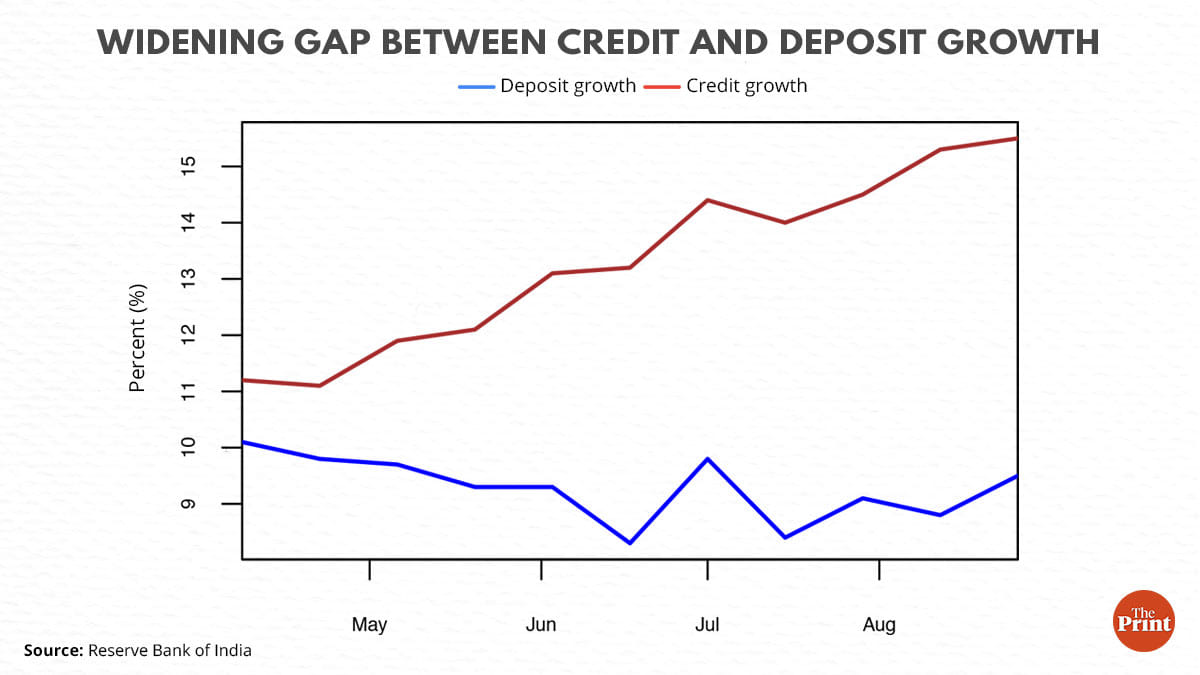

Bank credit growth surged to a nine-year high of 15.5 per cent (year-on-year) for the week ended 26 August. On a month-on-month basis also, credit growth showed an expansion. There has been a broad-based growth in credit demand despite rising interest rates.

While the retail loan growth has been going strong for some months now, the recent pickup in credit by industries — particularly for the large industries — bodes well for India’s economic outlook.

The robust credit growth should sustain amidst the onset of the festive season. However, the slow growth in deposits and the rise in inflation and interest rates could slow the growth of credit.

Also Read: Why volatile food prices will keep the heat on India’s consumer inflation level this year

Composition of bank credit

Data on the sectoral composition of bank credit is available at a monthly frequency. The latest data shows that bank credit to industry accelerated to 10.5 per cent in July. In July 2021, credit to industry had slowed to 0.41 per cent.

Within the industry, while credit to micro & small, and medium industries has shown consistent double-digit growth, the encouraging feature has been the revival in credit to large industries. Credit to large industries, which was languishing until May, showed a growth of 5.2 per cent in July. In July last year, credit to large industries had contracted by 3.8 per cent.

Credit growth to the services sector improved to 16.5 per cent in July from 3.8 per cent a year ago. Contact-intensive services are reviving as the effect of the pandemic has waned. This is likely to have contributed to an increase in credit demand from the services sector. The strong growth in credit to services was contributed by credit to “NBFCs” and to transport operators.

The personal loans segment continued to grow at a robust pace of 18.8 per cent in July. The sharp growth in the segment was driven by loans for consumer durables (69.8 per cent), housing (16.2 per cent), and vehicle loans (19.2 per cent).

Deleveraging cycle and revival of credit demand

One of the fallouts of the pandemic was the phenomenon of deleveraging (repaying loans) in the corporate sector. As investment activity slowed down amid an uncertain environment, many companies started reporting a reduction in their outstanding debt.

To be sure, the tendency to deleverage was not just an outcome of the pandemic but a phenomenon that got a push post the Asset Quality Review (AQR) in 2015-16. The Reserve Bank of India conducted an AQR with a view to cleaning up the balance sheets of banks. Banks were nudged to recognise non-performing assets (NPAs) on their balance sheets.

As an outcome, banks came under pressure due to the ballooning of NPAs. Several companies were taken to bankruptcy courts by the banks for failing to pay their debt. As an outcome, companies thought it prudent to repay debt and avoid debt-fuelled growth.

Bank credit to large industries remained tepid till a few months back as industries were on a deleveraging spree. According to an analysis by the State Bank of India, 1000 listed companies from 15 sectors reported more than Rs 1.70 lakh crore of debt reduction in the pandemic year 2021. This was despite a period of low-interest rate regime.

Deleveraging prevented an explosion of debt at a time when demand and investment conditions were muted.

In contrast, US companies were borrowing heavily at low interest rates. When Covid-19 pandemic triggered a recession, companies didn’t pull back. They continued to borrow at low rates. By the end of March 2021, corporate debt surged to USD 11 trillion. This phenomenon was seen in most of the advanced economies.

According to the IMF’s Global Debt Database, global debt rose by 28 percentage points to 256 per cent of the Gross Domestic Product in 2020. Debt surges amplify vulnerabilities as and when financial conditions begin to tighten.

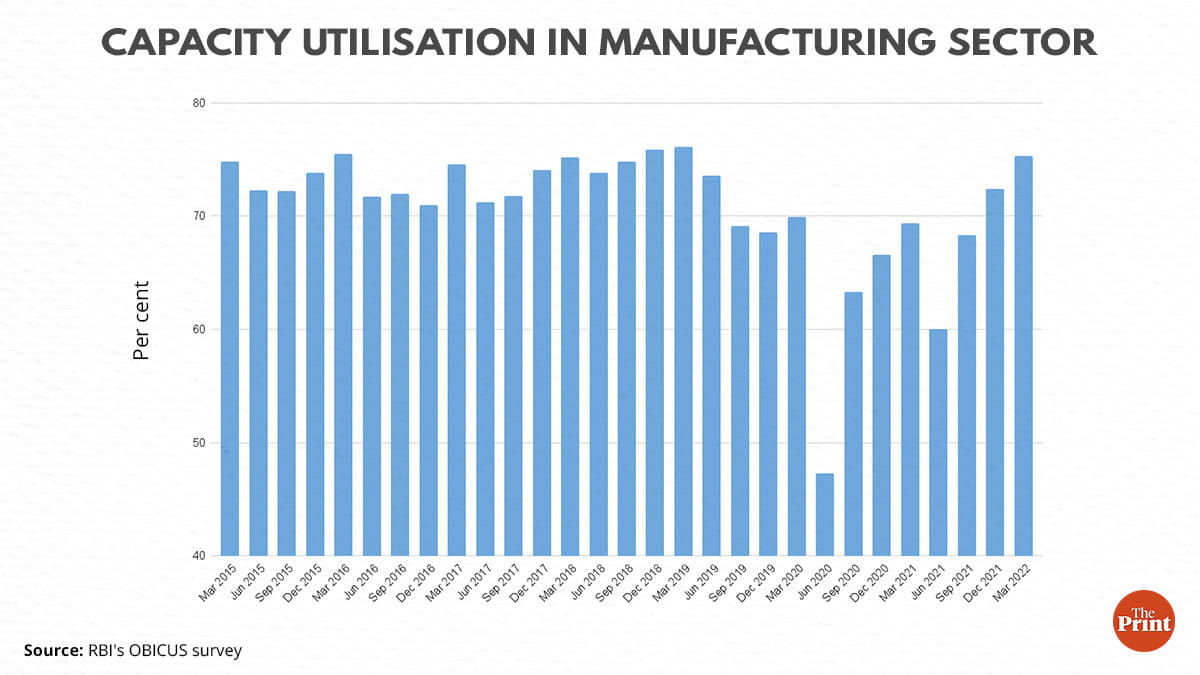

As the deleveraging cycle has ended, industries have started to borrow. Banks’ NPAs have also moderated significantly. According to the RBI governor, capacity utilisation at around 75 per cent in the manufacturing sector is now above its long-run average. This signals the need for fresh investment towards additional capacity creation.

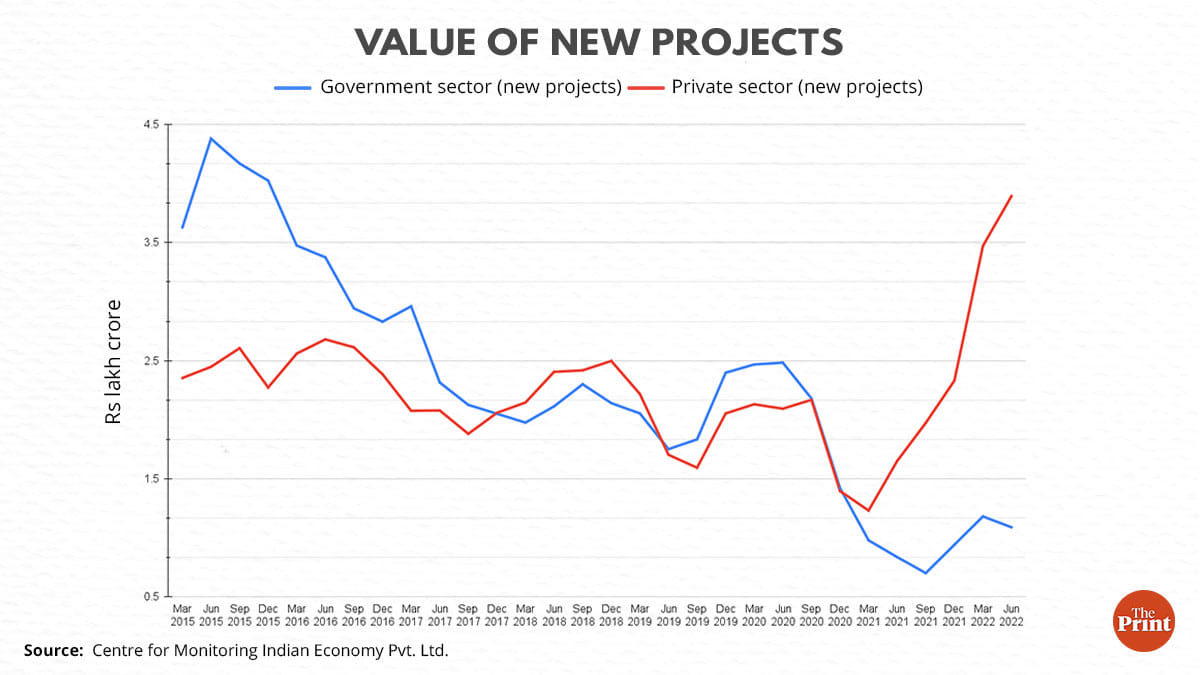

There are initial signs of a pick-up in investment activity. One way to look at the state of investment in the economy is to look at the project-level data. The nominal value of new projects announced has seen a sharp improvement in the last two quarters (March and June 2022) with more than Rs 12 lakh crore worth of new projects announced. In the last two quarters of the calendar year 2021, new projects worth Rs 7 lakh crore were announced.

Deposit growth needs to pick-up

Deposit growth has been trailing credit growth. The latest data shows deposit growth at 9.5 percent. Slow deposit growth could constrain robust credit growth. Banks will have to increase deposit rates to incentivise greater deposit mobilisation. Many banks have started special deposit schemes over the past month, offering more than 6 per cent interest on fixed deposits.

Another challenge in the way of sustained credit growth is the liquidity situation in the banking system. Liquidity in the banking system has slipped into deficit mode for the first time in over three years, signalling a shift to tight financial conditions. On 20 September, the RBI had to infuse liquidity worth Rs 218 billion into the banking system. Banks, which were until now parking funds with the RBI, are now borrowing from it under the Marginal Standing facility (MSF) window. Banks are also raising funds through Certificates of Deposits (CDs).

The RBI will have to infuse liquidity through different tools to ensure a steady flow of credit. Going forward, the rise in inflation and interest rates could also pose a threat to credit growth.

Radhika Pandey is a consultant at National Institute of Public Finance and Policy.

Views are personal.

Also Read: Why consumer confidence is on the rise in India & how this optimism can be sustained