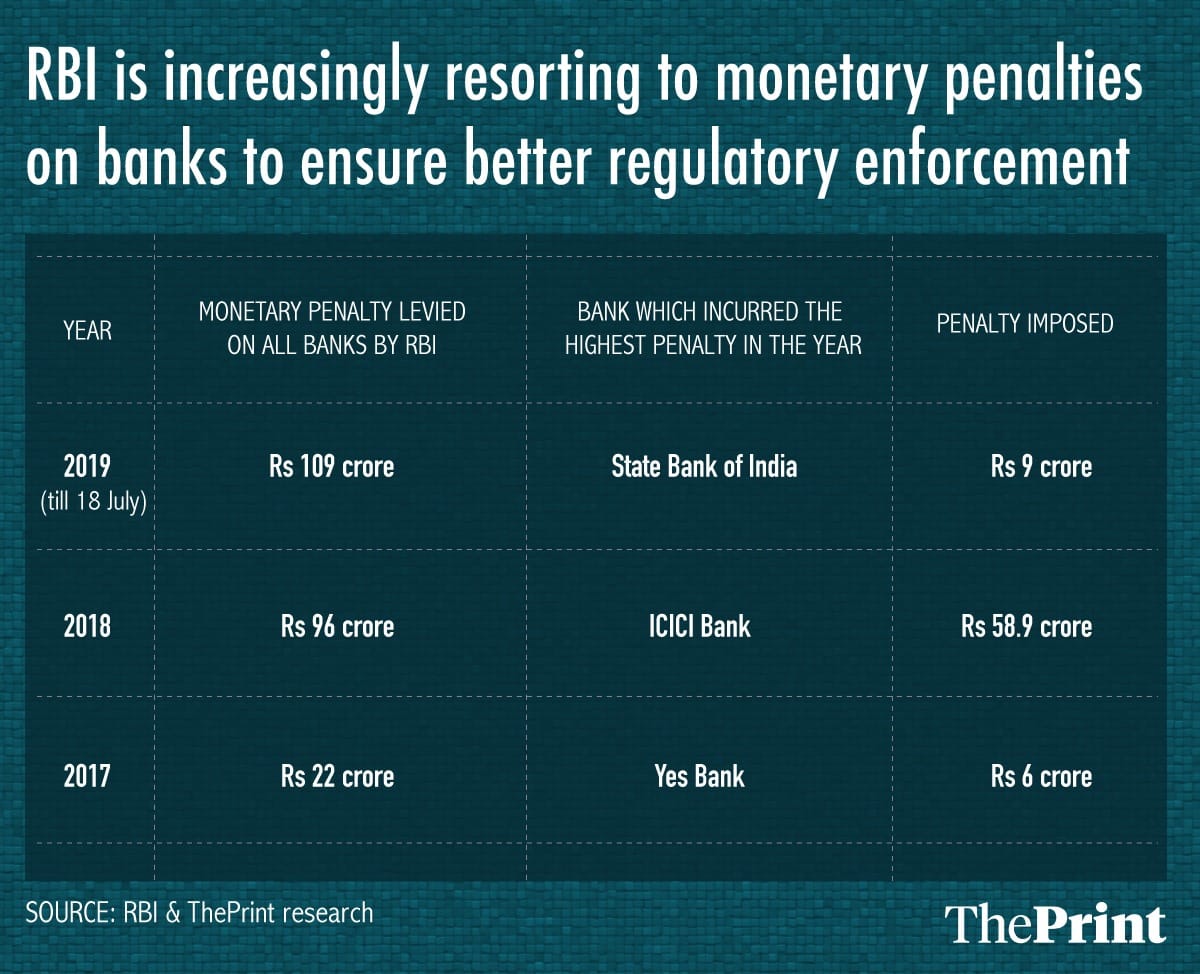

New Delhi: The Reserve Bank of India (RBI) has fined commercial banks Rs 109 crore this year for non-compliance with rules and regulations, as the central bank looks to step up enforcement and bring erring banks to task.

The penalties imposed in the seven months of this calendar year are 13.5 per cent higher than the total for 2018 (Rs 96 crore) and 395 per cent over the 2017 tally (Rs 22 crore).

This year, the RBI has penalised banks, including state-run, private and foreign, on 65 occasions for not complying with rules that deal with reporting frauds, recognition of bad debt, income recognition, and opening of current accounts, besides their failure to follow steps suggested to tighten the SWIFT system (that allows banks around the world to exchange secure communication related to intercountry money transfer instructions), among other reasons.

At Rs 9 crore, the penalties imposed on the country’s biggest state-run lender, SBI, were the highest.

The RBI penalties come at a time when the regulator’s supervisory role is under the scanner following the discovery of many frauds at banks last year, including the alleged Rs 14,000 crore swindle involving jewellers Nirav Modi and Mehul Choksi and Punjab National Bank.

Also read: Yes Bank shares drop 20% after profit misses estimates on bad loans

Worst offender

The State Bank of India has been slapped with penalties to the tune of Rs 9 crore over the year, the single-highest fine for one bank.

Of this, Rs 7 crore was imposed earlier this week for the bank’s failure to adhere to income recognition and asset classification norms, rules governing fraud risk management and reporting of fraud, and the code of conduct for opening current accounts.

The other fines came for non-compliance with directions monitoring the end-use of funds, exchange of information with other banks, restructuring of accounts, and strengthening of SWIFT-related operational controls. SBI declined to comment for this report. An email sent to the RBI remained unanswered till the time of publishing.

‘Token penalty meant to send a message’

The SBI’s total, however, is far lower than the highest penalty for 2018, Rs 58.9 crore, imposed on ICICI Bank for non-compliance with norms on the direct sale of securities from its held-to-maturity (HTM) portfolio.

In 2017, the highest fine was levied on Yes Bank, Rs 6 crore, on account of non-compliance with norms on income recognition and asset classification, and delayed reporting of information on security incidents involving its ATMs.

A source familiar with the central bank’s actions said the RBI had moved from “moral suasion” to penalties to ensure better adherence to regulations.

“The idea is to sensitise the banks that actions have consequences. The penalties levied are a token amount but seek to convey the message that regulatory enforcement is a priority with the central bank,” the source said.

“Earlier, moral suasion was the preferred method, wherein the RBI used to write a letter to the bank management to point out irregularities. But now the RBI has moved to levying monetary penalties to ensure adherence to regulations,” the source added.

An internal committee of the RBI takes decisions on levying penalties after allowing the banks to state their case and defend their actions. The time taken for the decision could vary from 3 months to a couple of years.

As part of mandatory disclosure requirements, banks have to disclose the penalties levied by the RBI in the notes to accounts of their balance sheet.

Also read: SC only quashed RBI circular on bad loans, insolvency law still hangs over private firms