")

Mumbai: Prashant Kumar, who completed his tenure as the Managing Director and CEO of YES BANK on 5 April, is a deeply satisfied man. After a career spanning 42 years, mostly with the State Bank of India (SBI) where he started out as a probationary officer in 1983, he is looking forward to a happy retired life.

His last assignment was, after all, among the most arduous of his career. It was a never-seen-before experiment in Indian banking to resurrect a broken bank, protect its employees and depositors, and get back on its feet, all through the thick of the Covid pandemic and the associated lockdown.

YES BANK had started going under from about 2018 weighed down by mounting bad debts, regulatory violations and dwindling deposits due to a collapse of customer trust.

It was pieced back together by a cast of characters that has largely gone unsung—Kumar, veteran banker Sunil Mehta, chartered accountant Atul Bheda and consultant Mahesh Krishnamurti, along with two independent directors each from the SBI and the Reserve Bank of India (RBI) on the board.

The government stepped in to save a private sector bank (PSB), designed a reconstruction scheme led by the SBI along with other players—HDFC, Axis Bank, Kotak Mahindra Bank, Bandhan Bank, Federal Bank and IDFC First Bank. It got the best industry brains on the bank’s board, which with all unanimous decisions revived YES BANK.

The shareholders saw their money severely diminished, but not a single depositor was impacted. Customers were angry, even violent at times, and employees got dejected and anxious, but the management and the board worked together—the management working inside out, and the board outside in—to script one of the greatest success stories in Indian banking.

“This is the only bank across the globe which has gotten back on its feet with the same brand name as it was before. Otherwise, all others have either perished or merged,” YES BANK Executive Director Rajan Pental, who was a member of the senior management when the bank was in the thick of the crisis, told ThePrint.

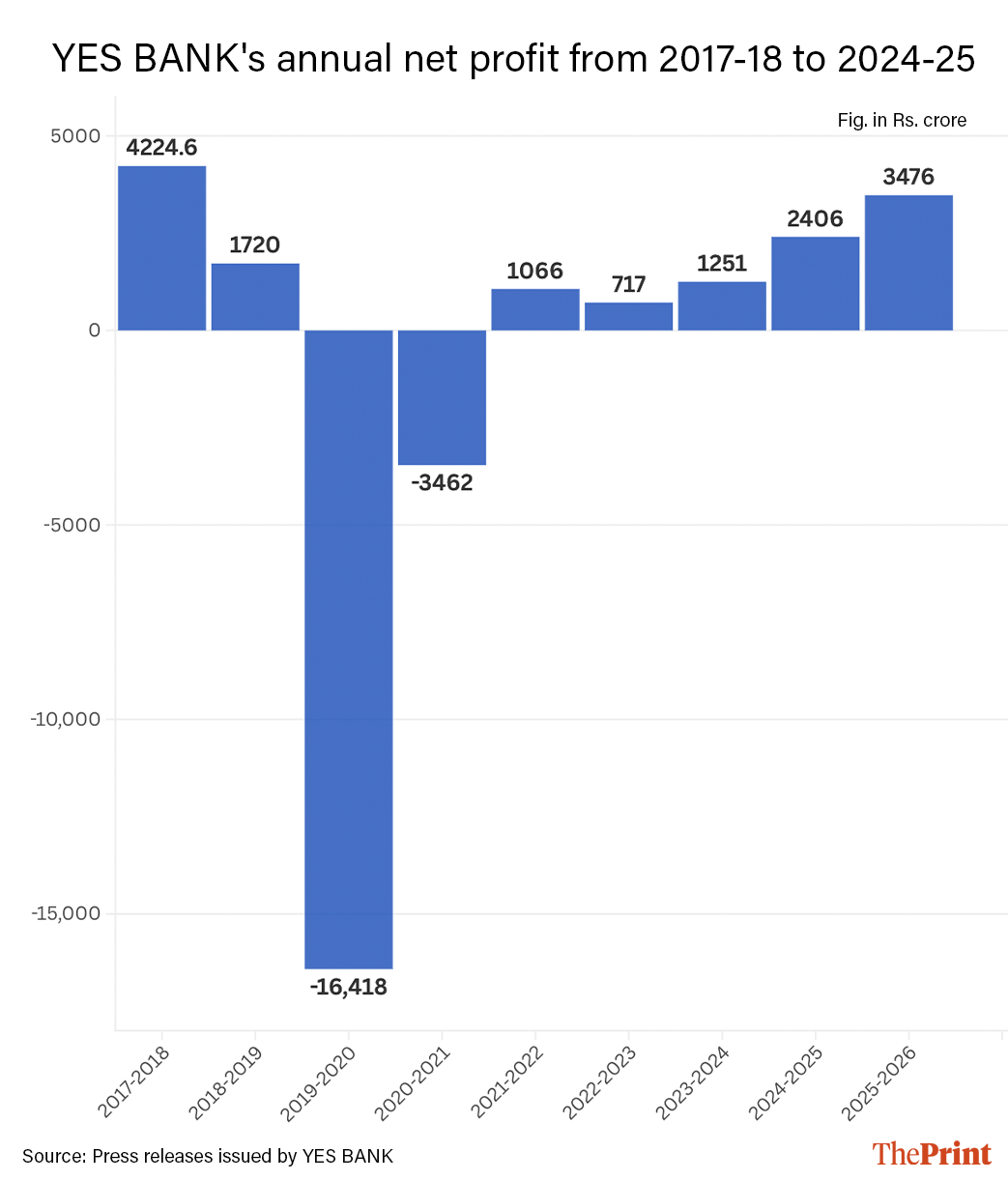

According to the bank’s latest results, its net profit for the fiscal 2025-26 was Rs 3,476 crore, up 44.5 percent from a year ago. At the end of the fourth quarter, the capital adequacy ratio (CAR)—an indicator of a bank’s capital strength against its risk-weighted assets—was 15.3 percent.

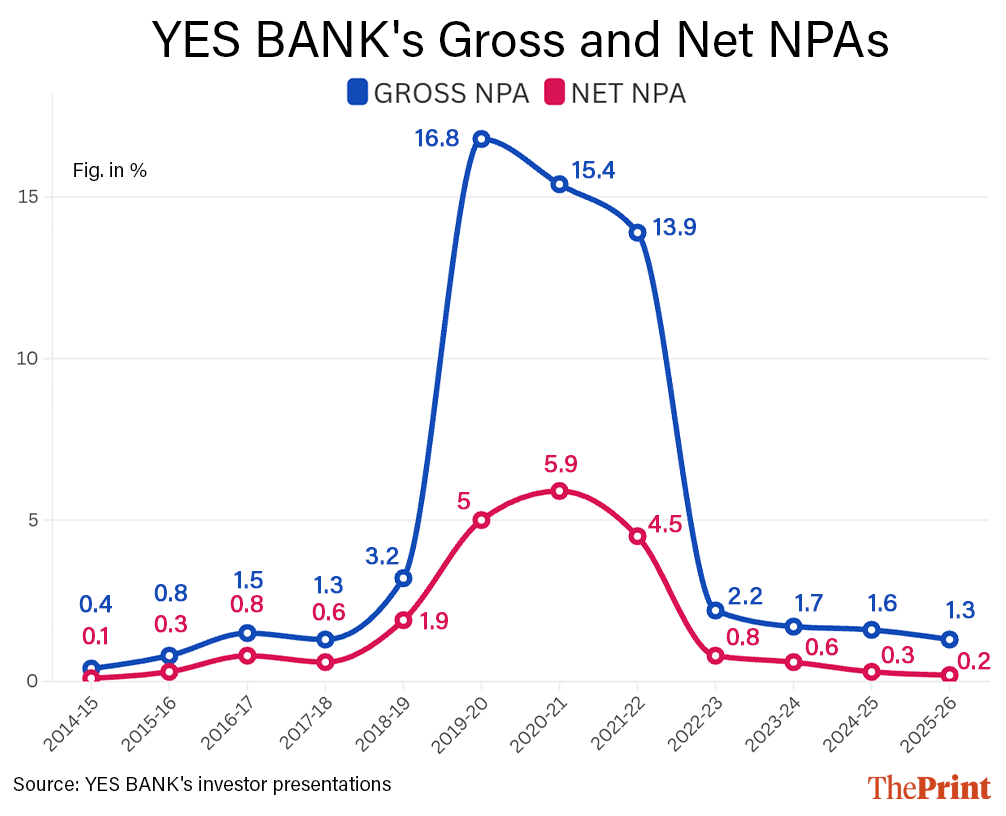

Private banks, the RBI guidelines stipulate, need to maintain the ratio at 9 percent on an ongoing basis. In the quarter ending 31 March, 2020, the CAR had slipped to 8.5 percent. The latest results—for the fourth quarter of 2025-26—show that gross Non-Performing Assets (NPAs) have fallen to 1.3 percent compared to 16.8 percent at the end of fiscal 2019-20.

Net NPAs have dropped to 0.2 percent from 5 percent in the same period. In the quarterly earnings call on Saturday, YES BANK’s new MD & CEO Vinay Tonse said the NPAs were the lowest in the last 24 quarters.

The Liquidity Coverage Ratio (LCR)—a measure of a bank’s high quality liquid assets—has significantly improved to 119 percent from just 37 percent in fiscal 2020.

Shaktikanta Das, the RBI governor during YES BANK’s restructuring, did not respond to calls and messages for a comment.

“We have done so many things for the very first time. We raised Rs 15,000 crore during a pandemic; we brought in an asset reconstruction company to take on a large amount of bad loans; and we have brought a global bank as a strategic investor,” Kumar told ThePrint.

In September 2025, Sumitomo Mitsui Banking Corporation (SMBC) became YES BANK’s largest shareholder by acquiring a 24.9 percent stake from the SBI and other investor banks that had participated in its reconstruction.

“It has been a very satisfying journey, because all the objectives that we had set out have been fulfilled. I am now looking forward to a happy retired life, a break after 42 years of service,” Kumar added.

He had taken charge as the YES BANK administrator on 5 March 2020 when the RBI superseded the board citing “serious deterioration in the financial position of the bank”. He then became its MD and CEO on 26 March, staying on for over six long years.

Many people, Kumar said, have suggested that he should use his retirement days to write a book on the entire experiment. “And I always joke that we are in Mumbai, the land of Bollywood. Why not a film or a TV series instead?” he said with a slight laugh.

Banking and finance, and all the jargons and decisions involved in their universe, can be dry. But, seen through the eyes of the board members who led the reconstruction from the front, the story is nothing short of a thriller.

Also Read: Drains to dividends: How Ghaziabad showed the way to cash in on green bonds, rewrite civic finance

How it all started

Sometime in March 2020, Sunil Mehta got a call, briefing about the Union government and RBI’s intention to reconstruct YES BANK, and inviting him to join the new ‘reconstruction’ board as its non-executive chairman. He was given just a couple of hours to think about it and get back with his decision.

Mehta had handled a fair share of turbulence and crisis-management at the executive and board level: he was the country head of AIG India from 2000 to 2012, including the time of its near collapse during the 2008 financial crisis, and the non-executive chairman of the Punjab National Bank (PNB) during 2017 to 2020 where he had to clean up after the multi-crore fraud involving jewellers Nirav Modi and Mehul Choksi.

“I put the phone down. I spoke to my wife and said, this is not an easy situation, but it is what it is. And she said, if you feel like doing it again, go for it, the choice is yours,” Mehta recollected.

Before he knew it, he was giving his confirmation to take up this next big challenge of being the non-executive chairman of the YES BANK reconstruction board.

“I knew that it would take up a lot of time and serious effort. It will not be easy and the credibility risks are higher than any potential upside, if we do not succeed in the complex reconstruction. But, I asked myself, was I the cause for the bank to be in this situation? No. Could I use my experience to improve it, contribute to its success and address a national issue? Yes,” Mehta said.

The veteran banker, who later went on to battle turbulence at the IndusInd Bank as its chairperson, added that a lot of what he experienced in PNB helped him to not get “overawed”.

Between fiscal 2015 and 2018, YES BANK, which was incorporated in 2003 by Rana Kapoor and Ashok Kapur, had one of the fastest growing balance sheets. Kapur was killed in the 26/11 terrorist attacks in Mumbai.

The bank had a strong growth in lending with net advances having swelled from Rs 75,500 crore in fiscal 2015 to Rs 2.41 lakh crore in fiscal 2019. The growth was, however, driven mostly by concentrated corporate exposure, with corporate banking comprising 66 percent of the total advances by fiscal 2019.

One by one, several of these large loans—DHFL, IL&FS, Essel Group, Jet Airways and those connected to Anil Ambani’s firms—faltered, leading to a crash. Between fiscal 2019 and 2020, gross NPAs surged to 16.8 percent in fiscal 2020 from 3.2 percent in fiscal 2019, while deposits more than halved from Rs 2.27 lakh crore to Rs 1.05 lakh crore.

The RBI had been raising governance issues and alleged under-reporting of bad loans since 2017. In 2018, it refused to extend the term of managing director Rana Kapoor, who had to step down by January 2019. He was arrested in March 2020 over allegations of money laundering, financial irregularities and receiving kickbacks for loans.

Kapoor spent four years in jail before getting bail in all the cases against him. His wife Bindu and daughters, Radha and Roshni, also spent some time behind bars. Kapoor, in multiple court filings, has denied allegations against him.

On 5 March 2020, the RBI took over YES BANK, putting it under a moratorium, and bringing in Kumar as the administrator.

The senior management set up a war room to handle the crisis, the third time that it was doing so since 2018-19. The first time was in 2019 when the RBI appointed Ravneet Gill in place of Rana Kapoor as YES BANK’s CEO and MD. The second time was again in 2019 when the PMC Bank collapsed, impacting the confidence of depositors.

Pental said the war rooms were set up to ensure uniformity in communication, ensure all channels whether physically or electronically had enough cash and technological limits, uniform customer outreach, compliance adherence, and regulatory reporting.

“By the third time, we had seen various things, a change of guard, the bank not being able to raise capital, so we were already trained to handle a crisis. We were doing early morning calls at 5.30-6 am to ensure there is complete institutional preparedness when the branch opens for the day. Our objective was clear: the bank should maintain a common narrative when employees speak to customers,” said Pental, who was then the head of branch banking, retail assets, the bank’s MSME and cards business.

Within 24 hours, the RBI published a draft reconstruction scheme, and a week later, a final reconstruction scheme on 13 March. SBI invested Rs 7,250 crore in the bank for a 49 percent stake.

“Dealing with the PNB case taught me a lot. It was a massive fraud in a public sector bank, you can imagine how many agencies came into the picture, the kind of pressure and public scrutiny the bank and board had to face,” Mehta said.

The challenge of reconstructing YES BANK was no different, and personally, Mehta said, it was also one that helped him separate the men from the boys in the industry, as his colleagues leveraged all their resources, contacts and networks for the success of the novel experiment.

The other two directors that the RBI named were Mahesh Krishnamurti, who was heading a global consultancy firm, and Atul Bheda, a chartered accountant. The board also included nominee directors from the SBI and the RBI.

The group had an initial informal meeting first at The Oberoi in Mumbai with members from SBI as well as the other banks part of the reconstruction process present.

And that informal meeting was the last time that the board members—Kumar, Mehta, Krishnamurti and Bheda—met in person. Little did they know then, that the next time they would get to shake hands would be when the bank had already, by and large, stabilised.

Also Read: For over 6,000 HDIL homebuyers, there is no home a decade since they invested. Hope running out too

A virtual reconstruction

The beginning itself was challenging: the Covid pandemic had struck and the board’s first meeting was shifted online. It lasted nearly 10 hours due to the urgent matters that needed immediate attention, the board members recall. And from there on, almost everything else, right from running employee accountability processes, bringing new deposits and marketing the bank to investors—was practically done virtually.

“It was like watching a soap opera unfold on your screen,” Krishnamurti told ThePrint.

“From my perspective, it was almost a full-time job, as it was for all the other members because we were in crisis mode. We had to deal with a variety of different aspects. I have vivid memories of board meetings lasting 7-8 hours, and often longer.”

Notably, Mehta, Krishnamurti and Kumar recall how not a single decision was passed with dissent. It was all about team work, they said. Members didn’t always agree with each other, but there was a genuine effort to build consensus.

“When you are in a crisis, the unanimity of the board is very important. There will always be differences of opinion—the head of audit will look at it differently, the risk management committee chair will have a different perspective, the board chairman will look at it differently. But, it is not a conflict. Board members must express independent opinions. As a board chair, you have to encourage members to come to a unified conclusion in the bank’s interest,” Mehta said.

The first major milestone for the board was its Follow-on Public Offering (FPO) in July 2020 when it raised Rs 15,000 crore, which enabled the team to tick a second milestone —return the special liquidity facility that it borrowed from the RBI. The facility was initially for three months, till June, and the RBI had already extended it by another three months until September.

“The FPO was a make or break situation for us,” Kumar said. He decided to go against the advice of merchant bankers, who suggested YES BANK should probably go for just half the amount. They had also suggested raising funds in two tranches, instead of one.

“As per SEBI regulation, if you don’t mobilise 90 percent of the amount, then the issue would fail. And if the issue fails, you can’t go to the market before six months again. And then you may not sail through,” Kumar said.

For the FPO too, the board conducted almost the entire exercise of investor engagement online. Kumar would sit in the erstwhile YES BANK office at Indiabulls Finance Centre with a very lean team of executives present with him, and attend calls with overseas investors at all odd hours—2 am, 6 am.

“We would eat khichdi every day because that was the only food that was being served to us at that time,” the former YES BANK CEO said.

There was some investor comfort given that SBI and several other strong PSBs had come together to resuscitate YES BANK with the government’s backing. And secondly, the issue was priced at as low as Rs 12 per share.

“From a normal mindset, getting a bank share at Rs 12…everybody thought, it can’t go below this. It only has to rise,” Kumar said.

The FPO had a three-day window. On the third day, at about 12.30 pm, Kumar was sitting in his office, sipping coffee and watching news channel CNBC. YES BANK was at 45 percent of the desired amount.

“My CFO came to see me, and he said, how are you able to sit here and sip coffee when we are nowhere close to our target and there are just a few hours for the markets to close. In a lighter vein, I said, ‘we have done what we could, now what can we do other than sitting back and sipping our coffee’?” Kumar recalled.

Then at about 3.25 pm, five minutes before the markets closed, there was a flash. The issue was successful. Kumar and the entire board felt a sense of vindication.

The YES BANK was able to raise Rs 13,700 crore, and the underwriters supported the bank on the Rs 1,300 crore shortfall. “The FPO was the second largest in the Indian capital markets. Doing so during the peak of Covid, within just three months of the reconstruction scheme, was a remarkable feat,” Mehta said.

In 2022, the YES BANK got another major capital infusion when it sold shares and warrants to private equity firms Carlyle and Advent for up to a 10 percent stake each, raising Rs 8,898 crore.

Also Read: Why one of Italy’s biggest environmental scandals is causing a stir in Maharashtra’s Ratnagiri

From bad loans to good books

It was a regular Friday afternoon at the YES BANK office in Santacruz. A few employees were mulling around in small groups with ID cards hung around their necks, and the sun, permeating through the glass structure, lighting up large parts of the spacious office building, was getting dim as early evening approached. It looked less like a bank and more like a welcoming campus with a huge lawn, greenery and abstract art.

The bank’s headquarters in Santacruz is one of its takeaways from the crisis, literally.

One of its biggest challenges for the board was to get money back from some of the large corporate borrowers who defaulted and dragged the bank down. What complicated the situation was that a significant number of these loans were from sectors such as real estate and hospitality that were stressed during the pandemic.

“Some were willing to come to the table and negotiate, some were in a genuinely difficult situation, some were recalcitrant borrowers. It was a combination of all of them, and there had to be different strokes for different folks. For some, the bank had to initiate legal action as required. It was not cowed down. The board and the management were prepared to take tough decisions without fear or favour as required,” Mehta said.

“The board also empowered the management to take tough decisions. We said we cannot take haircuts just because someone is being difficult.”

Case by case, the board and the management worked out the best possible settlements. The Santacruz headquarters was one such—a debt asset swap deal with the Anil Dhirubhai Ambani Group where the bank took over Reliance Centre, located on a 21,432 sq m plot, along with two other properties in South Mumbai after ADAG failed to repay Rs 2,892 crore.

YES BANK had said that it sought to recover the money in May 2020 and took possession of the three properties in July after the ADAG failed to repay the debt despite a 60-day notice.

At about 12 pm on 31 March, 2021, members of the YES BANK management were at the registrar’s office, getting the registration for the property done. In June 2021, the office moved. It was a renewed bank with a new headquarters.

By the end of fiscal 2021, gross NPAs were at 15.41 percent as compared to 16.8 percent a year ago. By the end of fiscal 2022, it further dropped to 13.9 percent, and the year marked the first full year of a return to profitability after fiscal 2019. YES BANK recorded a profit of Rs 1,066 crore as compared with a loss of Rs 3,462 crore a year ago.

The pool of stressed assets was so large that Kumar said he was spending 80 percent of his time in recovery and resolution, and that too wasn’t moving the needle beyond a point.

“As a bank, if you live with such a large NPAs, recovery will happen only over a period of time, but when you go to investors and you say my gross NPA ratio is like 18 percent, 15 percent, how will investors get the confidence? So, we thought why not have a transaction where this pool can be given to someone,” Kumar said.

And that’s how YES BANK agreed to offload up to Rs 48,000 crore of its stressed assets portfolio to JC Flowers (JCF) Asset Reconstruction after a rigorous bidding process. In the words of JCF CEO Chris Flowers, it was the “single-largest transaction of the sale of non-performing assets in the country’s banking system so far.”

JCF bought the portfolio for a total consideration of Rs 8,046 crore. The deal had a 15-85 structure, commonly used in asset reconstruction deals, where JC Flowers paid 15 percent of the total consideration (Rs 1,206.9 crore) upfront, and issued the remaining 85 percent in security receipts, which are essentially deferred payments. YES BANK receives payments on the security receipts only when JCF recovers money from the borrower.

“Post-acquisition, JC Flowers ARC will act as the manager for the portfolio workout to optimize recoveries, with a number of key personnel having worked on the portfolio at YES BANK. The ARC purchased a 15 percent vertical slice of the NPAs while YES BANK will retain the rest in the form of security receipts,” JCF said in a statement in December 2022, on the conclusion of the deal.

In its quarterly earnings call on Saturday, Tonse said the bank still has about Rs 1,500 crores in security receipts that can be redeemed over the next few quarters.

YES BANK also agreed to purchase an equity stake of up to 19.99 percent in two tranches, ensuring a share in JCF’s profitability. Initially, the bank acquired a 9.9 percent stake in the asset reconstruction company.

“There were two occasions when I thought that things were finally getting under control. The first was the private equity infusion. Companies had to be convinced. We had to show them the upside of what a reconstructed bank will look like. And the second was when the distressed assets were taken over by JCF, and suddenly our NPAs dropped to 2.2 percent (gross as of 31 March, 2023) from over 13 percent,” a YES BANK board member said.

Mehta had mentioned the JCF deal in his speech at the annual general meeting on 15 July, 2022, the day he stepped down from his Board Chair role on completion of the ‘rescue plan’ and made way for a new regular board.

The JCF mention was a last-minute addition in the chairman’s speech with hectic negotiations underway between the management and JCF till the eleventh hour.

“I had left a paragraph open regarding the balance sheet restructuring and the sale of stressed assets. While I was delivering my speech, someone from the management gave me a note that the sale transaction had been finally signed and executed. And so, I read that part before concluding my final chairman speech at YES BANK,” Mehta said, recalling the warm farewell he had over lunch afterwards.

Managing employees, customers

For the YES BANK management, and also its board, the biggest challenge was managing the morale of its employees and enabling them to face customers.

Pental remembers the night before the moratorium on withdrawals was supposed to be lifted on 18 March, 2020 at 6 pm.

“We started preparation in the middle of the night. A lot of people would be coming to branches—senior citizens, ladies, children. The message to all teams was to service the customers with folded hands and a smile. We told our employees that there will be situations where you will face abuse or harassment, but you have to handle them, getting into an offence would severely impact the reputation of the institution,” Pental said.

On that fateful day, there were instances of two-three branch members being attacked, glasses broken at a few places. “We were doing hourly calls at the branch levels. There were war rooms created for each zone.”

YES BANK also boosted the technological capability of its digital banking channels to ensure customers don’t get stuck. The message was, your money is safe and you can choose to withdraw it at any point of time. There won’t be a problem.

The senior management personally made calls to depositors to assure them that in the history of Indian banking, no depositor had ever lost money, and that YES BANK is being turned around and their money is safe. CEO Kumar himself was calling 10-15 customers every day.

The board and the CEO also ran a stringent staff accountability process where key employees were given a chance to be heard.

“There was a lot of finger pointing going on back then. The easiest thing for us to do would have been to let go of anybody who we thought was affiliated to some of the questionable decisions that had previously been made. But we wanted to be fair and needed the institutional knowledge to keep the plane flying. We didn’t want to throw the baby out with the bath water,” Krishnamurti explained.

“And so we took a very deliberate and mindful approach, gave specific individuals the opportunity to come to the board in a non-threatening manner, show us what they were capable of so that we could make objective assessments and evaluations.”

The bank had about 22,000 employees back then. Post reconstruction, the employee roster has grown to 29,174 as of 31 March, 2025.

Krishnamurti described how the board and the management tried to keep up employee morale, at a time when the bank was down, the economy lacklustre and the doom of the pandemic looming large.

“The board’s nomination and remuneration committee was working very closely with the chief HR officer to get a better pulse on employee morale. We sliced and diced to establish which employees needed to be full time, and how many could work hybrid or work from home. We created facilities for working from home, gave them good internet connectivity. We had to bolster cyber security and safety measures as well, VPNs had to be secured because of sensitivity of information. We created recognition awards, opportunities to hold their own townhalls,” Krishnamurti said.

Eventually, there were layoffs but it was less than five percent, he said. Generally, attrition was high due to the uncertainty. There were pay cuts and salary freezes.

During the entire period of the pandemic, Kumar was in his office every single day, and gradually, so was the top management.

In this period, the bank also had to decide what course it should take to grow, going forward. “Our challenge was to convert a largely corporate bank into a retail bank, convert lumpier deposits into granular deposits,” Pental said.

The bank launched new premium products for salaried individuals, families and small businesses such as Premia and the Yes Prosperity Family Account. Sometime in between the first and second wave of the pandemic, it also started a practice of inviting 20-30 customers to its branches, creating festivity, having the staff dress up and welcome them.

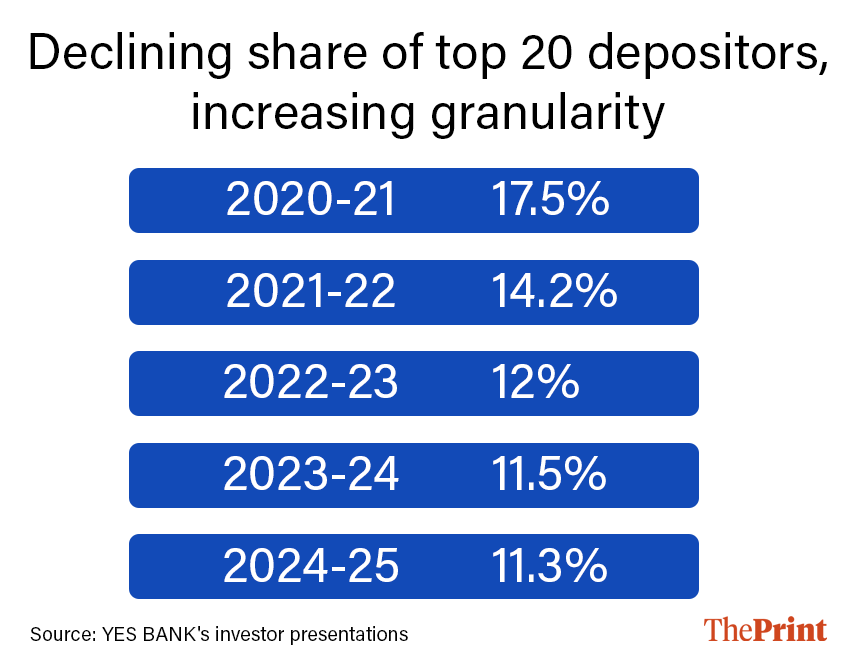

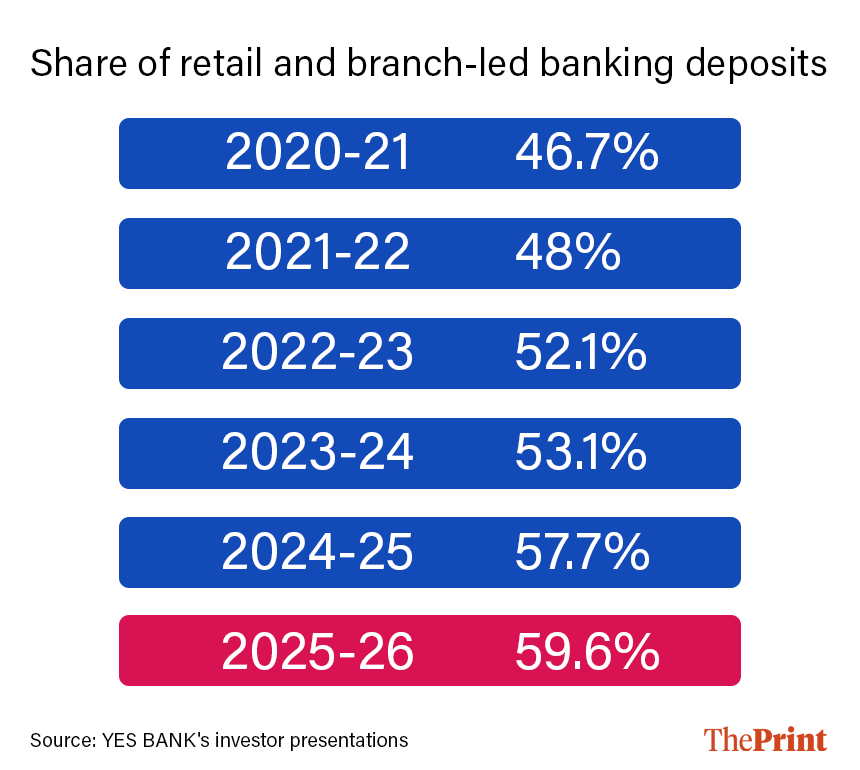

Their efforts have borne fruit. In fiscal 2021, the share of top 20 depositors was 17.5 percent. By fiscal 2025, it dropped to 11.3 percent. The share of retail and branch banking surged from 46.7 percent in fiscal 2021 to 57.7 percent by fiscal 2025.

Looking back, Pental recalls just how overwhelming day-to-day events were between fiscal 2020 and 2022. “I would often go inside my cabin and break down. But, we had all decided to never wear our anxiety on our faces. So, I would step out of the cabin, with a smile. It still gives me goosebumps, thinking of that time,” Pental said.

He remembers how cool and mature Kumar himself handled the office. “I don’t know what storms must have been brewing in his mind, but he always looked composed and had a smile,” Pental said.

On 6 April, Kumar exited with the same smile, only stronger, leaving behind a good robust bank.

Meanwhile, the Kapoors, once known for their extravagant parties and lavish lifestyle, are still battling the ghosts of the bad bank, with multiple charge sheets filed by the Central Bureau of Investigation (CBI) and the Enforcement Directorate (ED) against them.

(Edited by Tony Rai)

Also Read: Mumbai’s been driving India’s data centre market, but water shortage, power demand pose risks