International capital flows have been a subject of interesting debate over the last week, especially in the context of net foreign FDI in India. Economist Surjit Bhalla and Chief Economic Advisor V Anantha Nageswaran have written thought-provoking pieces recently in The Indian Express on this subject. Bhalla argues, broadly, that the recent decline is a symptom of a deeper malaise in some of the policies rather than global headwinds. Nageswaran has suggested that gross FDI keeps growing strongly, while the softness in net flows reflects profit-taking by earlier investors and the compulsion of Indian firms to invest overseas—real, but not alarming and he bats for further reforms. Having spent years at the IMF studying the composition and quality of cross-border capital flows—including being integral to the IMF’s independent evaluation office’s report on capital flows—we find it imperative to share some insights on this debate. This article attempts to provide nuance to the discussion and also articulate the specific, low-cost reforms that could resolve the tension between gross attraction and net retention.

Let’s begin with what is unambiguously good. India drew $81 billion in gross FDI in FY25, a 13.7 per cent rise and among its highest hauls ever. This reflects a slew of economic reforms in the last year, making India a leading global destination for greenfield projects. More than 60 per cent went into manufacturing, financial services, energy and communications, the productive core of an economy. This reflects genuine structural attractiveness: A vast domestic market, a maturing digital backbone, and a manufacturing ambition the world takes seriously as a China-plus-one hedge. The capital inflow story is good, and India is, demonstrably, a country the world wishes to invest in.

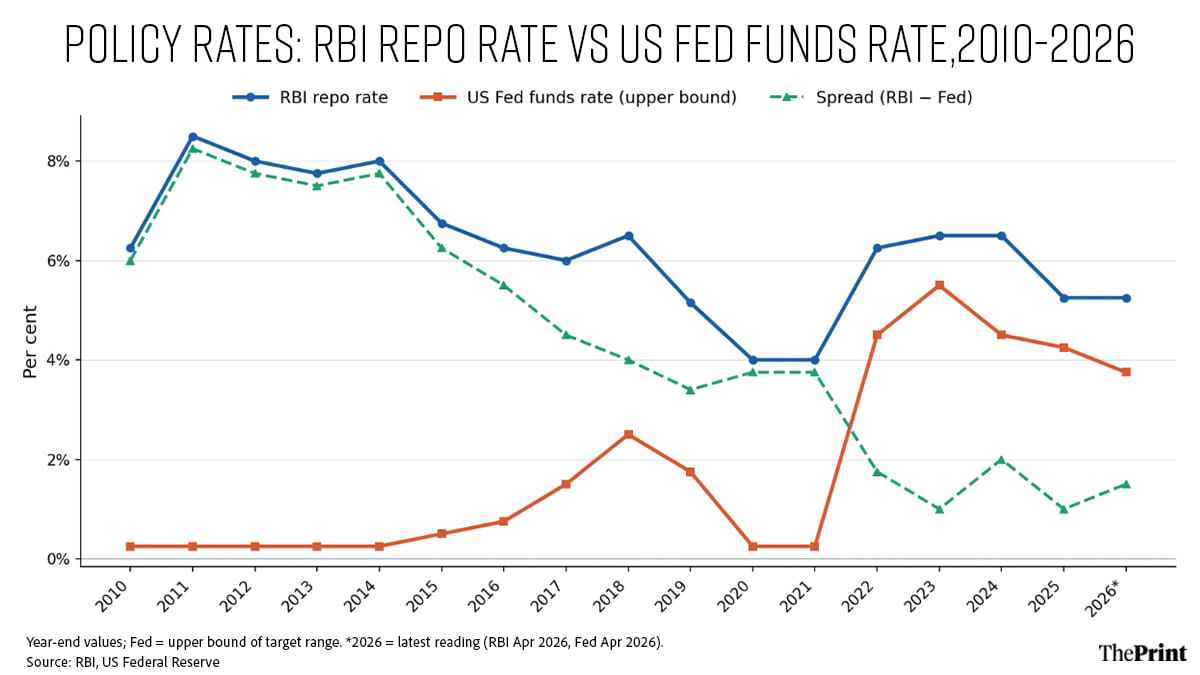

The harder question is whether India retains the capital it attracts. Comparisons to the 2013 taper tantrum are misleading. Back then, the RBI–US Federal Reserve rate spread (green line) was nearly four times what it is today, yet outflows were rampant the moment the Fed signalled hikes. This is because India’s macro fundamentals were far weaker, with high inflation and large fiscal deficits. Today, inflation is moderate, debt is benign, and the fiscal position is stable even after Covid-19. With the rate spread now much narrower (mirrored in the 10-year bond yields), some drift toward secure developed markets is natural—alongside other pulls like AI.

Repatriation by foreign investors rose to $51.5 billion, and outward investment by Indian firms rose to $29.2 billion. The RBI has called the repatriation surge the mark of a mature market, where investors can enter and exit smoothly. It’s precisely the quality that gives the next investor confidence. And India’s average return on inward FDI remains a robust 7.3 per cent, outperforming many peers.

Also read: India’s record net FDI plunge reveals a troubling trend—outward FDI beats investing at home

How India can step up

So what are the other factors that can help mitigate these outflows despite the international and structural factors mentioned above? Here, the international evidence is emphatic, pointing away from the usual fixations on tax or factor markets toward something India has under-prioritised: The speed and quality of its courts.

Drawing on the EU Justice Scoreboard, economists Panayotis Kapopoulos and Anastasios Rizos find that judicial inefficiency—by weakening contract enforcement and property rights—measurably depresses growth and investment.

For India specifically, economist Matthieu Chemin shows that slow courts substantially reduce output and employment growth in formal manufacturing, precisely the contract-intensive sectors that attract FDI.

Investors lacking certainty of enforcement price in “India execution risk,” demanding higher returns or shelving projects. This is precisely where India underperforms its potential. It carries one of the world’s largest judicial backlogs, with some 5.8 million cases pending in the high courts alone.

The gap between gross inflows and net retention is, in large part, an operational business execution problem driven largely by judicial uncertainty.

The encouraging corollary is that this is the highest-return, lowest-cost lever available. And we already have the foundation for it.

The Insolvency and Bankruptcy Code gave creditors a credible exit; the Commercial Courts Act of 2015 created a dedicated track. The finishing work is specific.

First, create properly resourced commercial divisions with strict case-management timelines and curbs on the adjournments that paralyse Indian litigation. This could be done by fast-tracking commercial and investment courts, especially for large multinational businesses that seek swift resolution in India. This could be kept in specific jurisdictions such as Gujarat’s GIFT city or other cities of convenience.

Second, a genuinely enforceable arbitration regime in which courts honour awards swiftly rather than reopening them, the precise failing exposed in White Industries v. India.

Third, after losing several arbitral claims, India terminated some 77 bilateral investment treaties from 2016 and adopted a restrictive Model BIT, whose requirement that investors exhaust local remedies for five years before international arbitration routes them back into the very courts they fear. Others argue that the evidence on BITs is mixed. The government, to its credit, confirmed in February 2026 that a revised, more investor-friendly Model BIT is underway; making that clause realistic is the linchpin.

Fourth, regulatory stability covenants for large, long-gestation projects need to be prioritised through single window clearance, not just for approvals but also for other matters, including implementation issues and easier exit possibilities for companies. In essence, an end-to-end window for large multinational projects that drive FDI into the country.

Singapore launched its International Commercial Court in January 2015, a specialist bench drawing international judges; the UAE’s DIFC Courts, operational from 2006, did the same for the Gulf. These countries felt the legal architecture of investment was worth building with intent. Unlike land or labour reform, predictable courts demand almost no exchequer outlay, yet could retain tens of billions annually. Confidence, the institutional literature consistently finds, compounds.

The reforms outlined here are possible, especially for a country with strong macrofundamentals and proven discipline in financial governance. We must build the legal infrastructure that makes capital feel permanent rather than provisional. It’s how the gap between what India attracts and what it retains will begin to close. India’s legal reform cycle for businesses could catalyse its FDI/capital flows, thus converting a retention problem into a compounding advantage.

Sriram Balasubramanian is an economist and best-selling author. He tweets @Sriramb1000. Prakash Loungani is director, Johns Hopkins Applied Economics Program. He tweets @LounganiPrakash. Views are personal.

(Edited by Theres Sudeep)