")

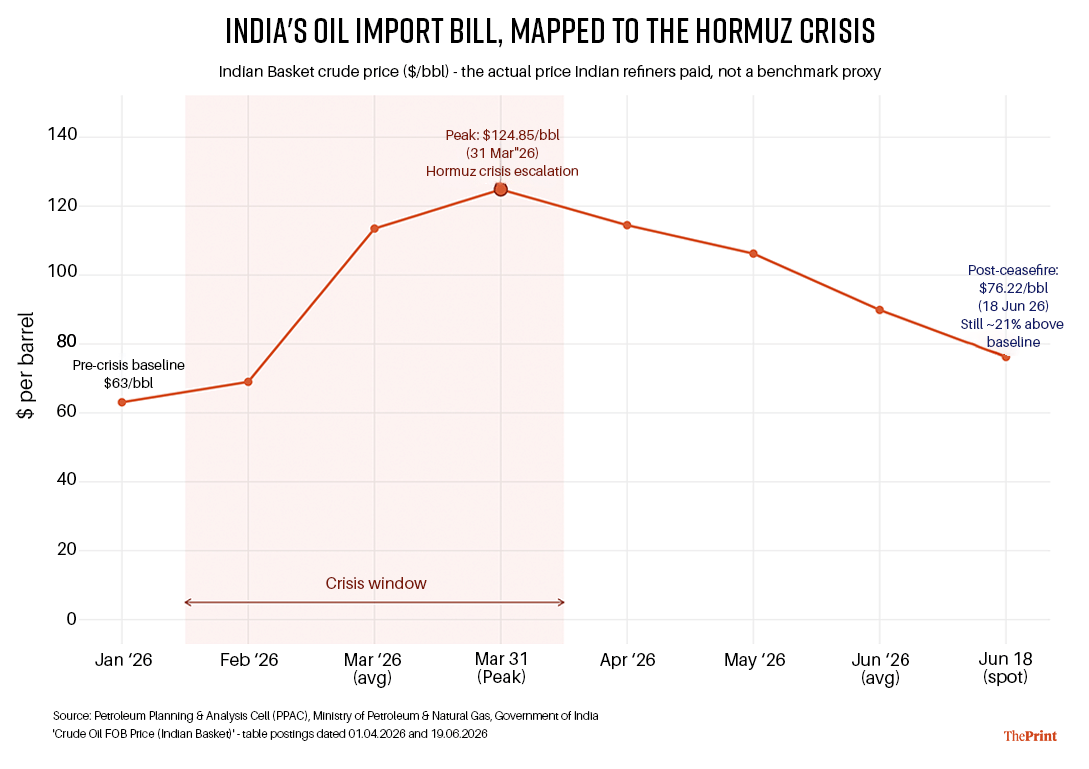

There is a specific figure Indian households are being encouraged to disregard right now: $124.85. This amount represented the cost of a barrel of oil on 31 March. The reason we’re not talking about it yet isn’t that we paid for it; rather, someone else paid for it on our behalf and hasn’t sent us the bill yet. Over a period of four months, Indian households observed stable petrol and cylinder prices, despite a conflict occurring two thousand kilometres away that disrupted nearly half of the country’s energy supply.

Currently, it is being cautiously communicated that the crisis has subsided. Crude oil prices have decreased. The Strait of Hormuz, we were told, had reopened. Exhale, except that even as I write this, Iran has declared the strait closed again, shipping traffic has stalled, and the United States insists it never closed at all. Nobody, including the ships currently sitting still in the Gulf, seems to agree on whether this crisis is actually over. The sense of relief that many felt, while understandable, may be somewhat premature. This is not due to the resurgence of danger, but rather because the economic implications of this crisis were not primarily about the war itself.

Instead, they pertain to fiscal illusion—something every economist recognises but is less visible to the general public. It is the reassuring notion that a cost not immediately apparent has not actually been incurred. It is simply an economic version of a credit card; the obligation remains even if the statement has not yet been issued.

The chart everyone saw, and the bill few did

Examine the actual price of the Indian crude basket, which reflects the cost incurred by our refiners, rather than a benchmark ticker number. In January, the price was a manageable $63 a barrel. By the end of March, at the peak of the Hormuz crisis, it had nearly doubled, reaching $124.85. That trend has been depicted in various forms in most of our publications this year.

However, what is less frequently noted is the current situation: even after the ceasefire and subsequent relief, the price remains approximately 20 per cent higher than at the beginning of the year. It represents a new, elevated floor that has been overlooked because the trend is now favourable.

The less visible aspect is more intriguing and significantly more challenging to discern.

The bill we haven’t looked at yet

When global crude oil prices increase significantly, governments encounter a critical decision: whether to immediately transfer the cost to consumers, or to mitigate the impact by absorbing the shock temporarily. India has opted to absorb the impact, relatively maintaining retail prices while state oil marketing companies bear a greater portion of the burden. This decision is not contentious; most governments, regardless of their political orientation, adopt this approach to deal with external shocks, as price stability is crucial for households during crises.

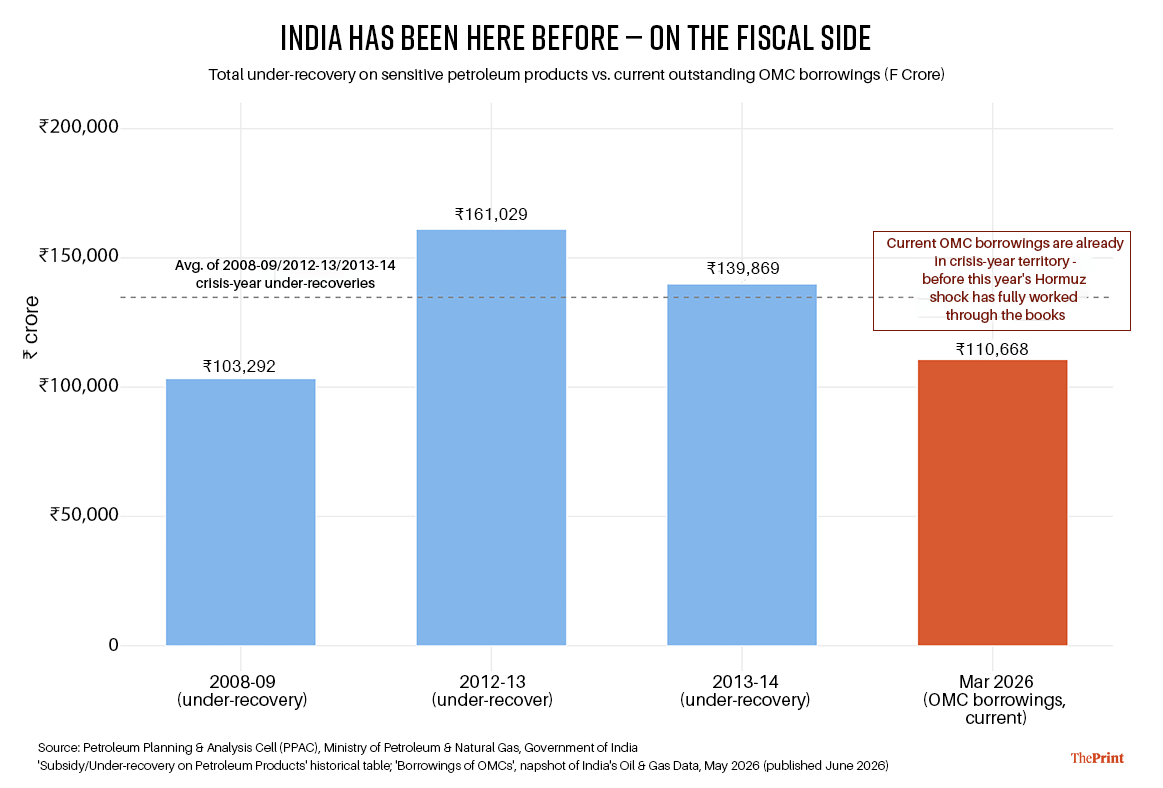

However, economics has a word for what tends to follow such a decision, and it isn’t relief; it’s deferral. India has previously lived through this mechanism twice. In 2008-2009, the total under-recovery on sensitive petroleum products amounted to Rs 103,292 crore, and in 2012-2013, it increased to Rs 161,029 crore. In both instances, the actual cost did not appear in the financial records of that year but emerged approximately 18 to 24 months later, typically as a recapitalisation of the oil companies that were initially asked to absorb the cost.

As of March 2026, the outstanding borrowings of oil marketing companies stand at Rs 110,668 crore, down from Rs 134,466 crore a year earlier, indicating some alleviation of the earlier financial strain. However, this figure remains comparable to the borrowing levels seen during the 2008-2009 crisis, and this is before the complete cost of the Hormuz disruption has been accounted for. The issue is not one of mismanagement but rather that the financial repercussions of this year’s crisis have not yet fully materialised. Given that India has encountered this pattern twice before, it should proactively plan for it rather than react to it later.

Additionally, there is a less conspicuous parallel that merits acknowledgement: although new gas exploration is progressing in the Andaman Basin and Assam, experts involved in these projects estimate that commercial production is still eight to 10 years away. Thus, while addressing future vulnerabilities at a decadal pace, the current year’s vulnerabilities are still being processed at the pace of an accounting cycle. In essence, we are borrowing time in the present in the hope that future supply will arrive in time to repay it.

Also read: How India’s maitrata doctrine benefits from the US-Iran truce

The way forward

None of this is a cause for alarm; rather, there is a need for enhanced transparency, which India is well-equipped to establish institutionally. Three measures could facilitate this process.

First, oil marketing companies should be required to publish a standing quarterly disclosure of their under-recoveries and borrowing levels. This would ensure that deferred costs are visible in real time, much like the RBI’s approach to more sensitive data.

Second, the Strategic Petroleum Reserve’s successful model, developed in partnership with the UAE for crude oil, should be expanded to include a substantial buffer of LPG and natural gas. These fuels were the most challenging to reroute during the recent crisis.

Third, the exploration initiatives in the Andaman and Assam regions should be treated as a long-term national project with clearly defined milestones and a dedicated financing plan, rather than being subsumed into the transient optimism of a single news cycle.

Wars end, but ledgers don’t settle themselves automatically. The Strait of Hormuz crisis will officially conclude when it is no longer a headline. However, deferred financial obligations will eventually need to be addressed. The critical decision for India is whether to confront this issue now, while there is still an opportunity to strategise, or to delay once more, mistaking the interim silence between the crisis and the invoice for a free pass.

Bidisha Bhattacharya is ThePrint Consulting Editor (Economics) and an Associate Fellow, Chintan Research Foundation. She tweets @Bidishabh. Views are personal.

(Edited by Ratan Priya)

We must reduce other imports.

Do crop diversification to reduce pulses/oilseeds.

Shift ethanol sugarcane production to Bihar and rice production to Bengal.

Build biogas plants to replace LPG.