When it comes to shrinking the state’s role in production, the priorities of the Bharatiya Janata Party government that’s ruled India since 2014 are very different from those of its predecessor, which left power a decade earlier. And that’s something that has annoyed investors no end.

Atal Bihari Vajpayee, the BJP prime minister between 1998 and 2004, gave a colleague free rein to kick-start a Margaret Thatcher-style privatization drive, something that hadn’t been attempted in India. The government let go of what it could — hotels, aluminium and zinc firms, a bakery chain — amid strong opposition from unions and even some entrenched tycoons who preferred to compete against bungling state-owned corporations rather than other entrepreneurs.

Things that the administration failed to sell before the drive ran out of steam — such as Air India Ltd. — are a millstone around the Indian taxpayer’s neck even today. And that brings us to Narendra Modi.

Apart from a so-far unsuccessful effort to sell Air India, the current prime minister has shied from restarting the stalled privatization program, despite being much more secure politically than Vajpayee ever was. He’s even spending $6 billion on two unprofitable state-run telecommunications firms. That’s a waste of meager government resources in India’s hyper-competitive mobile market.

But last week something changed. Team Modi decided to sell the government’s entire stake in the second-largest state refiner, Bharat Petroleum Corp., as well as the largest shipping company, Shipping Corp. of India Ltd. It also approved selling a controlling 30.8% shareholding in Container Corp. of India Ltd.

The motivation is simple enough. There’s a crisis brewing in the economy, some of which has resulted from Modi’s own adventurism, such as a disastrous ban on 86% of the country’s cash to catch tax cheats. The finance industry is in a shambles. Tax collections, a full 1 percentage point of GDP lower than the 7.9% the government had hoped for last year, continue to be horrendous. Selling capital assets to shore up revenue may not be a great strategy, but hitting a 1.05 trillion rupee ($14.6 billion) asset disposal target is the only way to lower the sticker shock of the budget deficit for the bond market.

It will also cheer the equity markets. What usually pass off as state asset sales in India are either small-ticket public offers of listed government companies, or transfers of one state-run firm to another. Neither does much to make the economy more productive. Nor do they hold any excitement for investors, who’ve been waiting for an end to the drought in real privatization deals.

And what a famine it’s been. It was 17 years ago when I last wrote about how the Vajpayee government was being thwarted by some of its own ministers from selling Bharat Petroleum. Back then, the refiner’s market value was $1 billion. Now it’s $15.4 billion. Yet cashing out then to invest in education and health instead might have been a better trade for India.

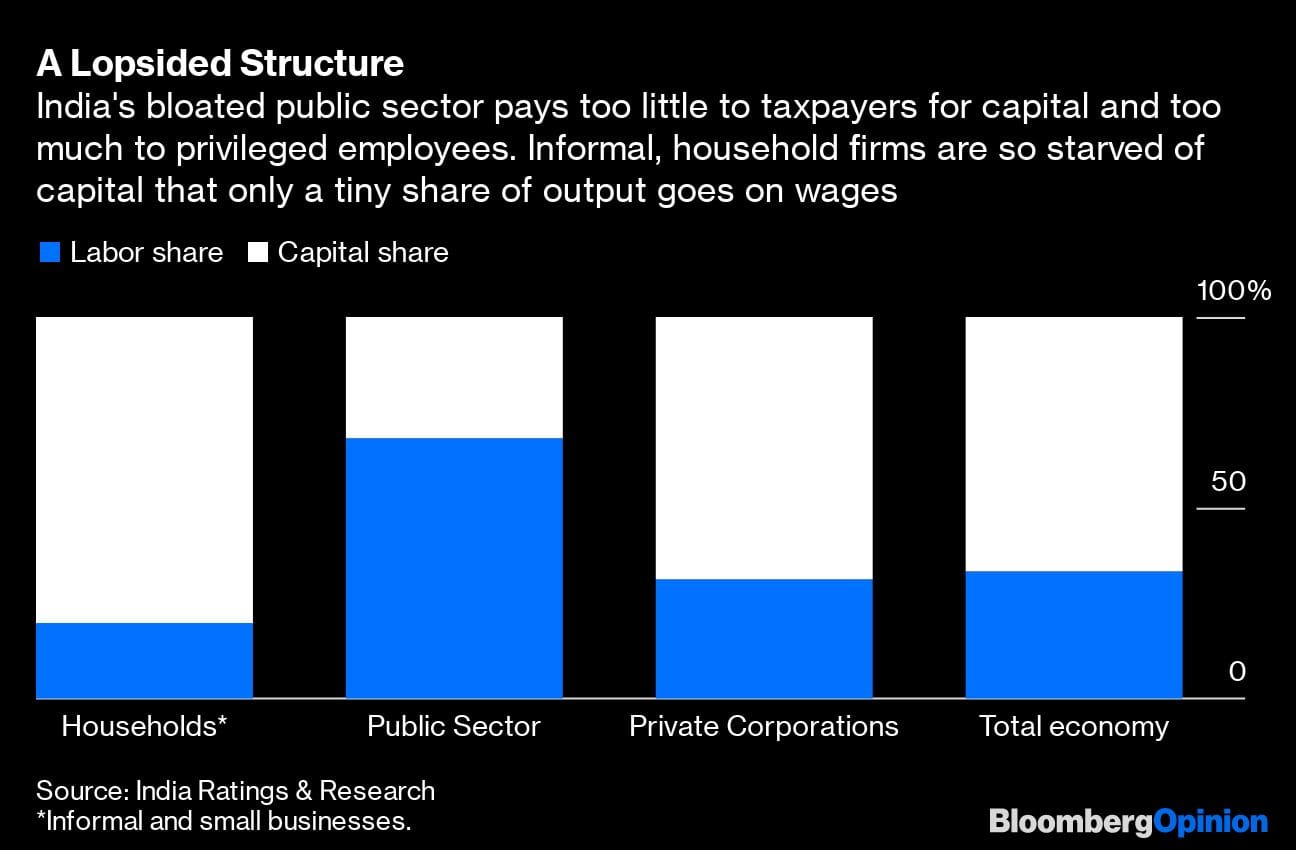

One reason the country is facing a debilitating demand funk is that the structure of the economy is lopsided. Profitable Bharat Petroleum is an exception, but overall only 32% of the output of India’s public sector goes to taxpayers and banks that supply capital; as much as 68% is pocketed by privileged employees who enjoy assured jobs and higher pay than they would in the private sector. A bloated public sector distorts the economy by trapping a vast number of Indians in informal household-level production, 80% of whose output is used to pay for scarce capital, leaving only 20% for workers.

It isn’t too late to use a combination of sales of better assets and closures of weak state firms to give the economy a permanent boost. Brokerages are speculating that Saudi Aramco, Kuwait Petroleum Corp. and Abu Dhabi National Oil Co. may be interested in Bharat Petroleum. And why not? As electric cars depress oil demand in the developed world, India will be a good dumping ground for Middle Eastern crude.

Container Corp., meanwhile, has a near-monopoly on railway freight. Bidders may include Dubai ports operator DP World Plc; Singapore’s PSA International Pte; shipping firm AP Moller-Maersk A/S’s terminal management unit; and Adani Ports and Special Economic Zone Ltd., India’s biggest private port operator.

Whatever the buyers’ reasons, as a seller India should ensure that its privatization program is both transparent and seen as fair. More importantly, it should set its sights at something more ambitious and durable than a crisis response.- Bloomberg

Also read: How Modi govt quietly repealed old laws to pave the way for BPCL disinvestment

Ha ha ha!

Obviously the writer is more an artist than an economist, but mostly a stooge of a defunct ideology. Even if we believed Demonization of a corrupted debased currency caused a 5 recession has to then explain how it also caused the same the world over! And with emptied coffers and looted banks and endemic corruption left behind by the CHALU CHA CHA’S PARTY, there’s little choice but to sell the assets!

Someone has tweeted, apprehensive that the sale proceeds of BPCL will be used to compensate the states for shortfall in GST collections. Aise toh economy nahin chal sakti.

A lot of wisdom in the last sentence.

Socialist Modi murdabad. Air India, Railways, government banks, government buses, government companies, goverment industries murdabad. Margaret Thatcher zindabad. Free market capitalism zindabad.