New Delhi: The phone rings. The woman on the other end sounds calm, but her voice has an edge. “You don’t understand my language it seems,” she says. “Maybe you will understand another language.” Another caller is openly threatening. “This loan you’re sitting on, who’s going to repay it?” she shrieks.

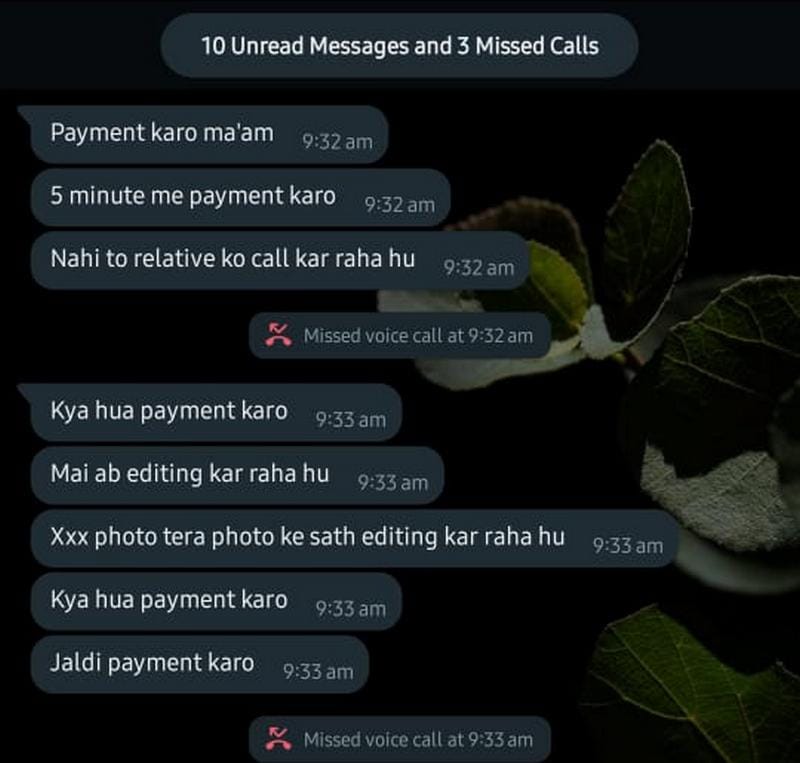

Nothing exemplifies the noxiousness of India’s loan apps more than the seven to eight calls that car broker Sumit Bhardwaj received from recovery agents within just one hour at his office in Delhi’s Badli. He put the calls on speakerphone so ThePrint could hear them.

“They torture us,” he said.

At one point, he even got a call from an irate customer. She said loan recovery agents had been asking her to repay Bhardwaj’s dues.

“I came to you to buy a vehicle. I am your customer. Why would you give my number to the loan people”? the customer asked. Bhardwaj assured her that he did not give her number to the loan app company. He claimed the app may have somehow extracted the number from his call records.

The harassment went one step further in the case of Bengaluru-based IT consultant Harish Kumar.

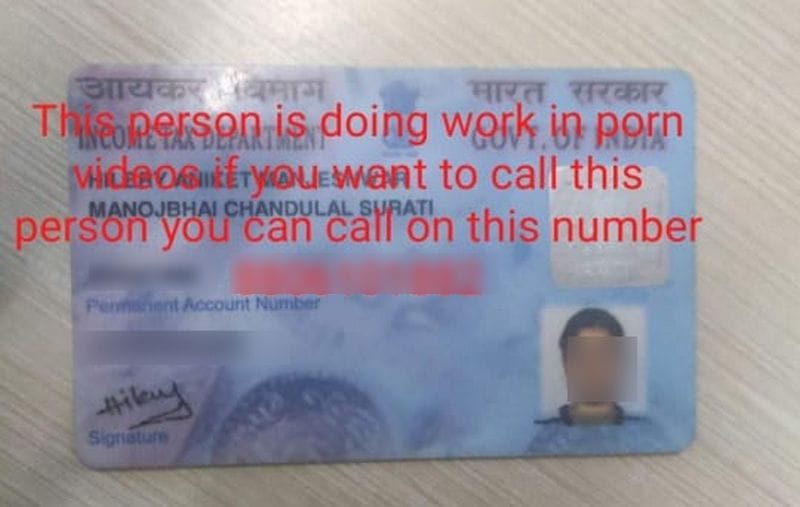

To extract payment from him, a loan company created a WhatsApp post featuring a photo of his face alongside the caption “Fraud Alert”. He told ThePrint that this post was circulated to all his phone contacts. “Be aware when you do a financial transaction with him or her,” the message says.

Stories like these are depressingly common. Journalist Shashank Shekhar, who runs a cybercrime news site called ‘The 420’, showed ThePrint some of the cries for help he has received from people who have been duped or harassed by companies peddling “online instant personal loans”.

“Few fraud loan people are forcing me to pay loan which I have not applied. They have paid me 2100 without my consent and now they are asking to pay 3500 (sic),” says one message.

“I am a loan fraud victim…Govt is not doing anything,” says another.

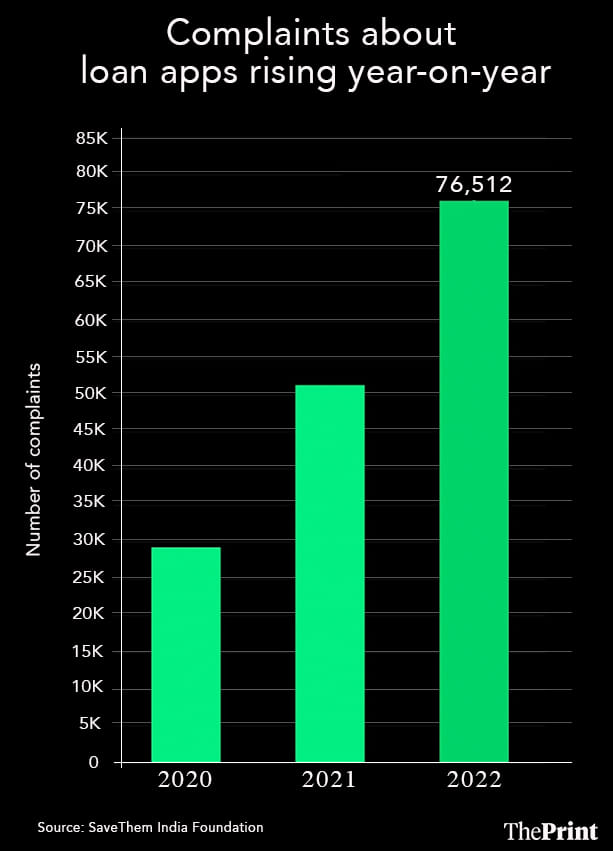

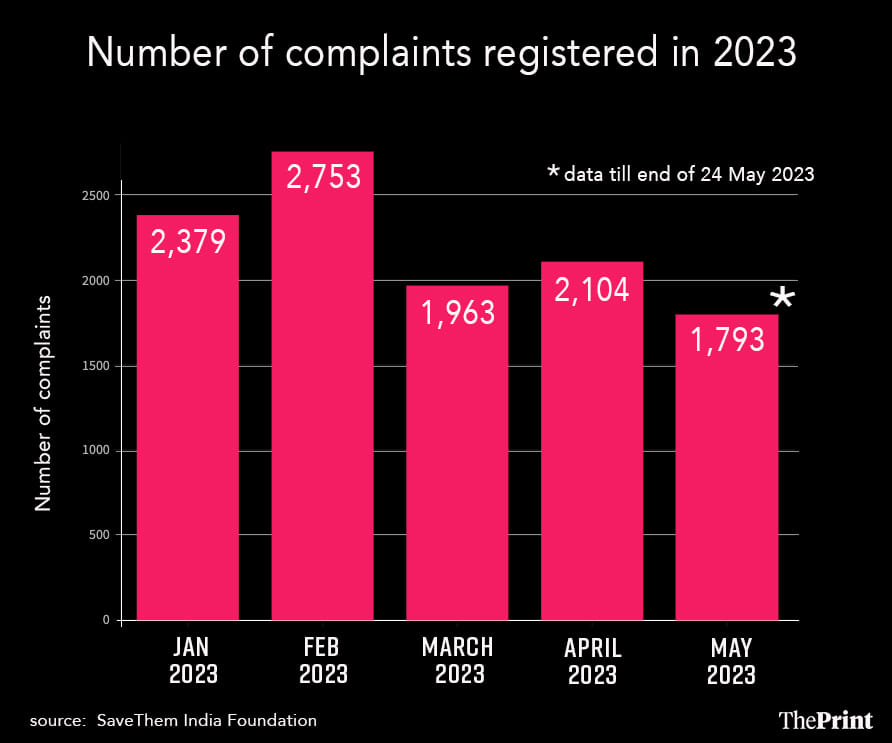

Loan apps reportedly started becoming popular during the 2020 Covid lockdown.

Statistics shared by SaveThem India Foundation, a non-profit dedicated to educating citizens about cybercrime, also show that complaints to them about digital lending have increased every year from 2020 onwards.

Last month, the NGO received a daily average of 70 complaints. For May so far, the average has been 75 complaints per day.

So far, the government has blocked dozens of loan apps, the Reserve Bank of India (RBI) has cancelled the registrations of several Non-Banking Financial Companies (NBFCs), and even Google Play has rolled out more stringent requirements for such apps.

These steps, however, are proving to be insufficient, and there is very little concrete action on the ground.

For instance, last year, Finance Minister Nirmala Sitharaman chaired a meeting to address the issue of illegal loan apps. During the meeting, government officials agreed to enhance cyber awareness among customers, bank employees, and law enforcement agencies. They also acknowledged that all ministries and agencies should take “all possible actions to prevent” illegal loan apps. It is unclear how much of this has been actioned in reality.

Then, this year, the finance minister cautioned against “financial influencers”, highlighting that seven out of 10 self-proclaimed finance experts may have hidden motives behind their advice and product endorsements. Still, the government currently has no plans to regulate financial influencers.

The problem is compounded by the lack of a defined ceiling for loan interest rates. The RBI microfinance loan master direction only says: “Interest rates and other charges/fees on microfinance loans should not be usurious.” However, it does not specify what qualifies as “usurious”.

“Things are not helped by the RBI not having a cap on interest rates. This allows the lender to decide the interest rate,” said Pravin Kalaiselvan, director of SaveThem India Foundation.

Ajaya Kumar Sahoo, a retired RBI official who is now chief operating officer at digital lending service FincFriends, said that the RBI de-regulated interest rates to keep pace with changing times.

“India is a developing economy in a global liberal market. In a liberal market, companies cannot compete if a regulator has fixed interest rates,” he explained.

When ThePrint spoke in depth to people who have borrowed from lending apps, it found that the ground reality is more complex than it may seem at first.

While some loan apps resort to dubious recovery methods and exorbitant interest rates, their customers tend to also be low on financial literacy, prioritising quick access to funds over caution. The result is a toxic lending space filled with distrust and default.

The following five stories all showcase this grim ground reality, and the several different forms it can take. One thing is clear. In a space with little regulation, it is each man and woman for themselves and often at their own peril.

Also read: Govt’s ban on loan apps: Data theft, tax evasion, extortion & fraud charges behind move

Too many loans to remember

On the face of it, Sumit Bhardwaj seems to be doing well for himself. He is president of Expert Driver Solution, a cab driver union affiliated with the Indian Federation of App-Based Transport Workers (IFAT), and runs a car brokerage in Badli.

Bhardwaj also seems to be drawn to loans, running his business on borrowed money more than anything else.

He doesn’t remember the details of each loan he has taken because there are too many. He only pays attention to them when the payment deadline approaches.

When ThePrint met him in February at his office, he mentioned one loan from Muthoot Finance and another of about Rs 20,000 from KreditBee. He also had a loan of around Rs 84,000 from Indiabulls, which he didn’t repay on time, so the due was over Rs 2 lakh in February. Additionally, he also owed loan payments to an app called PaySense.

“We need money urgently, so we take money from these kinds of apps,” he said about the PaySense loan. The interest rate is 30-40 per cent and he took the loan around December 2019 or January 2020, he estimated.

Bhardwaj was yet to pay off this loan when ThePrint visited him and recovery agents seemed to be getting impatient.

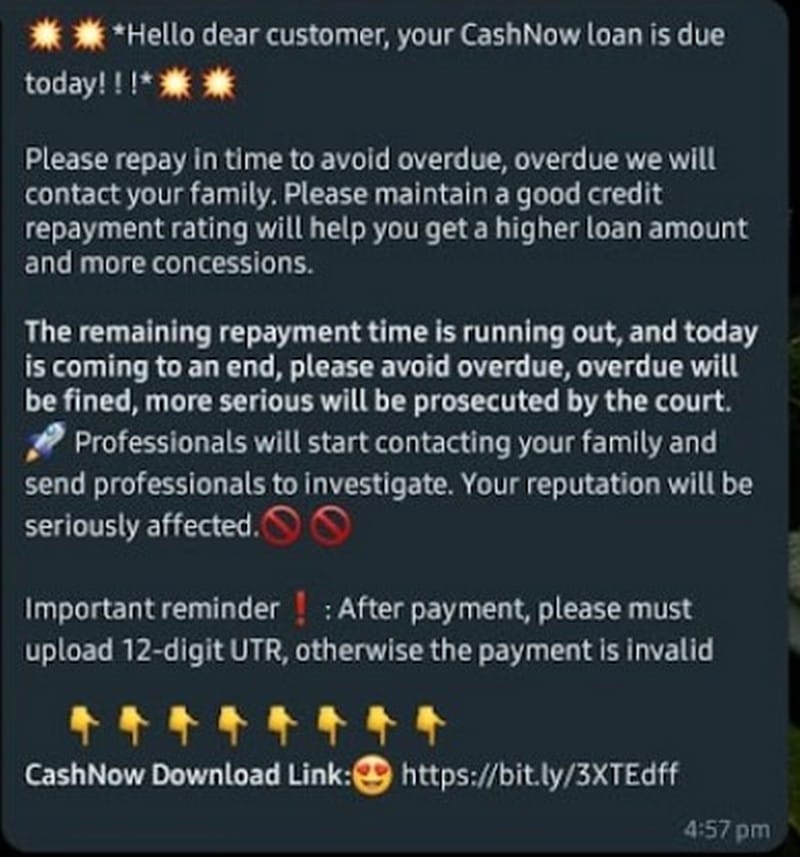

“We are unable to pay due to financial struggles after the Covid lockdown, but these lenders started to threaten us via recovery agents. They say if you don’t pay EMIs we will lodge FIRs, we will pick you up from home. They are calling everyone on my contact list asking for loan repayment, calling even my relatives. They torture us,” he said.

Even while ThePrint was speaking with him, calls kept pouring in, including those described at the beginning of this report.

The conversations were chaotic, often descending into screaming matches filled with confusion, with the loan collection agent repeatedly asking if he was Bhardwaj, and who would repay the loans.

Bhardwaj said all of these calls were from PaySense recovery agents.

When his customer called to complain about a recovery agent harassing her, Bhardwaj was not surprised. He said he suspected loan recovery agents somehow access his call records because they end up calling people who call his number.

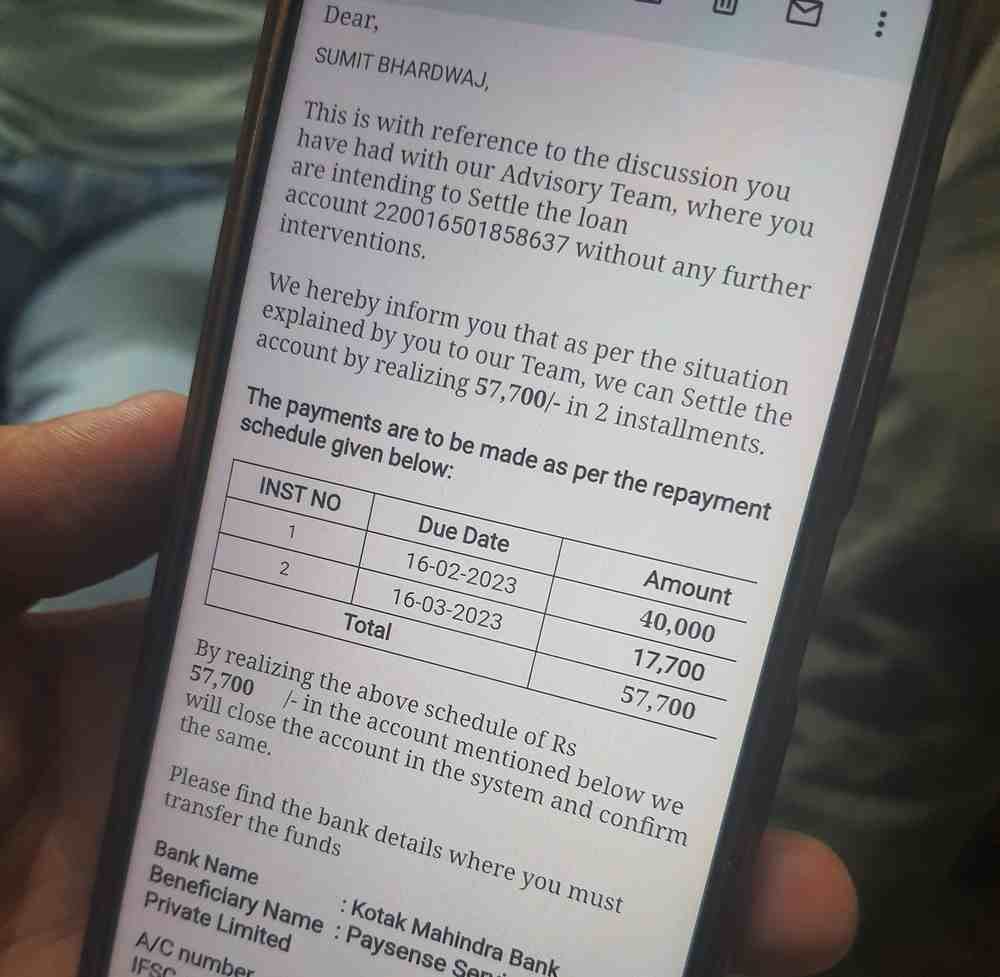

When ThePrint caught up with Bhardwaj again in April, he said he had settled the PaySense loan by shelling out Rs 57,700. He was unable to remember the original loan amount.

Asked for comment about the loan recovery practices at PaySense, a company spokesperson said that all collection efforts were in consonance with norms set by industry watchdog Banking Codes and Standards Board of India (BSCBI),

“Our recovery agents undergo rigorous training to comply with the regulatory directives and guidelines,” a statement by the company said.

The statement also addressed queries about agents allegedly accessing call logs.

“The PaySense App does not access the phone book of the customer, and this can be easily verified by downloading the app. We also do not have tie-ups with telecom providers to get the call logs of customers,” the statement said.

On the interest rate, the statement added: “Our annual percentage rate is clearly disclosed to the customers, in line with market practices and there are no hidden charges.”

‘Scam calls from Pakistan, Laos, and Bangladesh’

Hilery Manjeshwar, originally from Ahmedabad, has been in Pune for the past decade and works in marketing. She has had many run-ins with scams disguised as loan services.

She claimed it started in 2019 when the prevailing trend was “7-day loan apps”, which offered loans that could be repaid within a week. Most of these apps were shut down by the government in 2020 and 2021, Manjeshwar said.

“I didn’t know these apps were illegal or that their loan collection agents harass people. Somewhere in 2019, I took a Rs 3,000 loan because I had a money shortage. I can’t remember the name of the app. But there were hundreds of them with similar names,” she added.

The loan application was simple, Manjeshwar recalled. “You need to make an account, upload photos of PAN, Aadhaar, then provide basic info like your name. The scary part was that the app wanted permission to access my phone’s camera, photo gallery, and contacts,” she said.

However, she got a surprise when the loan amount was credited.

“They only put Rs 1,800 (out of the Rs 3,000) in my bank account. So, you can see how high interest rates were. Starting the sixth day after my taking the loan, they started calling asking to pay the full Rs 3000,” she said.

After this, a campaign of harassment started, she claimed.

“The app accessed the contacts on my phone and started calling family members also, abusing them, harassing, sending sexually morphed pictures of me to relatives,” she said.

In March this year, a new nightmare started, and this time she hadn’t even signed up, Manjeshwar claimed.

“Around end of March, I got a call from my cousin, asking me, ‘Hilery, I got a call in your name saying you have a loan of 15,000’. The caller was asking my cousin to pay it. But I had not taken any loan,” she said.

Manjeshwar suspects that her young son may have accidentally clicked on a spam link on her phone. “I too started getting WhatsApp messages to repay a loan even though I now have no lending apps on my phone,” she said.

“These WhatsApp messages came from numbers based in Pakistan, Laos, and Bangladesh. The WhatsApp voice notes were from a Laos number but were in Hindi so I know these are fake,” she added.

Manjeshwar e-mailed Pune City’s cyber police station about the issue and got this response: “plz contact your nearest police station”. ThePrint has seen this e-mail thread.

‘Driven by desperation to loan apps’

Harish Kumar, 38, is originally from Tirupati, but now divides his time between Bengaluru and Hyderabad.

He started an IT consultancy in 2017 but the business didn’t work so he was short on cash. He is the sole breadwinner for a family of three, including himself.

Speaking to ThePrint from Hyderabad, he said he “didn’t have the guts to go to the bank or relatives” when he needed money for family expenses.

Kumar couldn’t go to the bank because his CIBIL score, or credit history, was less than stellar.

“Month-on-month living expenses, along with a personal loan from a bank I had to repay, had surpassed my income,” Kumar said.

Desperate for options, Kumar turned to Google and searched for places where he could get loans despite his low CIBIL score.

During his search, he found links to YouTube videos on low CIBIL scores. In these videos were ads for loan apps. One ad was for an app called Swift Loan, then available from the Google Play Store, he said.

Kumar recalled that he first took a loan from the Swift Loan app “around a year or six months ago”.

“I started by taking a Rs 10,000 loan, but I kept taking more. The total loan is about Rs 1 lakh now,” he said.

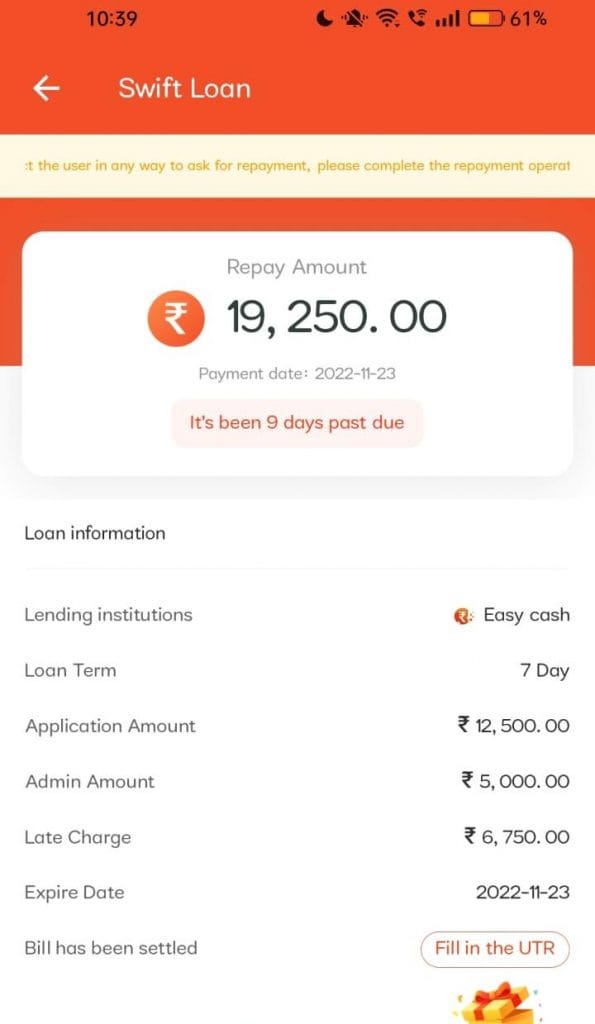

Kumar shared screenshots of his loan app profile, which showed that he took his first loan in September 2022. The Swift Loan app appears to be a platform where a user can access several loan providers.

According to Kumar, Swift Loan provides funds in tranches and charges hefty fees. Hidden costs were another issue, he said.

For example, in November 2022, he borrowed Rs 10,000 from a lending institution called BlinkLoan, via Swift Loan, with a repayment period of seven days. This loan came with a “late charge” of Rs 3,240. “Even before the seven days ended, they started charging me a late fee,” he said.

These types of extra charges have significantly hiked the dues payable by Kumar.

“The total loan amount disbursed to me was about Rs 1 lakh, but I have to repay around Rs 2 lakh due to processing fees and added charges like late fees,” he said.

Kumar claimed he has now paid off most of the loans obtained through the app and has stopped using it to avoid harassment from loan recovery agents.

“Once six days pass, agents from the app call and harass for repayment. Swift Loan app misused my contact list. They called my contacts to recover the loan and sent morphed vulgar pictures of me to relatives,” he alleged.

Kumar said he e-mailed the loan company and Telangana’s Cyberabad Police seeking help to stop the harassment, but allegedly received no response.

He insists that he downloaded Swift Loan from the Play Store, although it is difficult to verify as the app appears to be no longer available.

ThePrint tried to trace the app by using the e-mail address through which communications from Swift Loan were sent to Kumar. This search led to a website called ‘swiftloanol.com’, apparently operated from Mumbai. “We want everyone to have a better life and overcome the trials of life,” the ‘About Us’ section says.

However, there was no link to download the app when ThePrint accessed the site on 3 May.

“These apps change their names regularly so it’s hard to remember which app is which and it’s hard to trace them,” Kumar said.

‘Rs 20,000 loan rockets to Rs 1.4 lakh in dues’

Andhra Pradesh-based Peddireddy Samarasimhareddy, 25, has been working in the software industry for the past 4.5 years and earns an annual income of Rs 11.5 lakh.

In July 2021, he took a Rs 20,000 loan from an app named Creditt+. Samarasimhareddy claimed he came across it while searching for loan apps on Google Play Store.

“This was during the Covid lockdown. My salary was paid only partially so to cover expenses and to support my family of four, I took the loan. I am the sole breadwinner,” he explained.

According to Samarasimhareddy, he was ready to repay the loan in full after 34 days, but was unable to do so because his UPI was not working.

“The next day, I saw a penalty of Rs 5,000 had been imposed for the delay. I asked their customer support why there was a penalty and to reduce it. But daily, the company increased the penalty by Rs 200-300. Now they want me to pay Rs 140,000 in total,” he alleged.

Speaking to ThePrint in April, Samarasimhareddy said that Creditt+ had shared his Aadhaar details with his contact list in an attempt to retrieve the loan amount.

However, when ThePrint spoke again to Samarasimhareddy this May, he said that the company had stopped calling him about the loan, even though he is yet to repay it.

Notably, ThePrint also came across a LinkedIn post from a year ago by the co-founder of a company called Pixsonik complaining that Creditt+ was contacting them to recover the loan amount of “some random guy”.

ThePrint e-mailed Creditt+ seeking comment, but a response has not been received.

Perils of ignoring the fine print

Twitter user @ak46tweets reached out to ThePrint on the social media platform to express dissatisfaction with his experience of getting a loan via fintech platform Mobikwik, stating that the interest rate was too high and felt like a “scam”.

His Twitter profile indicates that he is a professor based in Chennai.

Later, he identified himself as Vinod Srinivasan but did not disclose his age.

When ThePrint spoke to him, he recounted two instances of taking loans, both of which he said have been fully repaid. He could not recall the exact dates but remembered the respective years.

In 2021, due to a Covid-related “medical emergency”, he required cash and obtained a loan of Rs 60,000 from “Fullerton or something” via Mobikwik.

There are two Fullerton companies on the platform — Fullerton India Housing Finance Limited and Fullerton India Credit Company Limited — but he could not remember which one he borrowed from.

“I thought I could pay it back in two months. It was my fault also — I went for the attractive interest rate. They said 2.5 per cent per month,” he said.

The fine print, though, painted a different picture.

“I didn’t read the entire terms and conditions, which said I had to pay the 2.5 per cent interest rate for a minimum of six months, whether I close the loan or not. That lock-in period was the dark hole I got caught in,” Srinivasan explained.

Then in 2022, he borrowed Rs 2 lakh from Tata Capital on behalf of one of his “best friends” who had a poor credit score.

He applied for the loan in his friend’s name, provided him with the money, and the friend made the monthly instalments (EMIs).

“Initially they told me the interest rate was 10.5 per cent per annum. After a few months they suddenly raised it to 14.5 per cent, citing RBI,” he said.

Srinivasan recalls that in May 2022 RBI increased the interest rate. This hike in the benchmark interest rate was by 40 basis points to 4.40 per cent. But Tata Capital’s hike was far higher than the RBI one, he pointed out.

The company, he said, had told him they had “no choice” but to raise the rates, and they also had a mandatory lock-in period of six months.

“This was a shock because I was hoping to close the loan within three months with an interest rate of 10.5 per cent. But the interest rate shot up, and we were both in trouble,” said Srinivasan, laughing sheepishly as he recalled the shock.

ThePrint contacted Tata Capital via email for comment about this interest rate increase, but no response was received.

“After that, I told my friend to not go for personal loans from private providers,” Srinivasan said. “It is better to get a loan from a bank.”

(Edited by Asavari Singh)

Also Read: China’s loan apps mafia spills over to India. Banning isn’t going to help