")

New Delhi: Private sector investment in India has been falling as a proportion of Gross Domestic Product (GDP) since 2012, and it’s not due to the conventional reasons of consumer demand, capacity utilisation, access to credit, and corporate profitability, an analysis by ThePrint has shown.

The problem instead seems to be a more unquantifiable one — a general lack of confidence in the way the Indian economy is being managed, economists and businesspeople say.

Analysis of data from the latest Economic Survey of 2022-23 shows that private investment has exceeded investment by the government as a percentage of GDP since 1950 (except for a brief period in the 1980s).

This incidentally belies the notion that it is public sector investment that has been the mainstay of India’s economic growth, despite the huge fanfare around the Modi government’s large-scale infrastructure push.

The data also shows that, since 2012, private sector investment as a percentage of GDP has been falling.

Broadly, there are five determinants of private sector investment — consumer demand, access to credit, corporate profitability, the level of capacity utilisation, and overall business confidence. The data shows that the first four factors, while measurable, haven’t had a particularly strong bearing on private investment in India.

“The main problem, according to me, is not so much a lack of confidence in the economy, but a lack of confidence in how the economy is being managed and how companies are being monitored,” Pronab Sen, former chief statistician of India, told ThePrint.

ThePrint reached the office of the commerce secretary, ministry of commerce, for comment on why they thought private investment was low, but did not receive a response till the time of publication of this report.

Also Read: India innovates in labour. It doesn’t need the pressure to spend huge on R&D like US, Japan

Private sector drives investment in India

The data shows that private sector investment as a share of GDP rose steadily since 1991 — spurred by the economic reforms implemented then — to a peak of 27.5 per cent in 2007-08. Even the Global Financial Crisis didn’t seem to have a lasting impact on investor appetite, with private sector investment recovering from a brief dip post-crisis to 27 per cent in 2011-12.

It is since then, however, that private sector investment as a share of GDP has been steadily falling. It fell to 21.3 per cent by 2015-16. By 2020-21, the latest period for which the Economic Survey has disaggregated data for the public and private sector, private sector investment as a percentage of GDP had fallen to 19.6 per cent.

Various private databases have shown that while private sector investment has increased more recently in absolute terms, it has nevertheless remained low as a percentage of GDP.

Data from investment monitoring firm Projects Today shared with The Hindu shows that private investment hit an “all-time high” of Rs 10.5 lakh crore in the January-March 2023 quarter. However, when looked at as a percentage of GDP, this works out to just about 15 per cent of GDP.

Consumer spending doesn’t impact private investment

The conventional belief is that private sector investment is driven by demand, whether domestic or from abroad, in the form of exports.

“Private sector investment is driven by demand factors,” D.K. Pant, chief economist at India Ratings, told ThePrint. “If there is low demand, and capacity utilisation is low, then why will companies invest in more capacity? Similarly, if the export situation is sluggish, then demand from there as well will be low, and companies will not invest in new capacity.”

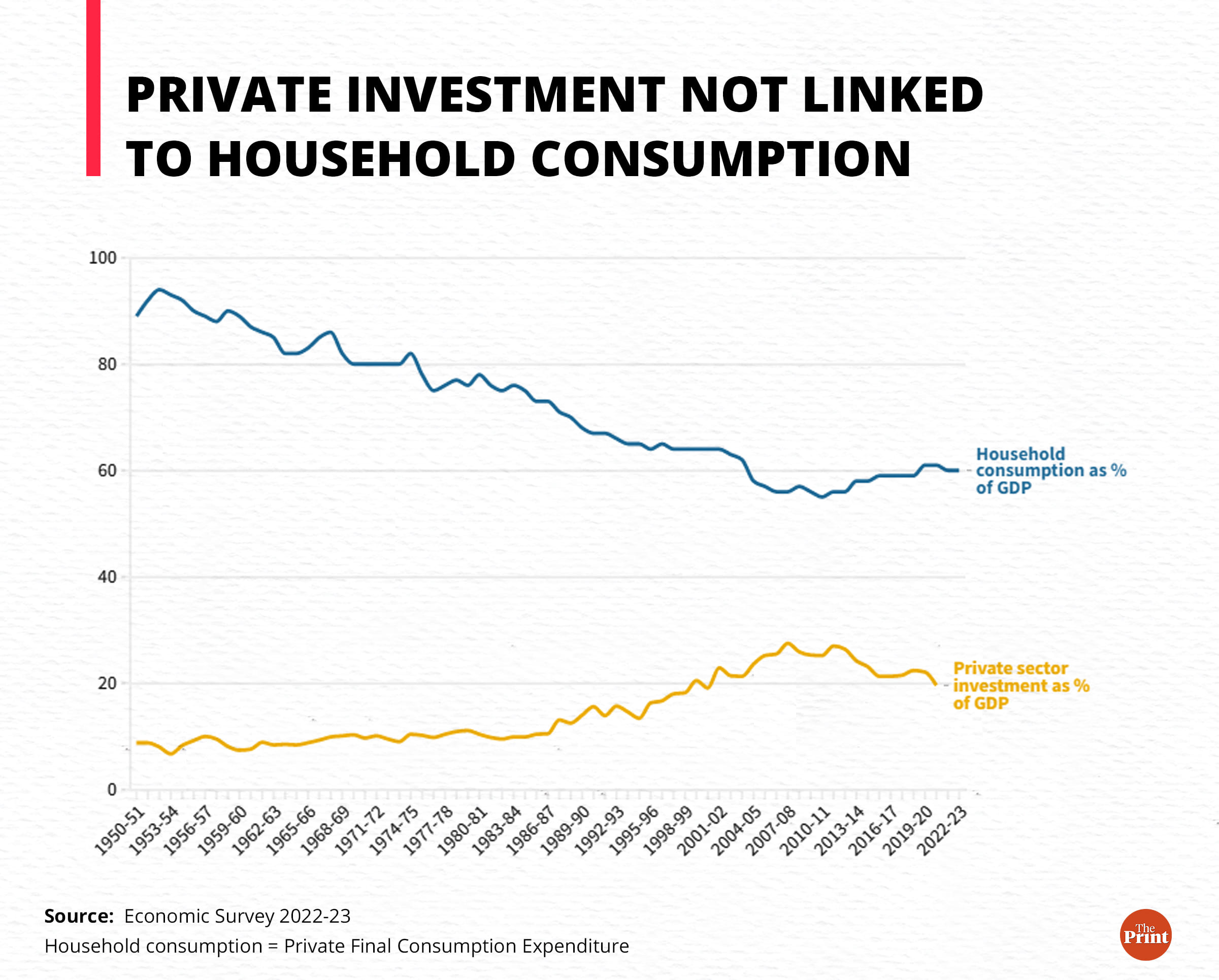

The data for India, however, shows that this doesn’t seem to be the case. Private Final Consumption Expenditure (PFCE), which is the amount households spend on consumption, has been falling as a percentage of GDP since 1950. PFCE as a percentage of GDP fell steadily to 55 per cent by 2010-11 from 89 per cent in 1950-51.

However, at the same time, private investment as a percentage of GDP rose to 25 per cent in 2010-11 from 8.8 per cent in 1950-51.

To further highlight the delinking of consumption expenditure and private investment, the next few years saw consumption expenditure rebound somewhat to 61 per cent by 2019, but this was the period when private investment was falling.

Further, although the government says that India’s exports are “projected to scale new heights”, data analysis shows that there does not seem to be a correlation between exports demand and private sector investment in India.

The analysis does, however, show that the level of capacity utilisation in the economy has a bearing on whether private sector investments happen or not. Capacity utilisation is basically a measure of the extent to which the installed capacity in a company or economy is being utilised to produce the output.

The higher the capacity utilisation, the more likely the company will invest in fresh capacity. If capacity utilisation is low, companies won’t invest in new capacity because what they have is more than enough to meet current demand.

The data shows that private investment as a percentage of GDP follows the level of capacity utilisation quite closely. When capacity utilisation is rising, private investment picks up. When capacity utilisation falls, so does private investment.

Another factor about capacity utilisation that is important to note is that it is an indication of not just current demand, but also a company’s confidence in future demand.

“If current capacity is more than enough to cater to current demand, then of course a company will not invest,” a former CEO of a large multi-thousand-crore consumer appliance company told ThePrint on the condition of anonymity. “However, a company will also invest in creating new capacity if it expects future demand to be strong, or if business conditions are positive in the country.”

“However, that is not the case right now,” he further explained. “Neither is there confidence that near future demand will be strong enough for new capacity to be needed, nor is there confidence in the way the economy is being managed right now in key business-oriented areas.”

Bank credit has no link with private investment

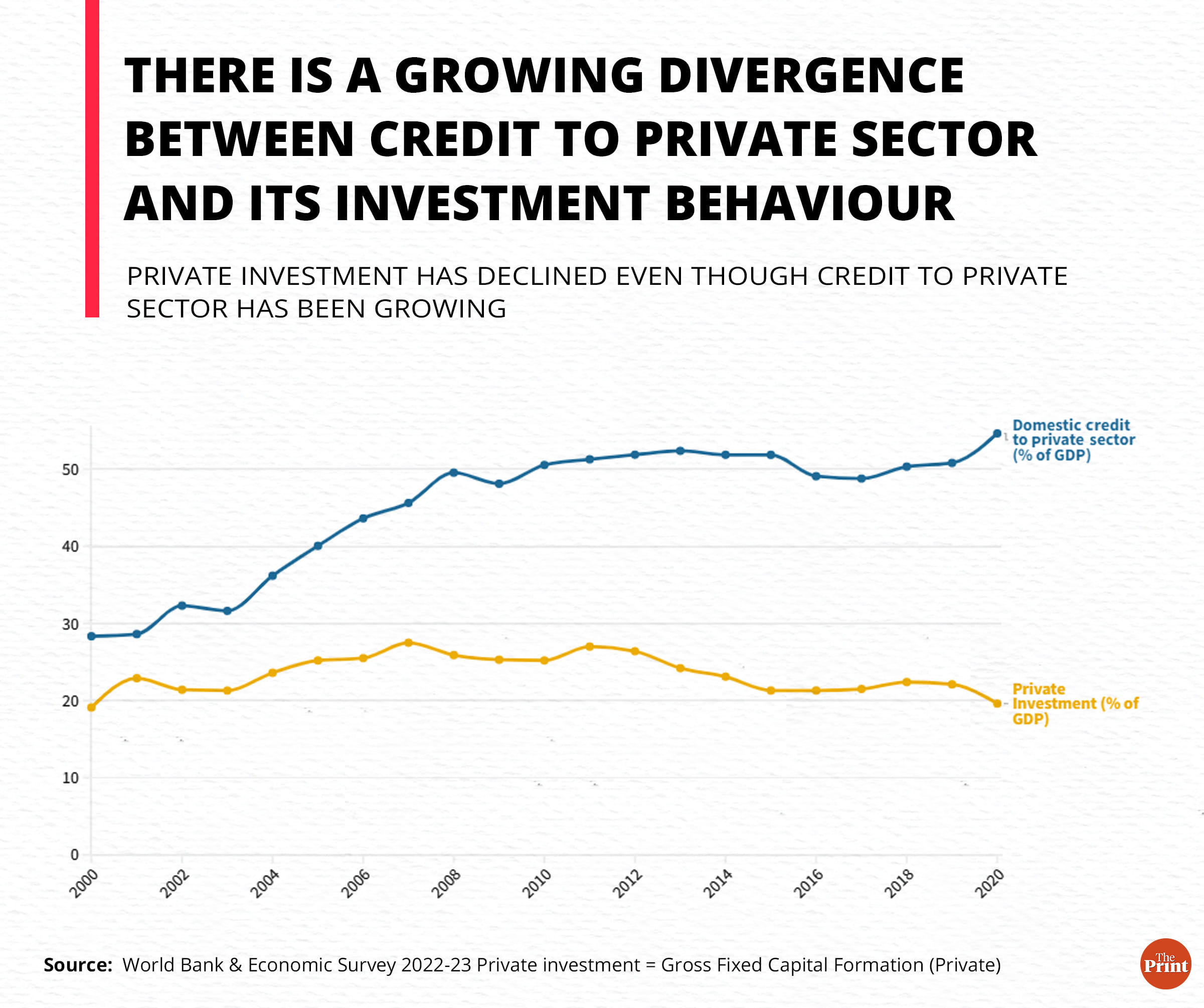

A common refrain when it comes to private sector investment is that access to credit is what drives it. That is, even if the private sector is willing to invest, if there isn’t enough credit available, then it can’t borrow enough to make those investments.

The latest Economic Survey has talked about how a “well-capitalised banking system with a low NPA (Non-Performing Asset) ratio and more robust corporate sector fundamentals will continue to enhance the flow of bank credit into productive investment opportunities, notwithstanding the rising interest rates”.

In other words, banks are in good health and companies are doing well enough, and so bank credit will increasingly fund private investment.

Analysis of the data shows that the surge in bank credit to the private sector as a percentage of GDP in the 2003 to 2008 period, from 31.6 per cent to 49.5 per cent in 2008-09, was largely accompanied by a growth in private investment as a percentage of GDP from 21.3 per cent to 27.5 per cent in 2007 — its highest ever level.

Thereafter, however, there’s been a disconnect between the two metrics. While bank credit to the private sector has increased, albeit at a marginal rate, private sector investment has dipped.

It thus seems clear that past data, at least, doesn’t show a strong link between bank credit to the private sector and investment behaviour.

The final measurable factor — of corporate profitability — also shows that it is not a major determinant of private sector investment. That is, while it is obvious that companies will not invest if they are in losses, it is not obvious that they will invest if they are in profit.

“Listed corporate profits (measured by profit after taxes, PAT) have been stable at 4.0-4.5 per cent of GDP during the past nine quarters,” a research note by Motilal Oswal Financial Services published in January 2023 said. “It has almost doubled from the pre-Covid period (FY18-FY20) average of 2.1 per cent of GDP.”

Here, too, Sen cautioned that the data could be partially misleading.

He explained that, since 2020, larger companies have been capturing the market shares of smaller companies that shut down due to the financial stresses of the pandemic. This is the reason behind their increasing profitability.

He also added that corporate profitability only looks at a part of the economy, while the profitability of about 45 per cent of the economy — informal sector businesses — is not being measured.

Tax, labour uncertainty & need for reforms

A company looking to invest requires certain things to be set, the former CEO mentioned earlier said. These include tax rules and labour laws.

“However, what we have seen is that the government promised that labour laws would be reformed, but nothing has changed on the ground,” he lamented. “Even when it comes to tax rules, a company wants tax rules to remain unchanged for at least a decade if it is going to invest. But this is not happening here. Here, they change the rules every few years, which leads to uncertainty.”

This lack of confidence has been noticed by international bodies like the World Bank as well. During the release of the World Bank’s latest India Development Update earlier this month, the body’s country director, Auguste Tano Kouame, said that government investment was “not enough” for confidence in the economy to grow.

“This will not solve the long-term issue of investment unless confidence grows,” he explained. “And confidence will grow, but to accelerate the growth of confidence, public investment is not enough. You need deeper reforms to make the private sector invest not just when it is hugely profitable for them, or not just when they have deep pockets.”

“You want the shallow-pocketed private sector to also invest and you want small firms to invest so they can grow,” he said. “There are a number of reforms that are needed for that.”

Sen added that “constant raids and harassment” by agencies like the Income Tax Department, Central Bureau of Investigation, and the Enforcement Directorate have significantly eroded the confidence of companies looking to do business in India.

(Edited by Nida Fatima Siddiqui)

Also Read: India’s FY24 growth to slow to 6.3%, says World Bank, cites US-Europe banking crisis among reasons