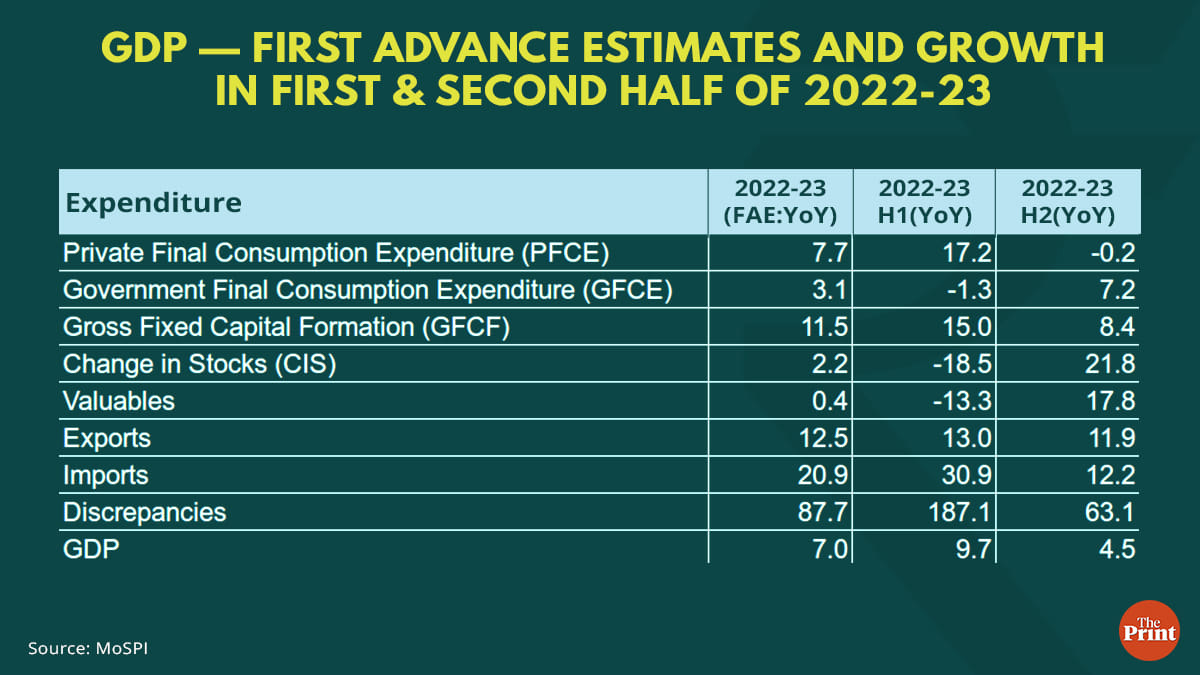

India’s Gross Domestic Product (GDP) is estimated to grow at 7 per cent for financial year 2022-23, as compared to 8.7 per cent in the previous year, according to the first advance estimates (FAE) of GDP released by the National Statistical Office (NSO). The first advance estimates are significant as they serve as essential inputs for the budget for the next financial year. Along with the estimates for the first half of the year, the FAE help in assessing the growth performance in the second half of the year.

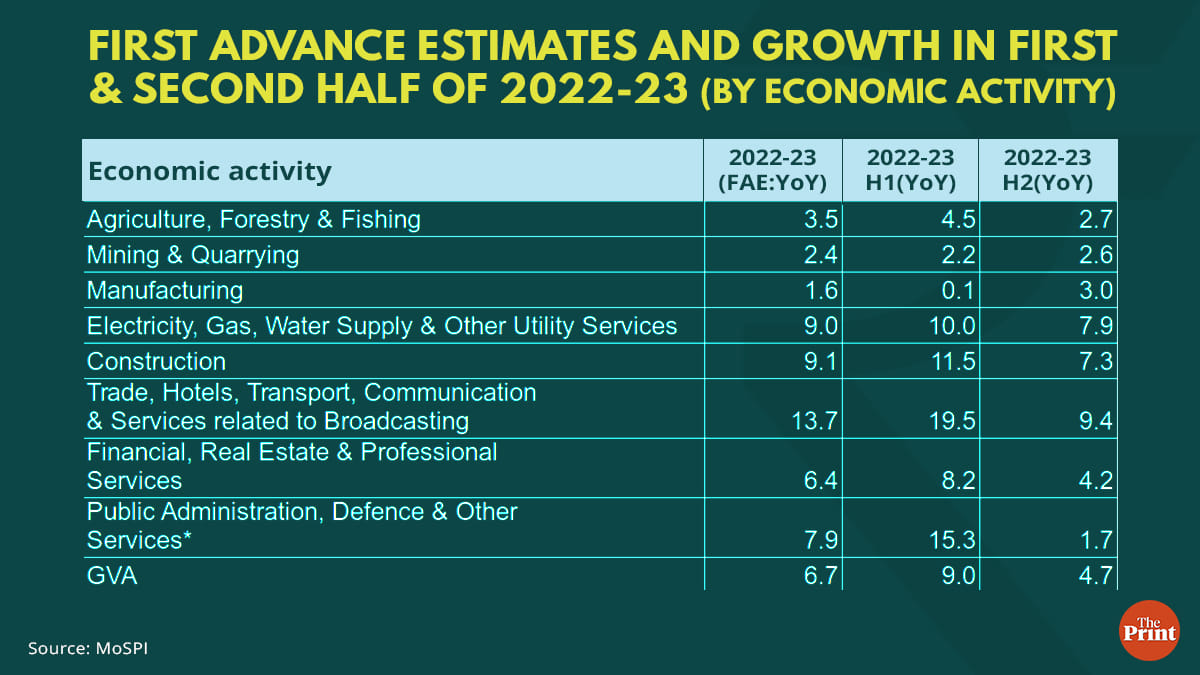

Sector-wise analysis shows a buoyant recovery by the services sector. The manufacturing sector output is estimated to decelerate due to high input prices and weak external demand. In the coming months, moderation in commodity prices will likely provide support to the manufacturing sector but weak external demand will continue to pose a drag.

The NSO has already estimated India’s GDP to have grown by 9.7 per cent in the first half of 2022-23. These numbers seen in conjunction with the advance estimates for the full financial year imply that the GDP growth in the second half of the year would moderate to 4.5 per cent. This is expected as the favourable base effect seen in the first half of the year will fade in the second half.

Also read: Why India’s critical textile sector, employing 4.5 crore people, is facing challenges

Domestic consumption demand recovering but uneven

Private final consumption expenditure (PFCE) is estimated to grow by 7.7 per cent in 2022-23. Its share in GDP is estimated to rise to 57.2 per cent as compared to 56.9 per cent in the previous year. However, high-frequency indicators are showing mixed signals.

While the Index of Industrial Production (IIP) for consumer goods remains muted, passenger car sales, personal loans, GST collections indicate strong consumption demand. Indicators of rural demand have been witnessing tepid growth due to high inflation and uneven monsoon.

The first half showed a robust growth of 17.2 per cent in PFCE. The second half of the year is likely to see a contraction in consumption. This is again due to the high base of the second half of the previous year which saw a spurt in consumption due to pent-up demand.

Investment showing encouraging signals

Investment measured by Gross Fixed Capital Formation (GFCF) recorded a growth of 11.5 per cent in 2022-23. While government capex has been the prime driver of investment, private sector investment is also showing initial signs of a pick-up. According to a survey by Federation of Indian Chambers of Commerce and Industry (FICCI), the average capacity utilisation in the manufacturing sector is above 70 per cent, which signals sustained economic activity in the sector.

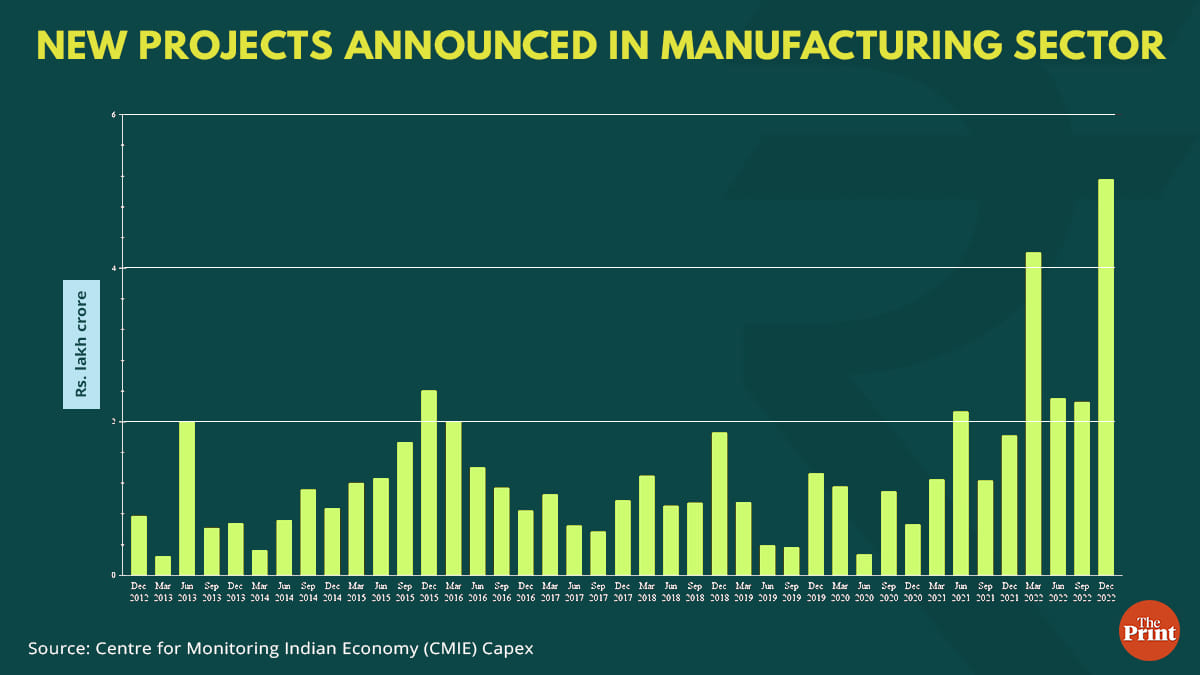

According to the Centre for Monitoring Indian Economy (CMIE), new projects worth Rs 6 trillion were announced in the December quarter. This is a 44 per cent increase compared to the previous year.

New projects announced in the manufacturing sector touched an all-time high in the December quarter. This shows that the intent to invest has improved. The actual implementation of projects has also seen improved traction in the three quarters of the current financial year. However, the trajectory of private investment in subsequent months will depend on the global environment, inflation and monetary policy response.

Manufacturing sector shows subdued growth

Manufacturing sector is estimated to register a weak growth of 1.6 per cent in 2022-23 as against a growth of 9.9 per cent in the previous year. The sector suffered on account of high raw material prices and weak external demand. In fact, in the first half of the current year, the manufacturing sector grew by a meagre 0.1 per cent.

One of the key proxies for the manufacturing sector performance is the IIP. The IIP has shown a reasonable growth of 5 per cent during April-November of the current year. The dip in the performance has been due to squeezing of margins of manufacturing sector firms due to high inflation and high interest costs. Thus, while output growth is still reasonable, the value addition in the manufacturing sector has been hit due to low profits and high costs.

The moderation in commodity prices seen in the recent months is expected to provide some support to the sector, which is likely to see a growth of 3 per cent in the second half of 2022-23.

Also read: November saw a drop in inflation but some major states missed out. Here’s why

7% growth may be revised

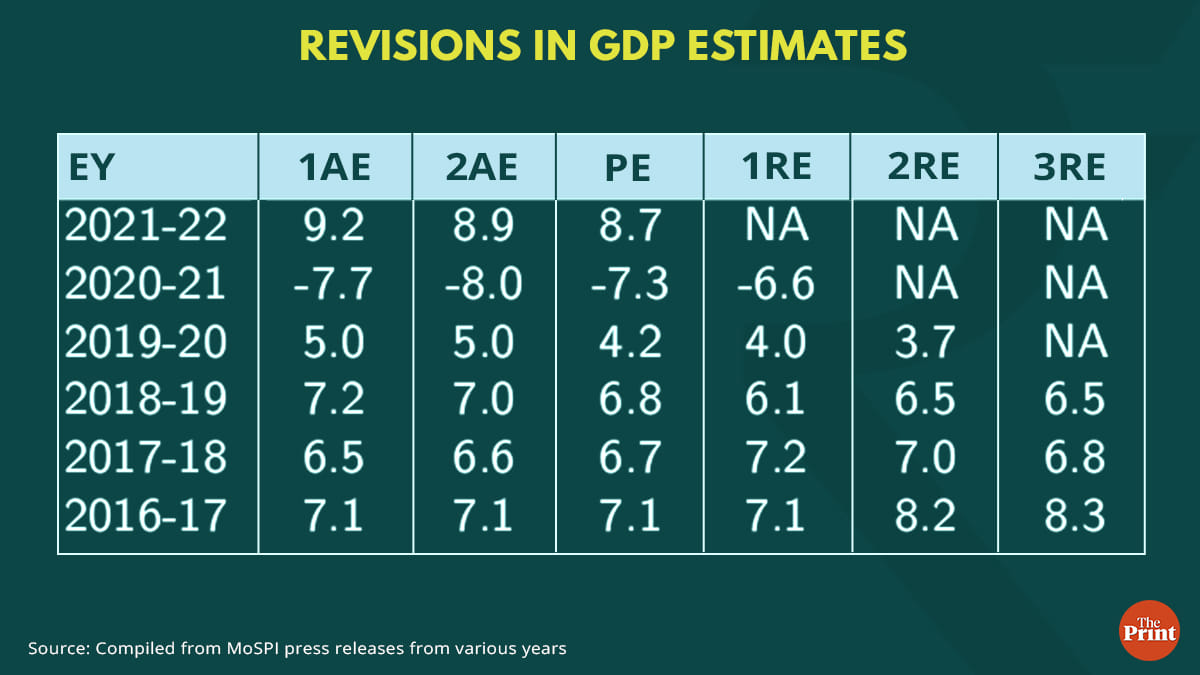

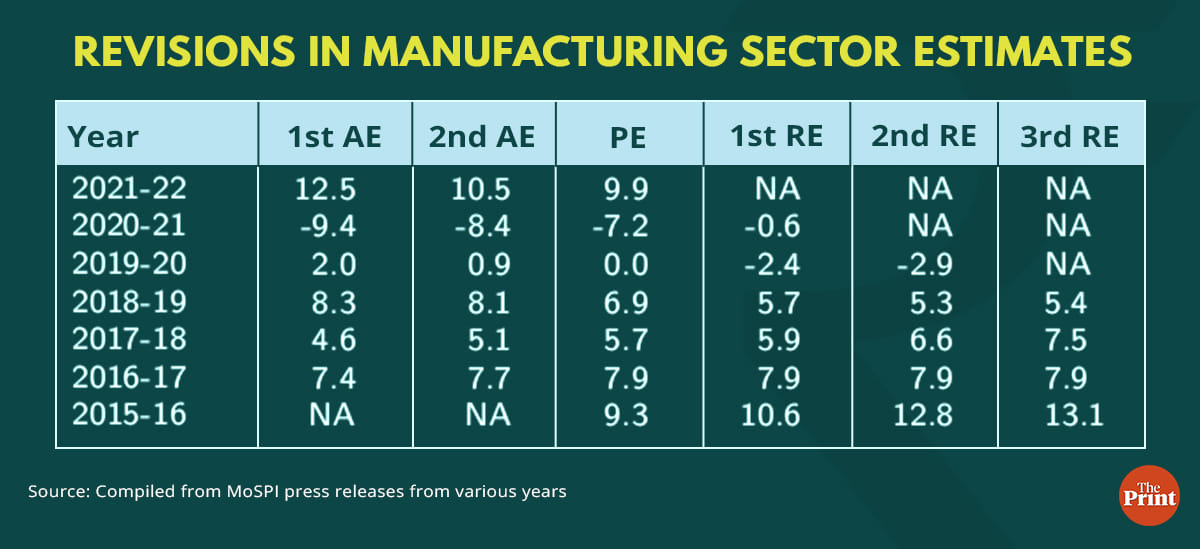

While the 7 per cent growth for 2022-23 looks encouraging, in all probabilities it will be revised. The NSO provides six estimates of GDP for any given year over a period of three years. The initial estimates are called the Advance Estimates (AE – First and Second) and Provisional Estimates (PE). Over time, the initial estimates are revised and are sequentially termed the First (1st RE), Second (2nd RE) and Third (3rd RE) Revised Estimates.

While the initial GDP estimates may be more useful as they are available within a shorter time span, a clearer picture of the economy may emerge with the release of the REs.

With each release, the GDP estimates see a revision. For instance, for the last year, 2021-22, the first advance estimates pegged GDP growth at 9.2 per cent; with the release of the second advance estimates, this was revised to 8.9 per cent. The provisional estimates scaled down the growth to 8.7 per cent. The first revised estimate scheduled to be released next month could see further revision in the GDP for 2021-22.

In some years, we see sharp variations between the initial and the final release. For example, for 2018-19, the first advance estimates pegged growth at 7.2 per cent. By the third revised estimates, the growth came down to 6.5 per cent.

Revisions at the sectoral level are even more striking. For 2019-20, the first advance estimates pegged manufacturing sector GDP growth at 2 per cent. The Second RE estimated a contraction of almost 3 per cent in manufacturing GDP. Such wide variations make the assessment of the growth performance of the economy challenging.

Inferences and policy responses based on the 7 per cent growth estimate should therefore be substantially qualified with the possibility that this number could undergo significant revisions in the subsequent releases.

Radhika Pandey is Senior Fellow and Pramod Sinha is Fellow at National Institute of Public Finance and Policy.

Views are personal.

Also read: How India’s economy fared in a year of shocks, aftershocks & slowing global growth