")

- Global debt passed $300 trillion in 2021, the Institute of International Finance says.

- This covers borrowing by governments, businesses and households, and the International Monetary Fund warns that it is at dangerously high levels.

- Covid-19 led to unprecedented borrowing and now the war in Ukraine is pushing global debt even higher.

- Low-income countries and households suffer the most from high debt levels, experts warn.

Borrowing was already surging before the pandemic – but COVID-19 and now the war in Ukraine have pushed global debt to new highs.

Countries need to work together to tackle this debt mountain in order to safeguard global stability and prosperity, the International Monetary Fund (IMF) warns.

“In the end, the impact will be most sharply felt by those households that can least afford it,” it adds.

So what is global debt and why does it matter?

What is global debt?

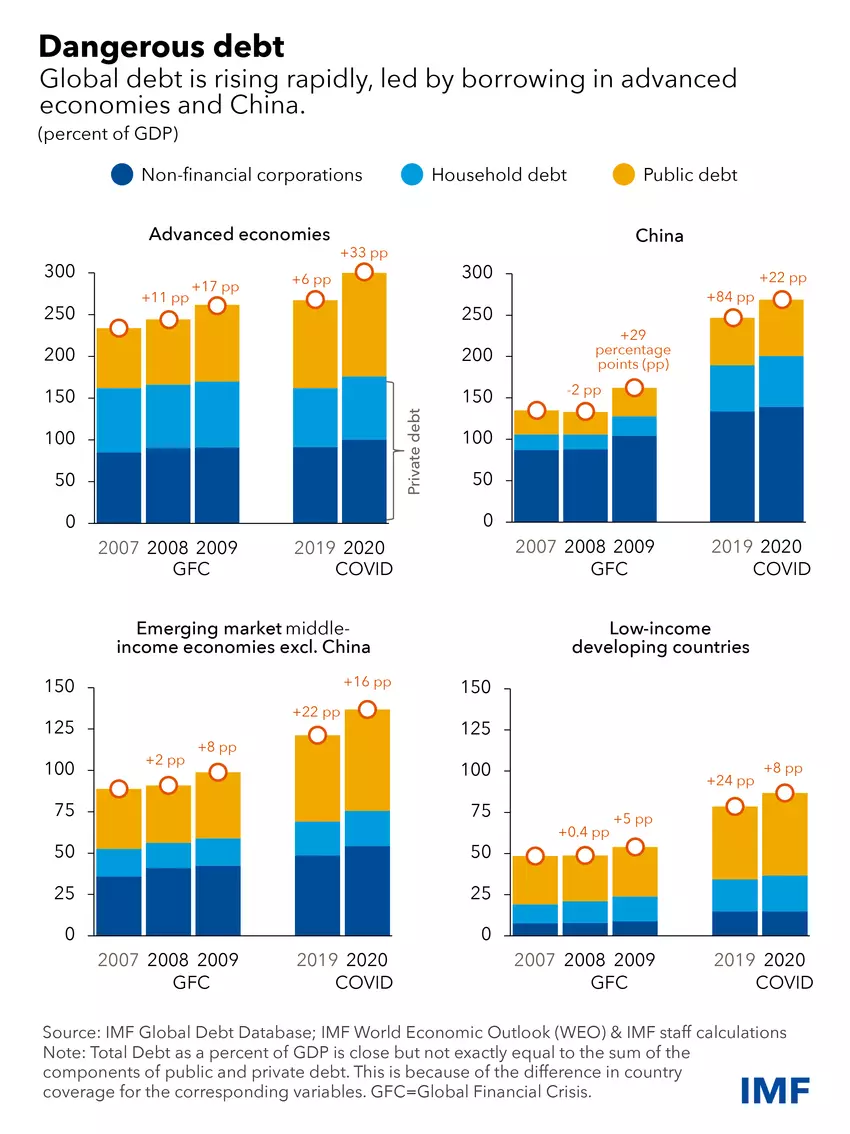

Global debt is borrowing by governments, businesses and people, and it’s at dangerously high levels.

In 2021, global debt reached a record $303 trillion, according to the Institute of International Finance, a global financial industry association.

This is a further jump from record global debt in 2020 of $226 trillion, as reported by the IMF in its Global Debt Database. This was the biggest one-year debt surge since the Second World War, according to the IMF.

According to @WorldBank’s latest International #Debt Statistics 2022 report, many developing countries entered 2020 in a vulnerable position, with public and #externaldebt already at elevated levels. https://t.co/QrlPFDIcvO #IDS2022 pic.twitter.com/zkqDRkJjcZ

— World Bank (@WorldBank) October 12, 2021

Covid-19 caused high spending on measures to protect jobs, lives and livelihoods. “Now the war in Ukraine is adding risks to unprecedented levels of public borrowing,” the IMF warns in a blog.

The current debt wave is the world’s fourth since 1970, the World Bank says.

Why does global debt matter?

Emerging and developing economies have been the worst hit by previous debt crises, World Bank research shows.

To meet debt payments, at least 100 countries will have to reduce spending on health, education and social protection, the IMF estimates.

If countries default on their debts, it can cause panic on financial markets and economic slowdowns.

For businesses, meeting repayments on high levels of debt can mean less money is available to invest in jobs and expansion. Insolvency is also a risk for businesses that are unable to pay back their loans.

For households, high levels of debt can force them to cut some areas of spending, such as food or fuel. Low-income households are most at risk, the IMF says.

What do experts say about global debt?

When low-income countries get into debt distress, it’s associated with “protracted recessions, high inflation and fewer resources going to essential sectors like health, education and social safety nets, with a disproportionate impact on the poor”, the World Bank says.

Debt distress is when a country is unable to fulfil its financial obligations, such as repayments due on its debt. The IMF and World Bank believe 60% of low-income countries are at or near this point.

At a time when the war in Ukraine is disrupting food supplies and pushing food prices higher, countries that “strain to pay their creditors will also struggle to help their poorest citizens”, Al Jazeera reports.

As food and fuel prices soar, governments may need to give more grants to households in need to help them cover costs, particularly in low-income countries, the IMF says.

In 2021, the countries with the highest global debt levels compared to GDP were Japan (257%), Sudan (210%), Greece (207%), Eritrea (175%) and Cape Verde (161%), according to data published by Visual Capitalist.

Rising prices mean inflation is spiking, so central banks are increasing interest rates to try and contain this. Rising interest rates in turn mean higher loan repayments.

The most highly indebted governments, households and firms will be hardest hit by significant interest rate rises, so countries have to be careful to strike the “right balance”, the IMF warns.

Victoria Masterson, Senior Writer, Formative Content

This article was originally published in the World Economic Forum.

Also read: Why India should pull Sri Lanka out of China’s ‘debt trap’ and take it closer to the US