")

Bad news, pandemic-era investors: The Federal Reserve won’t have your back as it once did.

For newbie traders who signed up for Robinhood Markets Inc. or other online brokerages over the past 22 months, the playbook has remained constant: Buy any dips in large U.S. equity-market indexes and profit. This tried-and-true strategy persisted even amid a face-ripping rise and fall in meme stocks, cryptocurrencies and shares of unprofitable companies that relied largely on belief.

That hasn’t worked in the first three weeks of 2022. At first, a sharp increase in U.S. Treasury yields was to blame as bond traders quickly realized that not only was the Fed serious about raising its key lending rate multiple times this year but that it would also soon start to reduce the size of its $8.9 trillion balance sheet. Yet the benchmark 10-year yield fell about 12 basis points in three days last week, the sharpest drop since late November, and equities still tumbled, led by rate-sensitive tech shares. The S&P 500 Index is down almost 8% this year and closed below its 200-day moving average for the first time since June 2020, while the Nasdaq 100 has declined more than 11%.

That’s one clear hint that the stock market is coming to terms with the reality that the “Fed put” is disappearing in the rearview mirror. Even after this latest swoon, among the most severe since the central bank swooped in to support financial markets in March 2020, it’s highly doubtful that policy makers will be knocked off course at their meeting this week. Instead, they’ll look through the rout in equities to signal that they’ll raise the fed funds rate from near zero in March and probably begin balance-sheet runoff around mid-year, dialing back accommodation in the face of persistently elevated inflation.

There are a few key reasons why the Fed won’t falter because of this stock-market volatility. Here are four of them:

President Biden gave the green light to hike

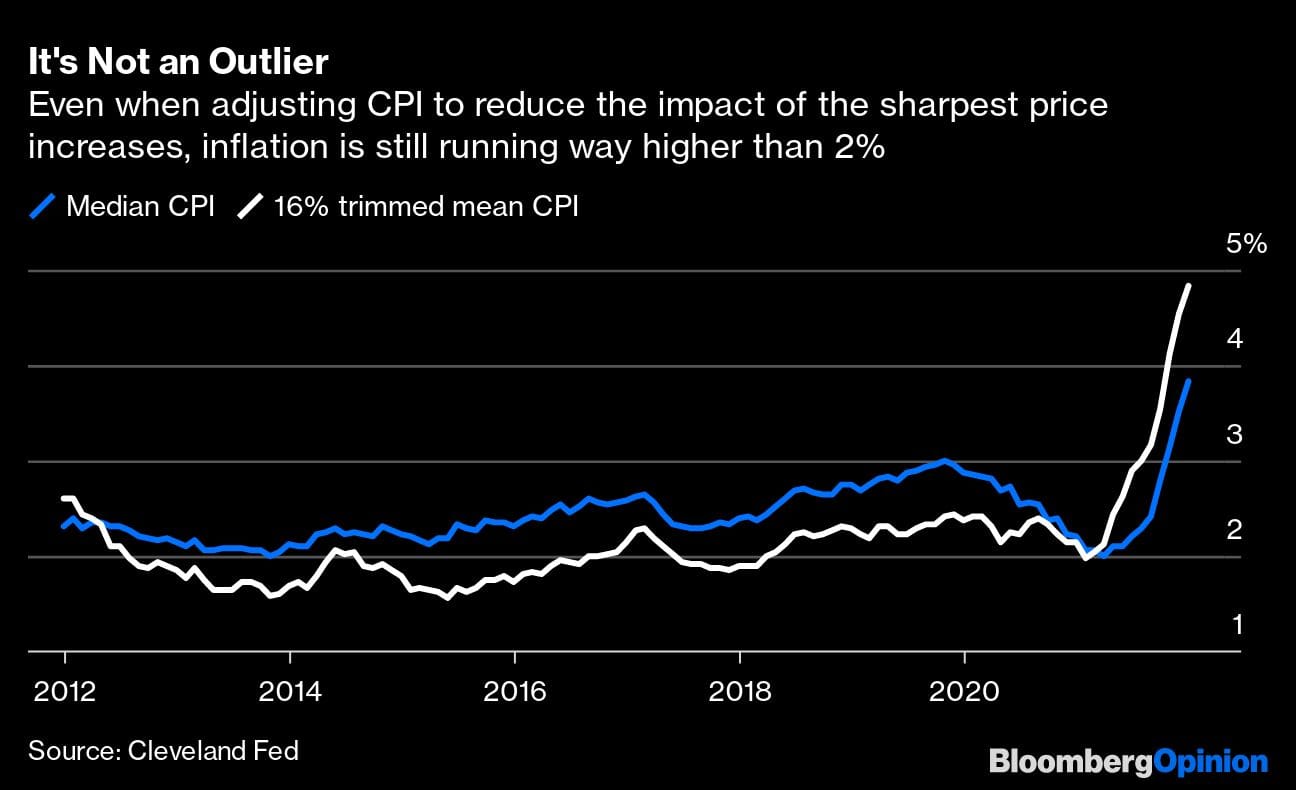

It’s no secret that inflation is top of mind for all leaders in Washington. When Fed Chair Jerome Powell and Governor Lael Brainard appeared before the Senate Banking Committee earlier this month for their confirmation hearings, they were grilled on how they would bring down consumer price growth, which far exceeds the central bank’s 2% target.

Powell, as he often does, tried to thread the needle, arguing that the central bank needs to quell inflation to get to maximum employment. But he sprinkled in hints that he’s still betting that supply constraints will ease so the Fed doesn’t have to raise interest rates quite as much to fix the economy’s supply-demand imbalances.

President Biden, whose approval ratings are sliding in a midterm election year, appears less inclined to count on hope as a strategy. In a press conference marking his first year in office, he attempted to put the onus squarely on the Fed to deal with annual price growth that by some measures reached 7% in December.

“The critical job in making sure that the elevated prices don’t become entrenched rests with the Federal Reserve,” Biden said at the White House. “Given the strength in the economy, and the pace of recent price increases, it’s appropriate,” as Powell indicated, “to recalibrate the support that is now necessary.”

Even before Powell’s testimony, I posited that Biden wouldn’t mind if the central bank found a way to gently lower price growth — and preferably by Nov. 8. He will never be as blatant in violating central bank independence as his predecessor, Donald Trump, who pounded the table for interest-rate cuts. But this is about as clear a green light as Biden will give that his administration is on board with Fed tightening.

Also read: Day traders jump into India stocks as they start to collapse

Increasingly hawkish calls provide cover for the Fed

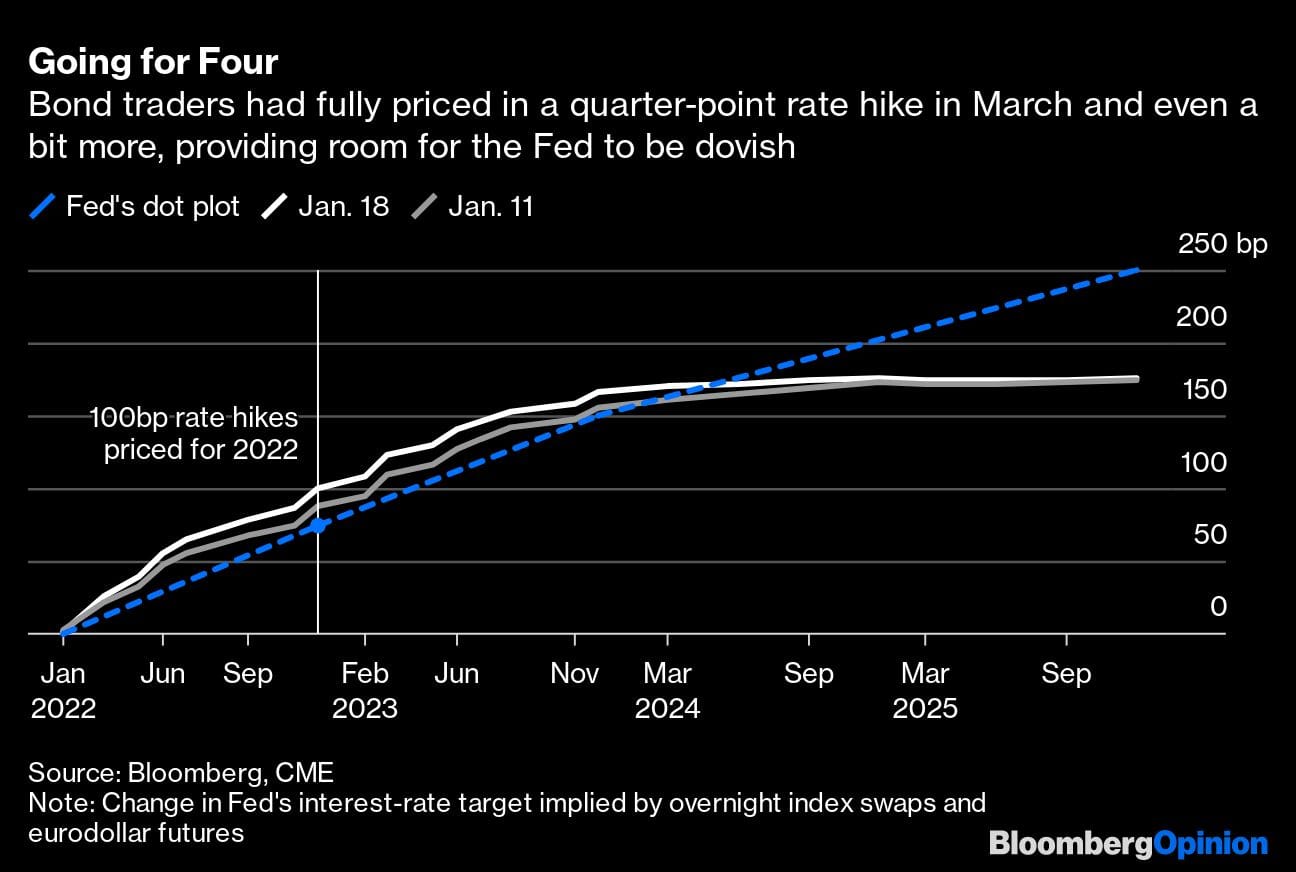

As of mid-December, the median forecast among Fed officials was for three quarter-point rate increases this year. At that point, the Fed had already seen the consumer price index rise toward 7% and the unemployment rate drop to near 4%. While the jobless rate has declined even more and year-over-year inflation has increased, neither have moved in such a way that would drastically alter the thinking within the central bank.

And yet bond traders used the sharp move higher in interest rates to push the envelope. At one point last week, 100 basis points of rate increases were priced in for 2022, with bets mounting that the central bank could lift the fed funds rate by 50 basis points in March. That kind of increase hasn’t happened since 2000 but was championed by billionaire investor Bill Ackman as a way for the Fed to “restore its credibility.” Days later, Bank of America Corp. strategists led by Michael Hartnett called policy makers “hysterically behind the curve” and argued they should boost rates by 50 basis points at this coming meeting.

A half-point rate increase this week absolutely won’t happen, and it almost certainly won’t in March, either.

If anything, these splashy hawkish calls are a boon to the Fed because they give Powell and his colleagues more room to be dovish by comparison. The policy statement this week might say something like raising the fed funds rate “may soon be warranted,” setting up a quarter-point move in March. That’s a far cry from the type of panic that Ackman and Hartnett suggest — and yet, just a month ago, only Fed Governor Christopher Waller was explicitly pointing to a likely March liftoff.

Whether sticking to the charted course will cause a stock-market bounce is far from certain, however.

Fed was anxious about market froth even before calls of “super bubble”

Jeremy Grantham made waves last week by calling out U.S. stocks for being in a “super bubble.” The co-founder of Boston asset manager GMO has often warned of market excesses, insisting “I feel it is just about nearly certain.”

Central bankers, for their part, would never use such terms. But the Fed did seemingly come as close as it could to saying “bubble” in its May 2021 financial stability report, and it reiterated in November that “asset prices remain vulnerable to significant declines should investor risk sentiment deteriorate.”

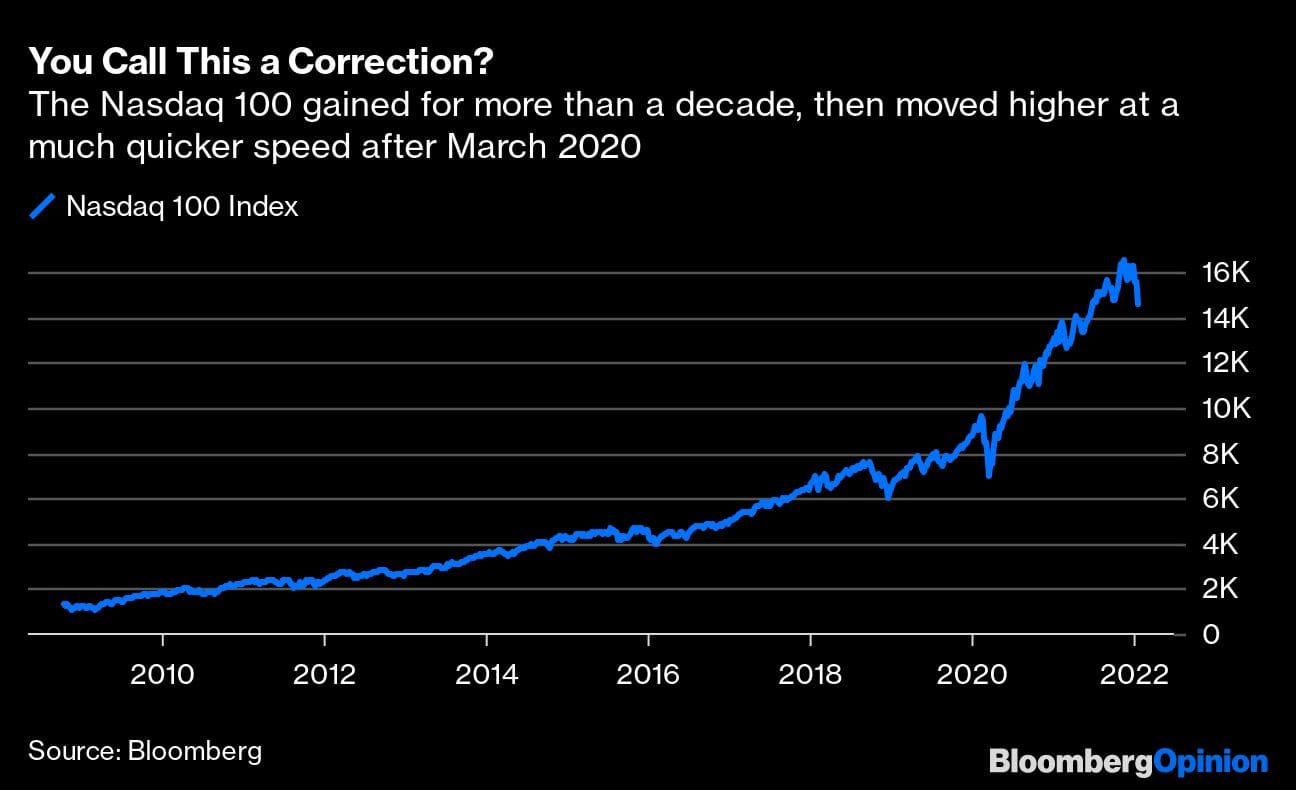

Whether this latest drop counts as “significant” depends on whom you ask. I tend to agree with my Bloomberg Opinion colleague John Authers, who scoffed at saying the Nasdaq 100 is in the midst of a “correction” just because it fell more than 10% from its peak. This latest turbulence came after a ferocious nearly nonstop rally.

The Nasdaq 100 has reliably gained over the past decade in large part because of subdued inflation — something that gravely concerned central bankers. Now they have price growth that is too high. They’ll use their blunt tool, interest rates, to attempt to find a new equilibrium. There’s no reason to expect a further rotation away from growth stocks and into shares of companies that benefit from a robust economy today will affect that calculus.

Also read: Lockdown sees more than a million new stock traders in India

Most important, credit markets are showing little sign of panic

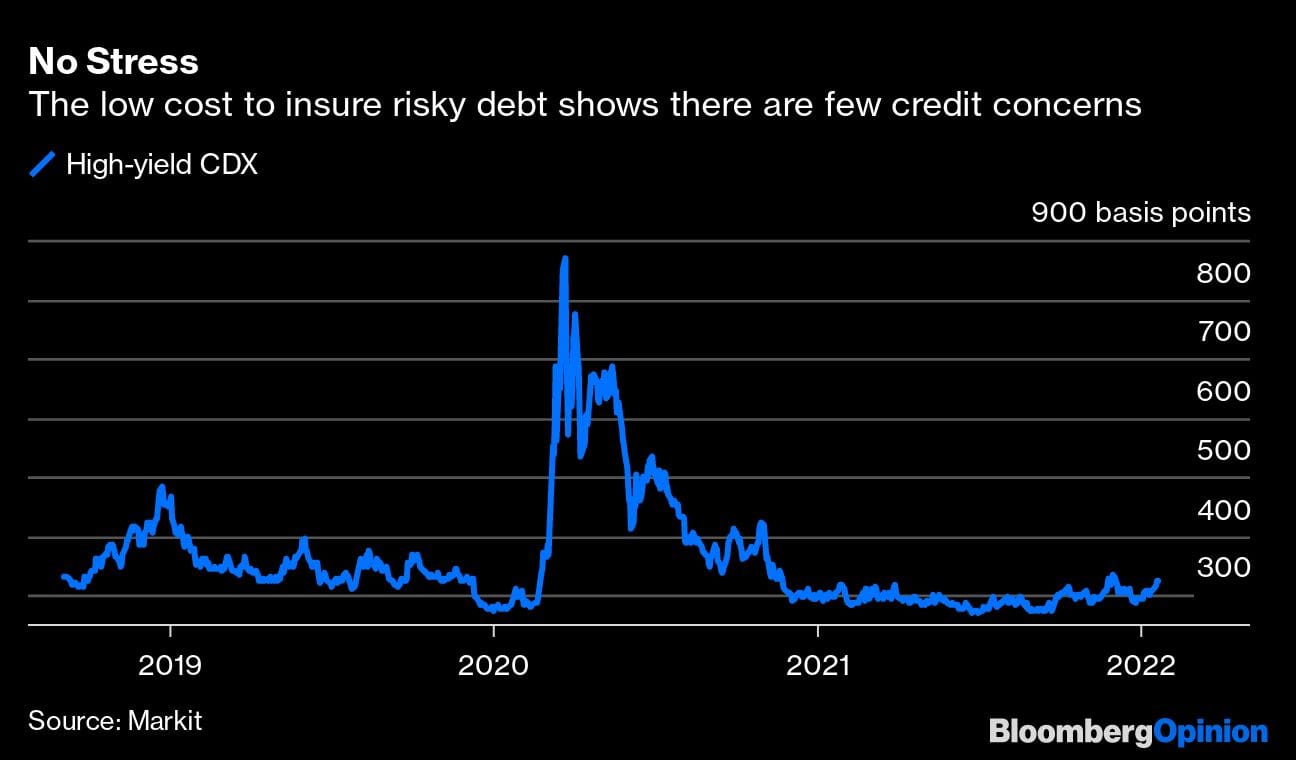

It’s popular to quip that the Fed is hypersensitive to declines in U.S. stocks. But it’s not quite correct. In reality, the central bank is acutely focused on making sure that credit-market conditions don’t deteriorate, which threatens both employment and financial stability. It’s why the central bank established corporate credit facilities at the onset of the pandemic.

Even as the share prices of Netflix Inc. and Peloton Interactive Inc. have plunged, there has been relatively little spillover to the broader corporate-bond market. Markit’s North America high-yield CDX index, which measures the premium demanded by investors to protect against debt defaults, stood at about 321 basis points at the end of last week. By comparison, it reached as high as 485 basis points at the end of 2018, around the time that Powell was forced to abruptly pivot from raising rates to eventually cutting them. On March 23, 2020, the day that the Fed unveiled its emergency credit facilities, the high-yield CDX index peaked at 871 basis points.

Meanwhile, at an all-in yield of 4.71%, the average junk-rated company can still borrow more cheaply than at any time before late 2020. They can also easily tap the leveraged-loan market, where funds are adding a record amount of cash given the appeal of their floating interest rates.

The credit market is quite possibly the most important indicator to watch for an indication that the Fed’s more hawkish rhetoric is adding strain to the financial system that would cause policy makers to back off. For now, Goldman Sachs Group Inc.’s financial conditions index remains more accommodative than any pre-pandemic period and is little changed from October. That’s a clear go-ahead for the central bank to proceed as planned.—Bloomberg

Also read: Analysts have never been this bullish about SBI in nearly two decades