTs is gram, about 16 per cent or 4.1 MMTs is tur, about 10 per cent or 2.6 MMTs is moong and about 9 per cent or 2.4 MMTs is urad. Despite a higher production compared to last year, CPI of pulses such as gram, masur and tur have been rising at near double-digit rates since February 2021, which is also when most pulses are harvested and enter the market.

To address this inflation, the Narendra Modi government has undertaken a multipronged approach.

To increase existing supplies, the government removed the import quota restrictions on moong, urad and tur on 15 May 2021, but their duties remained unchanged. For moong, however, on 26 July 2021, the government reduced the basic duty to zero for all non-US imports (and to 20 per cent for all US imports).

To augment supplies in the future, the government signed two bilateral agreements with Malawi and Myanmar on 16 June and 26 June for tur and urad. It also extended its existing MoU with Mozambique for tur.

In addition, the government also directed the National Agriculture Cooperative Marketing Federation of India (NAFED) to offload three lakh tonnes of gram from its existing stocks, in the open market until August 2021.

The biggest policy action, however, came in the form of invocation of the provisions under the Essential Commodities Act (ECA) aimed at making private stakeholders offload their stocks, thereby increasing supplies.

As pulses have a shelf life of about nine months to a year, many stakeholders, including farmers, tend to hold back their stocks to release at a later date for better realisation of prices. To get these players into early action, the Department of Consumer Affairs (DoCA) invoked provisions of the ECA in three sequential notifications. First came on 14 May 2021, when DoCA directed states to declare the amount of stock holdings of traders, millers, wholesalers, importers and stockists. This step, however, did not mandate traders to declare their stock holdings, nor did it force offloading of those stocks. This was more a forewarning of more stringent ECA provisions to be invoked on stakeholders if prices continued to rise. The stricter measures came on 2 July 2021 with the next notification, which not only imposed stockholding limits (on wholesalers, retailers, millers and importers for all pulses except moong) but also ordered offloading of excess stocks by 31 July 2021. However, within the next 17 days, these provisions were partially eased when on 19 July 2021 the Modi government declared its third notification that allowed the wholesalers and millers to hold back larger quantities of stocks and more importantly, removed importers from restrictions on their stock holdings.

Also read: Forget petrol & diesel, prices of edible oils have soared even higher in June, July

How did these notifications effect prices of these pulses?

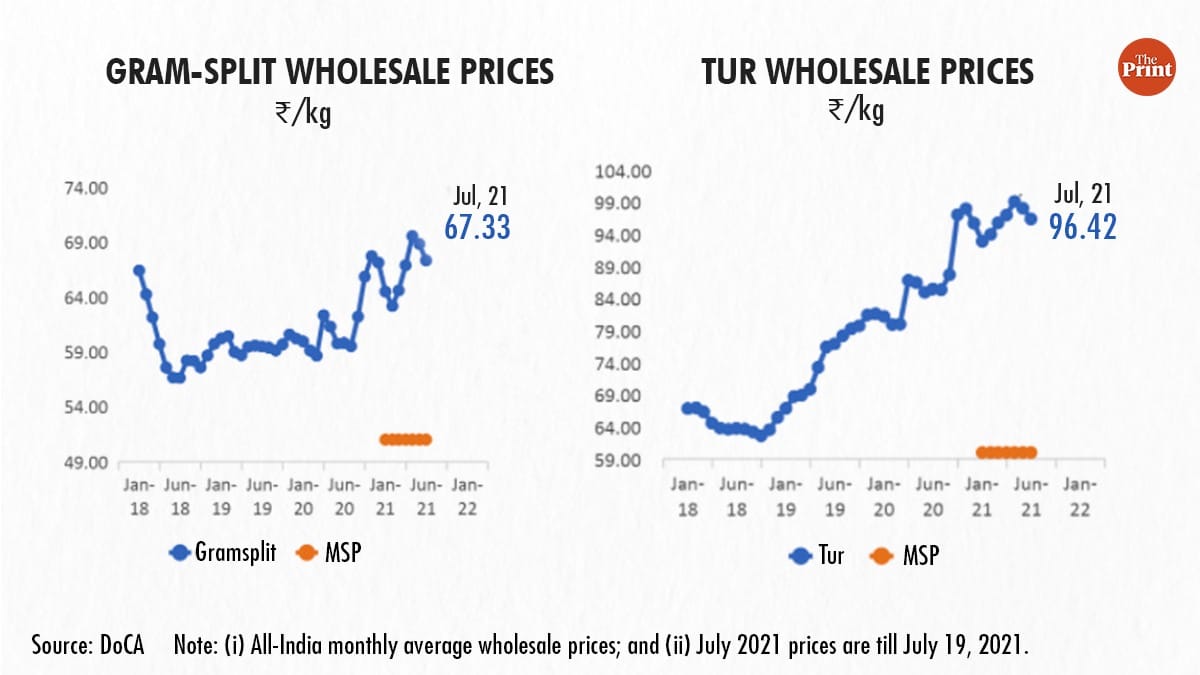

We plot the price series for the two most important pulses: gram and tur in Figure 2. Since May 2021, wholesale prices for both these pulses moderated in June and July. However, it appears that despite the fall, prices continue to be high. One then wonders why the DoCA rushed to ease the stocking limit orders and reversed parts of its 2 July 2021 notification.

Also read: Erratic monsoon hits cereal, pulses, oilseed sowing in top producing states amid inflation

Gaps in policy actions

While we commend the Modi government for being proactive in regulating trade policies to tame price pressures, the continued price rally mandates a relook at some steps. Some pointers are given below:

- Policy pendulum:Within 17 days, the government reversed parts of an order/notification. Even though it reflects its proactive management, it does highlight the myopic nature of its decisions and adversely impacts their credibility. Besides, had the prices really moderated, such a reversal would have still been justified. But as we see above, the sustained price rally continues.

- Stockholding restrictions on importers:If we recount the policy actions mentioned above, the policymakers on one hand opened up import of pulses but on the other imposed stockholding limits on importers. Based on assessment from the importers, it appears that an average import lot size of any pulse variety is about 125 to 200 MTs, depending on the variety and origin of imports. But if importers had a stockholding restriction at 100 MT of one pulse variety, it was uneconomical for them to import. If the importers would not import then the government’s efforts of increasing domestic supplies via increased imports would not materialise. It seems that the government did not initially spare much thought on this front. But later, in its 19 July notification, it corrected this as it removed importers from stockholding restriction. It may reflect the rather hushed approach of policy-making.

- Gap in data: As highlighted above, as per data from the agriculture ministry, there do not appear any major production pressures this year. In fact, the production is higher compared to last year. So, if production is high and rising, then why are the prices steep? For an ongoing research project at ICRIER, we study and track markets of major agricultural commodities on a real-time basis. As per our assessment of the market, it emerges that the data on production of some pulses from the Ministry of Agriculture is ratheroptimistic and that the actual production may be much lower. An example of this is gram. As per government’s third advance estimate, gram production in 2020-21 was about 12.6 MMTs, however, as per estimates by trade, the production is much lower. Now the question is: if production is indeed as high, then why is the government closely monitoring their prices? From the recent string of policy actions, it appears that the government in a way does acknowledge the gap in the production data.

- ECA Amendment 2020: Enough has already been written about how these policy actions on account do not go in line with the ECA Amendment 2020. It appears that byimposing restrictive provisions, the government may tacitly be acknowledging its current lack of confidence in the private sector in clearing markets efficiently. We need to remember that Indian production of most crops, barring rice and wheat, still fluctuates, and thus it is only over time that market dynamics can truly play out their role.

- Farmer bias: Policy stances often oscillate not just within a year but also between years and mostly aim to protect the consumers of agriculture, much to the detriment of the farmers. The plight of farmers is well documented. They lose in a good crop year as prices crash due to the glut and they also do not gain much in a year with lower production becausegovernment uses provisions such as the ECA and eases import restrictions to moderate prices. Supporting farmers need a more thorough and long-run vision, with governments taking on a more comprehensive and concerted approach.

The fact that the country is facing a deficit in supplies of its major pulses stays strong today. The Modi government needs to be on its toes as the price pressures are likely to pinch harder as we draw closer to September-October 2021 when the existing stocks are likely to be at their lowest levels. Will the government pre-empt these pressures and revert to stricter action again? Only time will tell.

It is not easy to predict prices of agricultural commodities but by directing efforts into doing so, the government can buy itself time to be better equipped to handle gluts and deficits. The first step to such predictions is access to accurate, credible, and timely data. If production data, for example, is over- or under-estimated, then the policy actions taken based on it remain corrupted and the economy is bound to suffer. Any government walks a very thin line managing prices for the producers and consumers of agriculture. But in order for it to have a long-lasting impact, it will need to invest in robust data collection methods to begin with, and inter alia ensure that it creates a dynamic yet stable and predictable policy environment for all.

Shweta Saini @shwetasaini22 is a Visiting Senior Fellow and Aishwarya Pothula is a Consultant at ICRIER, New Delhi. Views are personal.

(Edited by Anurag Chaubey)