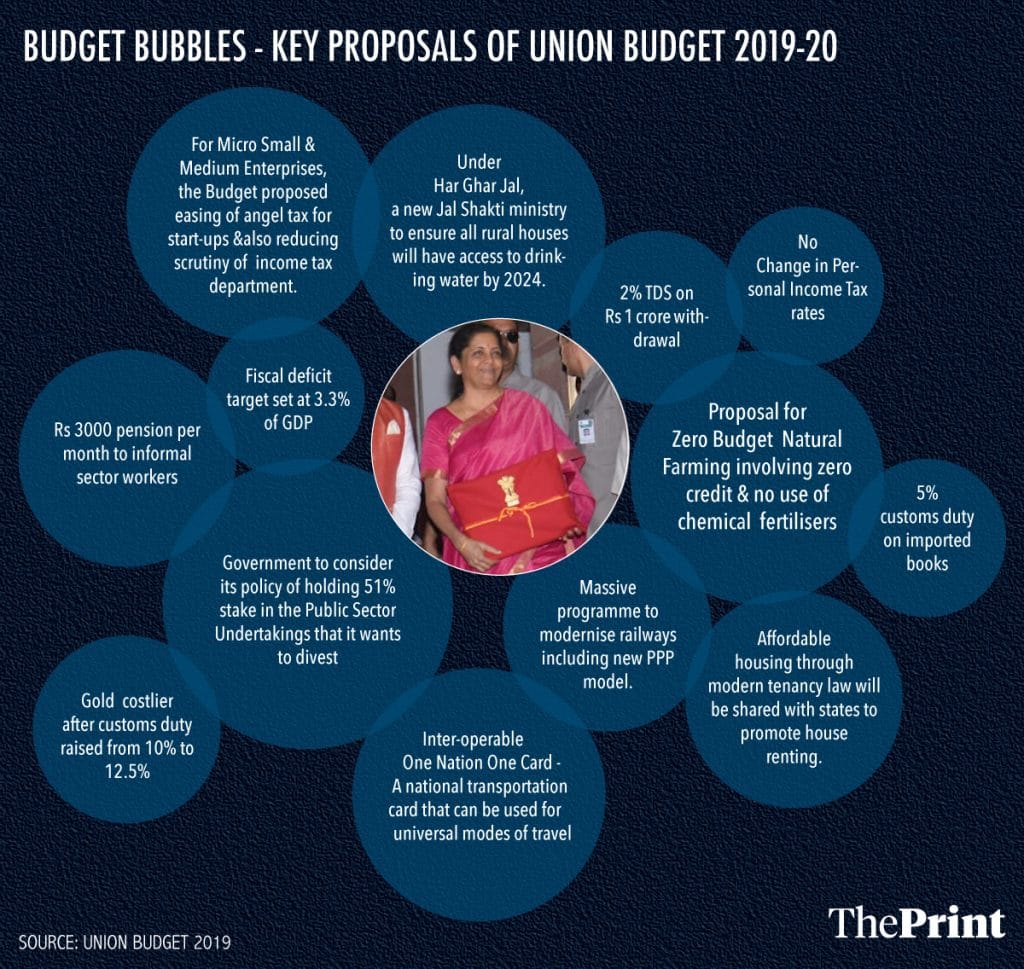

Budget 2019 began with a goal of making India a $5 trillion economy by 2024-25.

And to achieve that, the Budget provides a mixed bag of measures to boost financialisation of household savings. It talked about strengthening the financial markets, in general, and incentivising financialisation of household savings, in particular.

Four measures that affect households directly include:

- Continuation of the interim budget measure of no tax liability for those who earn up to Rs 5 lakh

- Possibility of retail investors in Central Public Sector Enterprise exchange-traded fund (CPSE ETF) getting equity-linked saving scheme-like(ELSS) benefits

- A new pension scheme, Pradhan Mantri Karam Yogi Maan-dhan, for retail traders and small shopkeepers

- Improving inter-operability between the Reserve Bank of India (RBI) and the Securities and Exchange Board of India (SEBI) depositories for retail investors in government bonds

Taken together, these steps provide a set of mixed incentives, heading in different directions.

Also read: Two pension schemes, one problem: What Modi govt didn’t learn

In India, tax-breaks have traditionally influenced the choice of saving instruments. Our research indicates that tax-incentivised households invest in products that offer a tax-break, especially insurance policies, and this impact is the highest for households in the income tax bracket of Rs 3.5 lakh to Rs 5 lakh.

By choosing to continue with no tax liability for those earning up to Rs 5 lakh, the government has reduced the incentive for this set of households to invest in Section 80C instruments. At the same time, an additional deduction of Rs 1.5 lakh on interest paid on home loans (valued up to Rs 45 lakh) will incentivise households to further invest in real estate. It is possible that saving in financial products, such as insurance, public provident fund (PPF), under the 80C bracket may get adversely affected, thereby eroding financialisation of household savings.

The Budget also announced that retail investors in CPSE ETFs could get ELSS-like income tax benefits. Investments made in ELSS mutual funds, which come with a lock-in period of three years, are eligible for tax deduction of up to Rs 1.5 lakh under Section 80C of the Income Tax Act. The extension of these benefits to the CPSE ETFs may help channel retail money to these funds.

The interim budget in February had announced a Pradhan Mantri Shram Yogi Maan-dhan (PMSYM) scheme for unorganised sector labourers. This budget has announced yet another pension scheme for retail traders and small shopkeepers. The details of the new scheme are awaited, but it is likely that both these schemes will work in parallel to the Atal Pension Yojana started by the previous government, also for the unorganised sector workers.

On the one hand, incentivising informal sector workers to save for their old age is a noble cause. On the other, creating separate schemes for different groups further fragments an already fragmented pensions market. The government should consider merging these schemes under the Atal Pension Yojana. The Pension Fund Regulatory and Development Authority (PFRDA) can regulate it to ensure better governance of informal sector pensions.

The proposal to make it easier for retail investors to access government bonds is an important one. The option to invest in government bonds has been around for a while, although it has not been very successful. This is probably because infrastructure for retail participation in government bonds has not been a part of the mainstream financial market infrastructure.

Also read: Why Nirmala Sitharaman renouncing budget briefcase for ‘bahi-khata’ is significant

By allowing inter-operability between the RBI depositories and the SEBI depositories, the experience may become relatively seamless for retail investors. If the government is able to actually facilitate this, it will be an important milestone in direct participation of households in government bonds, instead of through small saving schemes, the rates of which have been falling over time, or insurance plans, which have often provided very poor rates of return.

Once the implementation details are clear, we may get a better picture of the overall impact.

The author is an associate professor at the National Institute of Public Finance and Policy (NIPFP). Views are personal.