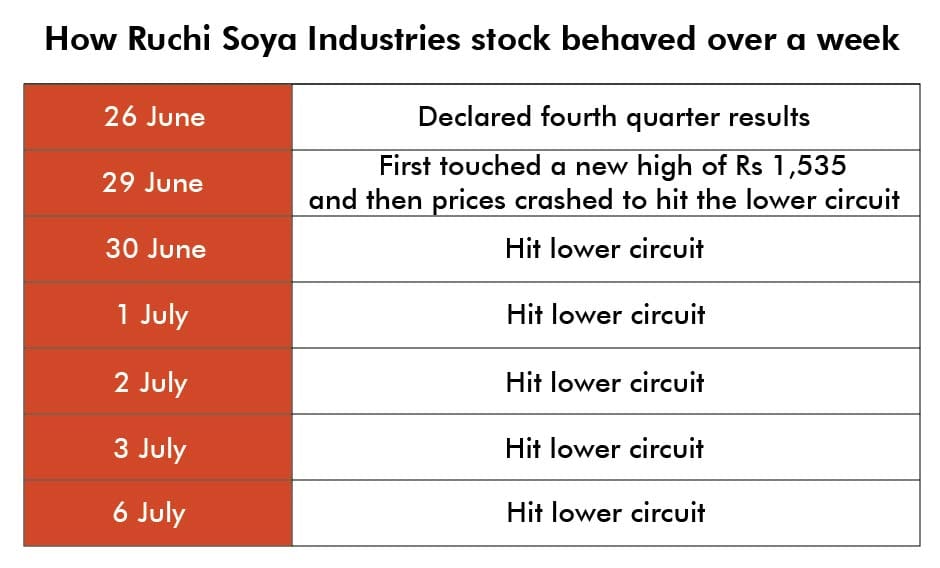

New Delhi: A leap of 8929 per cent in five months of relisting after insolvency, and then a steep fall for six consecutive trading days — the stock movement of Baba Ramdev’s Patanjali Ayurved-acquired Ruchi Soya Industries has left markets perplexed and raised questions over leeway to firms that have come out of the insolvency process.

On 27 January, the day the edible oil maker relisted after Patanjali acquired it under the provisions in the Insolvency and Bankruptcy Code, the Ruchi Soya share price was at Rs 17. It skyrocketed over the next few months to touch Rs 1,535 on 29 June — a jump of 8929 per cent.

The market cap of this lesser-known firm also rose to over Rs 45,000 crore last week. The sharp increase in Ruchi Soya’s stock price came at a time the benchmark Sensex fell 11 per cent over the last five months.

But since 29 June, the stock consistently fell by 5 per cent for six consecutive days, triggering the lower circuit — the levels where trading activity in a stock are suspended following a sharp fall in share prices — on six trading days until Monday.

In all, the stock price has crashed by 28 per cent since it touched its record high on 29 June. The stock closed at Rs 1,108.20 on the Bombay Stock Exchange (BSE) Monday.

Also read: World economy that took elevator down faces steep stairs back up

The shareholding issue, leading to volatility

Analysts point out that the rise in Ruchi Soya’s stock price was mainly on account of the low level of free float or the percentage of the shares with the public. This is also adding greater volatility to the price movements.

BSE data shows that of the total 29.58 crore equity shares, the promoters owned 29.29 crore shares or 99 per cent. This left only about 1 per cent with the public. The low level of public shareholding has also translated into low trading volumes for the stock.

According to existing listing guidelines, companies have to ensure 25 per cent public shareholding. However, since Ruchi Soya Industries was relisted following the resolution process, the promoters have 18 months to raise the non-promoter shareholding to 10 per cent and 3 years to take it to 25 per cent.

Such high levels of promoter shareholding also led to speculation that Patanjali Ayurved, a private unlisted company, may be considering a reverse merger with Ruchi Soya, a claim that the latter denied as factually incorrect in a disclosure to the stock exchanges.

A reverse merger is a situation where a private company could take over a publicly listed company thus indirectly listing itself without undergoing the lengthy process of an initial public offer.

Acharya Balkrishna is the chairman and managing director of Ruchi Soya. Yoga guru Baba Ramdev is a board member. Both are also the founders of Patanjali Ayurved, a company that posted revenues of more than Rs 8,000 crore in 2018-19.

ThePrint reached Patanjali Ayurved for a comment but there was no response until the time of publishing this report.

Also read: How Indian factories are trying to overcome labour shortages as economy reopens

The company financials

Ruchi Soya Industries reported a loss of Rs 41 crore in the quarter ended March 2020 and total revenues of Rs 3,190 crore — the first quarterly results after the acquisition. The results were announced on 26 June and since then the stock has seen a downward slide.

At the time of announcement of the results, the company said the pandemic has impacted capacity utilisation at its plants due to unavailability of labour and transportation as well as procurement of packing materials. However, it expressed confidence of recovering its trade receivables.

Ruchi Soya Industries, a company which sells edible oil and soya products under some popular brands like Mahakosh, Ruchi gold and Nutrela brands, was delisted in November 2019, about two years after the insolvency proceedings against the company were initiated in 2017 by the lenders.

The sale transaction was completed in December 2019 and Patanjali Ayurved paid Rs 4,350 crore to take over. The company was relisted in January this year.

However, existing shareholders of Ruchi Soya got only one share for every 100 shares held in the newly formed entity.

Also read: Refining industry enters ‘age of consolidation’ with ‘catastrophic’ margins

What the analysts say

J.N. Gupta, founder, Stakeholder Empowerment Services, a proxy advisory firm said, “The problem is that the case has come out of NCLT (National Company Law Tribunal) and the company is allowed to relist even if there is one share with the public. But this causes a problem of liquidity. No one knows what is going to be the future course of the company and hence there is a lot of speculation.

He said, “Added to it, there is a demand supply mismatch and there are no valuation metrics available.”

He pointed out that as of date, any company that comes out of the insolvency process is like a black box with no clear picture about its present financial position or the plan of the promoters.

“All such stocks should not be allowed to be traded until an information memorandum akin to a prospectus is put in the public domain so that the public can make an informed decision. In addition, the time limit to increase the public float should be curtailed,” he added.

Kris Capital director Arun Kejriwal pointed out that the appreciation in value of shares is not as high as the value suggests.

When the new promoters came in, there was a reduction in capital by 99 per cent as for every 100 shares held, an investor got one share. So the increase in price is not as substantial if one considers that, he said.

So if the price of the share before delisting was Rs 5, the investor would not make any money till the stock’s price touches Rs 500, he explained.

He said Ruchi Soya has time to increase the public float under the law and per se there is no violation by the company.

“The current high valuation will not remain when the free float of the company will increase,” he said, adding that the new entity with its focused business of edible oil processing may be better placed than the previous entity that was a trading conglomerate.

With inputs from Himani Chandna.

Buy fear and sell greed…is the mantra of Warren buffet.. investors should use this opportunity to get into this company which has brought itself to a position higher than Marico and will soon surpass HUL..with the hardworking base of babaji and acharyaji

Worst media page.. They make up all things against bjp and hindus

Upper wala na char char haath hoi tenu Kaun Shun ukhadi le ?

SEBI Exchange servilianc under ??????????

Thugs of hindustan

There is only 1% floating stock of this company. India is never short of smart guys and girls with uncanny abilities

to play with numbers. For some one who has the abiity to read deeper into the company’s stock price movements

it may not be difficult to see that the key players in this couner have long left the ground. It would be interesting

to see the auction details at the next settlement day.

The Print is left with no other news. Everyone knows Pitanjali products are good. This indian brand is making big because of the quality of its product.

A big money trail for approval of high demanded products medicine in international markets. That has not been done and price kept low on the cost + logistics+ marketing, so the system refused certification, but has to admit its an immunity booster for confusing general public. See it’s results when used in huge lots.

Why we not give permission to baba sand covid19 peshant at Patanjali Yogpeeth and teel to baba couqre this porson and take parmission