With the US and Israel bombarding Iran, the surge in oil prices brings to mind the inflationary energy shocks of the past half century. But that may be the wrong way to think about what’s unfolding in the economy today.While the 1970s and 2022 shocks supercharged US inflation, a sustained conflict with Iran would primarily hit the American economy through slower growth. Modern central bankers know to look through supply-driven energy price volatility when adjusting policy rates, and rising bond yields suggest that markets may be misjudging the Federal Reserve’s reaction function. In fact, today’s Fed policymakers are likely to understand the growth-dampening effects of the war on a brittle labor market, and geopolitical developments are unlikely to lead to policy rates that are higher for longer.

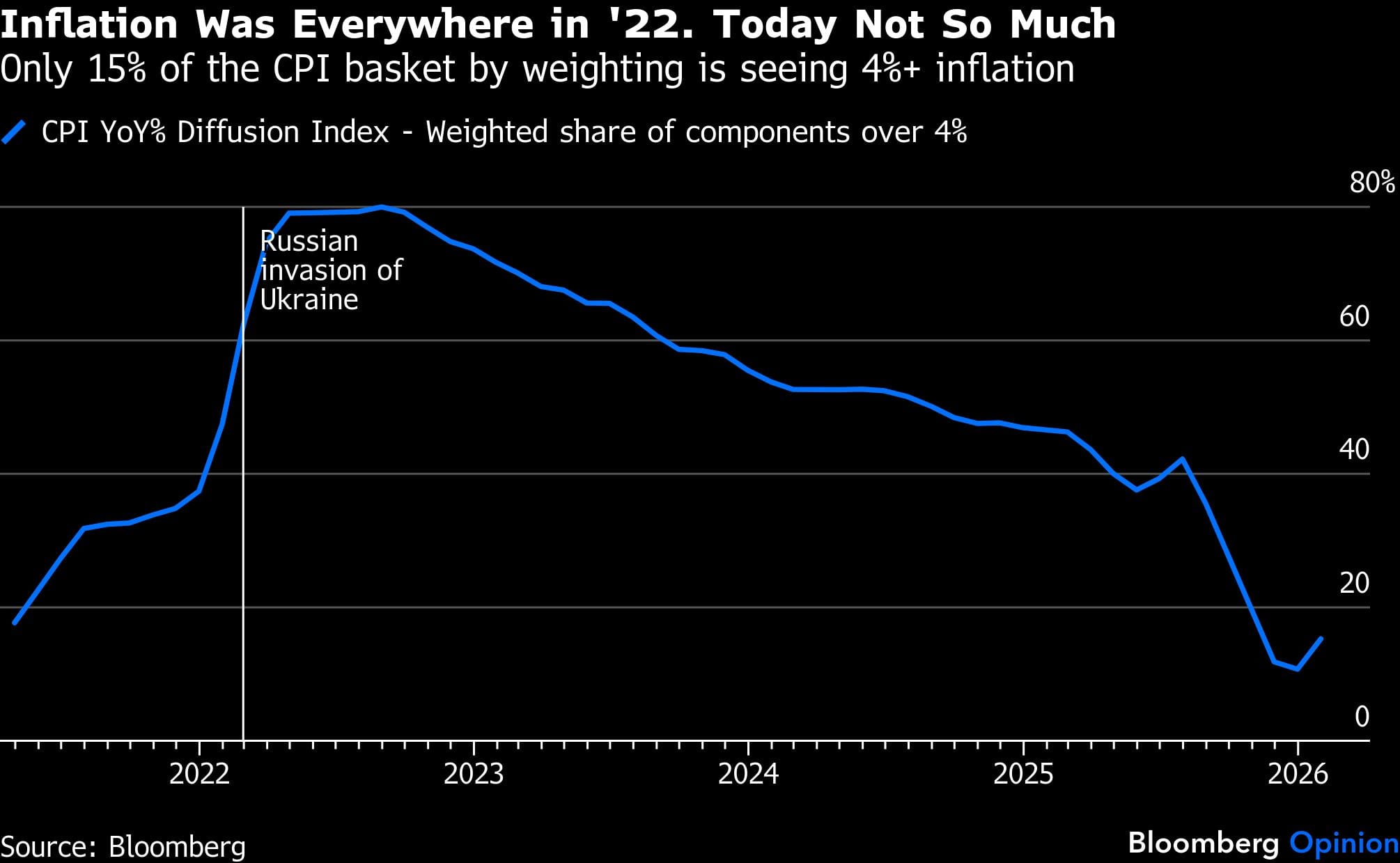

First, consider the inflation backdrop. The energy price spike comes against subdued inflation pressure in the rest of the consumer price index. Only about 15% of the CPI by weighting is currently inflating at a pace of 4% or more. The same statistic was at 62% when Russia invaded Ukraine in February 2022. Although pump prices are still among the most salient in household inflationary psychology, consumers aren’t likely to experience the shock as part of a broad increase in the price level. And while high prices have become a persistent complaint, inflation expectations have been relatively well-anchored in recent quarters, as measured by swaps and consumer surveys.

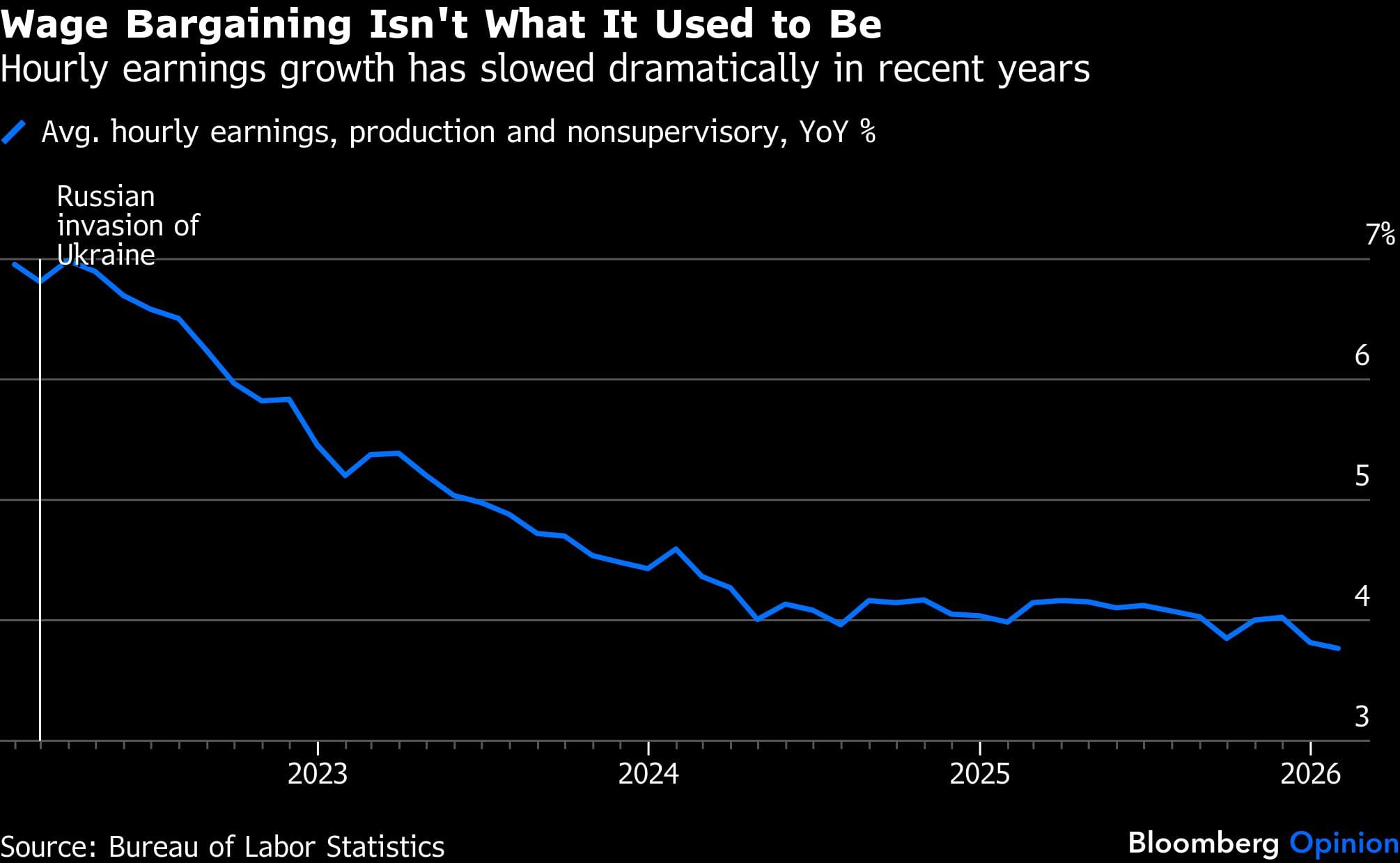

Similarly, labor market slack is primed to act as a disinflationary force. Not only is the unemployment rate higher than it was during the last energy shock, but job openings have also plummeted and payrolls growth has flatlined in just about every industry outside of health care. Whereas higher pump prices led workers to demand higher wages in 2022, they have no such bargaining power today. Average hourly earnings for production and nonsupervisory employees grew at a modest 3.8% in January. In February 2022, when Russia invaded Ukraine, they were growing 6.8%.

The story is more concerning for growth and workers. Businesses lacking the pricing power they’ve enjoyed in years past may adjust to higher energy prices by shrinking payrolls. Worse, the proliferation of artificial intelligence may give them the pretext to do so, a growing concern after Block Inc. laid off close to half its staff this week ostensibly due to technological progress.

Household finances are also more tenuous than in the recent past. The effective rate on outstanding mortgage debt sits at 4.24%, the highest since early 2012, and debt service ratios are at the highest since early 2020. Student loan, credit card and auto loan delinquencies have all moved higher, too. In such an environment, current Fed Chair Jerome Powell (and Fed chair-nominee Kevin Warsh) should know that the Fed mustn’t let a supply shock draw it into an unduly tight policy stance.

The outcome, of course, all depends on the extent to which the Third Gulf War affects the flow of vessels through the Strait of Hormuz. As my colleague Javier Blas wrote Tuesday, the US needs to get the strait reopened. While much of the conversation centers on export shipments, Javier says that the world also pressingly needs to get ships into the Persian Gulf, lest the region run out of storage and have to resort to slowing production. As an example, Iraq has already cut output at the Rumaila oil field, and Bloomberg News reported that the country appears poised to shutter about 3 million barrels a day of output if the conflict carries on.

But even under a more pessimistic scenario in which oil shoots above $100 a barrel, it seems somewhat odd for investors to bet on tighter-for-longer policy rates. At the time of writing, trading in Fed funds futures suggest diminishing odds that the central bank will cut rates twice in 2026. It’s plausible, of course, that policymakers may opt to stand pat while they monitor to ensure that inflation expectations don’t lose their anchor, since inflation is seen as a self-fulfilling prophecy. Yet that would be a temporary posture. What’s harder to comprehend is why investors have pared bets on rate cuts for late 2026 and early 2027, after the growth drag has hit.

All told, that sort of interpretation treats the 2026 shock too much like the more inflationary ones from the past. And under the surface, it’s clear that this is a very different economy.

This column reflects the personal views of the author and does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Jonathan Levin is a columnist focused on US markets and economics. Previously, he worked as a Bloomberg journalist in the US, Brazil and Mexico. He is a CFA charterholder.

Disclaimer: This report is auto generated from the Bloomberg news service. ThePrint holds no responsibility for its content.