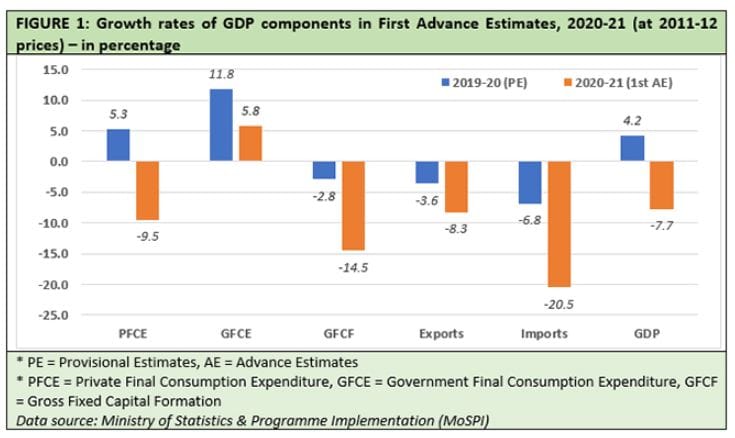

First Advance Estimates project the value of real GDP (gross domestic product) at constant prices (base: 2011-12) for the year 2020-21 at Rs. 134.40 lakh crore – compared to Provisional Estimate of 2019-20 GDP at Rs. 145.66 lakh crore. So, the real GDP growth rate is projected to be -7.7%, as against 4.2% real GDP growth in 2019-20.

Starting the first quarter of the fiscal year 2020-21 with a 23.9% contraction, this latest optimism about a muted effect of pandemic on the economy is prompted by an apparent “good recovery” in the second quarter.

However, among the major components of GDP only government final consumption expenditure (GFCE) is expected to have a positive growth rate. All other components are expected to be in the negative zone. While private consumption and investment continue to be projected as major dampeners, a -20.5% growth in imports is a matter of concern. For an import-dependent country for capital goods (heavy machinery and industrial inputs) like India this is not an encouraging trend (Figure 1). Government consumption has already reached its limits and will not be able to prop the economy up any longer.

Also read: V-shaped recovery is on, but by 2022, India will grow only 2.4% over 2019-20 — Economic Survey

The estimates are obtained by extrapolation of a set of indicators like first seven months’ IIP and financial performance of listed companies till September 2020. Therefore, the advance estimates come with a cautionary caveat that these are “likely to undergo sharp revisions”. So, any excessive future optimism should ideally take this into consideration.

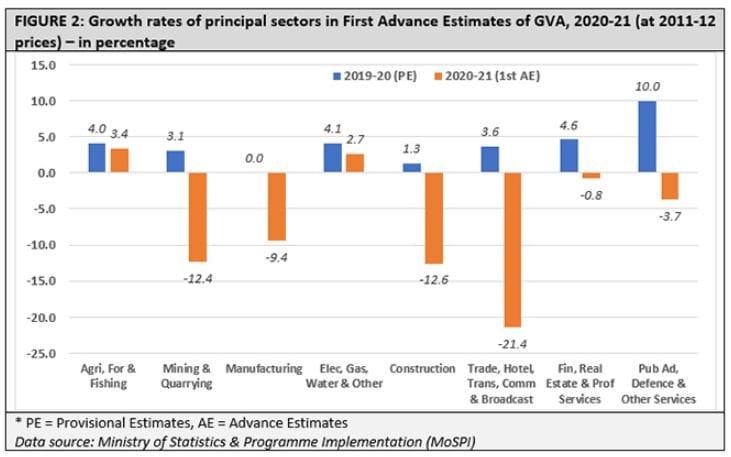

Agriculture, forestry and fishing is one of the principal sectors of the economy likely to have a positive growth rate of 3.4% in 2020-21. Other two are electricity, gas, water and other utility services, and public administration, defence and other services. In a very optimist projection, manufacturing has been estimated to grow at 0.03% in 2020-21. Rest are expected to clock negative growth rates in this fiscal year (Figure 2).

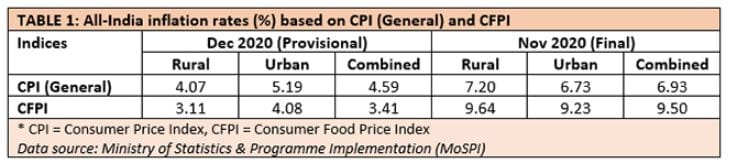

Another relief came in the form of softening inflation in consumer prices indices (CPI) in December 2020. The month of November has experienced upward pressure on both CPI and CFPI (consumer food price index). Domestic fuel prices continue to rise and contribute to the inflation. However, the festive season activities are likely to be a factor behind November inflation figures. So, the easing up in December is good for the economy (Table 1). However, the price movement needs to be closely watched as any flaring up would result in an eventual upward pressure on interest rates.

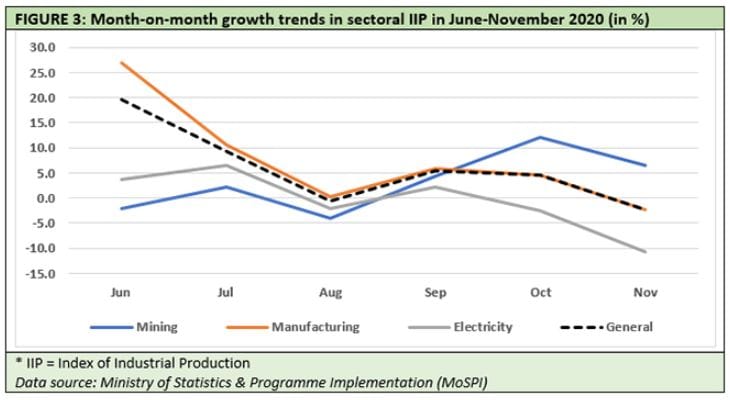

If all these results are combined, then definitely optimism about immediate future economic outlook looks logical. However, November IIP (Index of Industrial Production) data sufficiently clouds that optimism.

Also read: Economic Survey lauds India’s Covid approach, notes Kerala, Telangana, AP saved most lives

The pandemic induced restrictions were lifted in June 2020. If month-on-month growth rates in IIP figures are calculated since June, then the trendlines have fallen till August, then somewhat went up in next two months, but have fallen again in November – when the festive season was over (Figure 3).

Since August, production in mining sector clearly picked up. Electricity has gone down since September – part of the reason may be seasonal as winter set in while substantial section of workforce keeps on working from home. However, the trendlines of both manufacturing and general IIP are moving in tandem, signifying the importance of manufacturing in industrial production. And both have dipped in November. Here it may be interesting to remember that the First Advanced Estimates have projected a 0.03% growth in manufacturing in fiscal year 2020-21 (Figure 2).

Last four months’ performance of industrial production in this fiscal year will be crucial for the GDP optimism to actually materialise.

In its January 2021 World Economic Outlook, IMF (International Monetary Fund) projected a 11.5% growth for Indian economy, and many rejoiced. However, it is not yet conclusive that the economy has revived itself. Contradictory results in different set of official data signifies that. What seems to be a recovery may be, after all, a flash in the pan.

Abhijit is Senior Fellow with ORF’s Economy and Growth Programme. His main areas of research include macroeconomics and public policy, with core research areas in monetary economics and the political economy of finance. Views are personal.

The article first appeared in the Observer Research Foundation website.