A small exporter in Tiruppur does not follow the Strait of Hormuz. However, when shipments are rerouted, resulting in increased freight costs and delayed payments, he feels the impact immediately—not through media headlines, but through cash flow disruptions. While his order book may withstand global shocks, liquidity often does not. This encapsulates the paradox inherent in India’s MSME economy: resilience is presumed, yet fragility is systemic.

This fragility is significant because micro, small, and medium enterprises (MSMEs) are not a marginal segment of the economy. They contribute nearly 30 per cent of the GDP and account for approximately 45 per cent of India’s exports, anchoring the nation’s position in global value chains. In industries such as textiles, leather, and food processing, MSMEs form the foundation of trade. As a result, when global disruptions intensify, as observed during the ongoing West Asia crisis, the stress on MSMEs rapidly escalates into a macroeconomic concern.

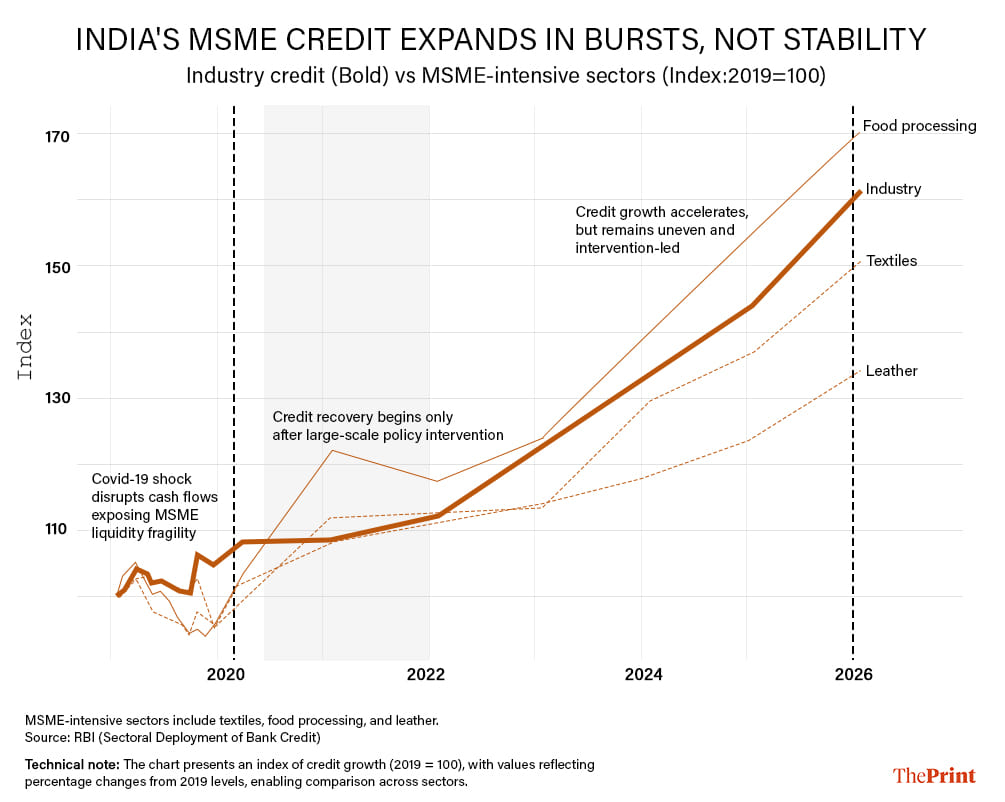

That concern is already visible on the ground.

Recent reports indicate that MSME exporters are encountering not only increased costs but also heightened compliance burdens, shipment delays, and working capital stress due to constantly shifting routes and regulatory uncertainties. The government has responded with targeted support, including the Rs 497 crore RELIEF scheme, aimed at providing insurance coverage and stabilising export flows, particularly for the MSMEs. These measures are timely and necessary, yet they also reveal a deeper pattern in India’s MSME policy response.

To understand this better, let’s first examine the behaviour of credit.

The chart shows that credit growth in India, particularly in the MSME sector, does not follow a stable, continuous pattern. Instead, it exhibits episodic fluctuations, stagnating during periods of economic stress and experiencing sharp acceleration only after policy intervention. The Covid-19 pandemic in 2020 starkly highlighted this structural vulnerability: liquidity rapidly diminished, even for otherwise viable firms, as supply chains were disrupted and payments delayed.

That shock did not result in a self-correcting recovery.

Rather, recovery came only after interventions such as large-scale credit guarantees, liquidity support, and regulatory easing. Importantly, this pattern is recurring in the present context. The recent surge in credit growth aligns with renewed policy support in response to global disruptions. However, the disparity across sectors indicates a more profound issue: growth is uneven, and resilience remains dependent on intervention. This leads us to a critical distinction. India’s MSMEs are not becoming structurally stronger; they are being repeatedly stabilised, and that distinction matters because stabilisation is not the same as strength.

The problem is not credit

The policy framework for India’s MSMEs is predominantly centred on credit expansion, encompassing guarantees, refinancing facilities, and emergency lending schemes. These are reactive measures, designed to be deployed post-crisis. While essential for crisis management, they fail to address the fundamental vulnerabilities that put MSMEs at risk in the first place.

The core of this vulnerability lies in liquidity.

For a majority of MSMEs, financial strain is not solely a consequence of credit access but is significantly influenced by the predictability of cash flows. Factors such as delayed payments, uncertain tax refunds, escalating input costs, and fragmented financing systems contribute to a baseline vulnerability. When external shocks occur, this vulnerability rapidly escalates into financial distress.

In a recent issue brief, I argue that mechanisms such as Goods and Services Tax (GST) refunds, which are typically perceived as passive reimbursements, can function as active liquidity stabilisers if effectively designed. Evidence indicates that timely and predictable liquidity flows not only alleviate immediate financial stress but also enhance credit behaviour over time.

This insight is crucial as it reframes the policy discourse.

The objective is not merely to expand credit during crisis periods but to develop systems that pre-emptively mitigate liquidity stress, thereby preventing it from escalating into a crisis.

Also read: US negotiating position is brute force. Iran’s is the power to hurt

The risk of a permanent rescue economy

India’s current strategy risks progressing in a counterproductive direction.

Each disruption, be it a pandemic, supply chain shock, or geopolitical conflict, triggers a similar response: the expansion of guarantees, the easing of credit, and the deferral of repayments. While these measures are effective in the short term, they engender a cycle in which MSMEs remain reliant on sporadic state support. Over time, resilience risks being replaced by dependence.

This has fiscal consequences. Much of this support is facilitated through contingent liabilities, such as credit guarantees and insurance coverage, that increase the state’s implicit obligations but do not directly reflect in Budget allocations. Although India may not formally revise its Budget in response to global shocks, it is subtly recalibrating its fiscal stance through MSME backstops.

This raises an uncomfortable yet necessary question: if every shock requires a new additional layer of intervention, what does that imply about the system?

Rather than withdrawing support, it is imperative to redesign it.

MSMEs should not require rescue each time the global environment becomes uncertain. Instead, they need a system characterised by liquidity flows, enforced payment mechanisms, and a financial framework where stress does not immediately lead to distress. That means a focus on time-bound, automated refund systems, enforceable payment cycles across supply chains, deeper integration of receivables financing, and liquidity-sensitive credit frameworks.

These reforms may not capture headlines, yet they are essential for transforming resilience from mere rhetoric into reality. Ultimately, MSMEs do not fail solely because of crises; they fail because the system fails to absorb these shocks.

Until this systemic change occurs, the narrative of India’s MSMEs will remain as the data currently indicates: episodic, intervention-driven, and perpetually vulnerable to the next crisis.

Bidisha Bhattacharya is Consulting Editor (Economy) at ThePrint. She tweets @Bidishabh. Views are personal.

(Edited by Prasanna Bachchhav)