Following a credit expansion and contraction that took place over the better part of the past two decades, Indian banks have been left with a number of delinquent loans on their balance sheets. Rather than selling or writing them off, however, some banks have continued to extend credit, keeping borrowers ‘alive’ on paper even as their economic productivity waned. These firms – now popularly known as “zombies” – have become a source of concern. Zombies tie up productive workers and capital, discouraging new investment by healthy firms (Caballero et al. 2008).

Our research aims to identify zombies in the Indian corporate sector and to understand which policy tools are effective in eradicating these firms (Kulkarni et al. 2019).

While it has traditionally been difficult to distinguish between zombies, distressed firms, and firms receiving subsidised loans, we introduce a new way of identifying zombies using quarterly supervisory data from the RBI’s (Reserve Bank of India) Central Repository of Information on Large Credits (CRILC).

We define zombies as firms that experience positive credit growth despite being 60-90 days past due on a loan in the previous quarter. We also restrict our definition to firms with credit ratings below AA, and firms that did not establish any new banking relationship over an eight-quarter period.

Based on these criteria, we find that zombies account for 11% of the borrowers in our sample, on average. A third of these zombies did not generate enough cash flow to cover their annual interest payments even during the period before our analysis. Note that the firms we identify as zombies are not only significantly past due, but their loan balances are increasing. We also find that, even as late as 2016, the majority of zombies were not reported as non-performing assets (NPAs) even though this designation technically applies to all firms that are 90 days past due. It is important for banks to recognise zombies as NPAs because they must then make additional capital provisions to protect against possible write-offs of these loans. However, due to lax enforcement, prior to 2018, banks were able to maintain that borrowers were perpetually 60-90 days past due, sometimes for years.

Also read: Record stimulus to fight Covid crisis is slowing credit downgrades of Indian companies

Solving the problem

The zombie problem is neither new nor specific to India. It drew attention after Japan’s ‘lost decade’, as economists wondered what factors held back Japan’s growth. Still, although the zombie problem has been documented in Japan and around the world, we know little about how to solve it. India underwent two policy interventions, spaced two years apart, which provide us with a valuable window into potential solutions. The first was a major overhaul of its bankruptcy system, known as the Insolvency and Bankruptcy Code (IBC) of 2016. The second was a regulatory intervention in 2018, put in place by the RBI, which forced banks to recognise and initiate the curing of defaults as soon as they took place. This regulatory intervention is popularly known as the ‘February 12th circular’. Our analysis ends in the first quarter of 2019, just before the Supreme Court quashed the February 12th circular on the grounds that the RBI had exceeded its authority.

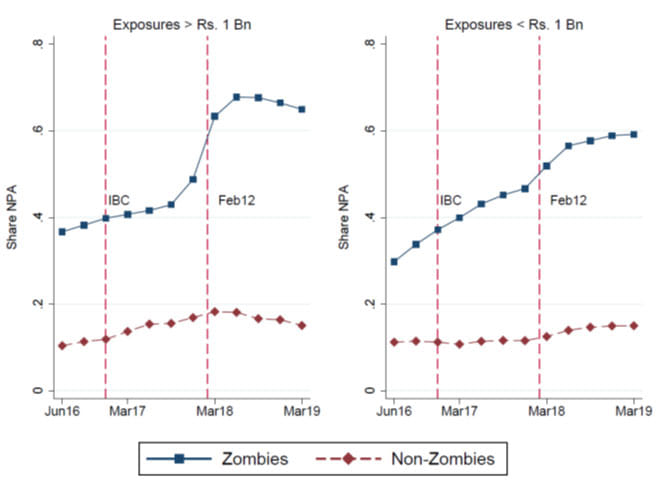

If the primary disincentive for banks to report NPAs is the low expected recovery on these loans stemming from an ineffective bankruptcy system, we would expect the passage of the IBC to lead to an uptick in zombie disclosures. Otherwise, we would expect the RBI intervention to have a stronger effect. Our results show that both policy actions mitigated the zombie problem, but the February 12th circular had an effect that was about four times larger. For robustness, we exploit a loan exposure cut-off of Rs. 1 billion, below which the February 12th circular implied weaker guidelines. We show that the regulatory intervention had a significantly stronger effect for borrowers above that cut-off. The effect of the IBC was no different for larger versus smaller borrowers, consistent with the absence of a size threshold under the new bankruptcy regime. Figure 1 below shows the proportion of borrowers reported by banks as NPAs, split by exposure.

Figure 1. Proportion of borrowers reported by banks as NPAs, split by exposure

The strengthening of India’s insolvency system led to a small improvement in zombie reporting. However, given that a stronger response came 15 months later with the February 12th circular, a lack of faith in bankruptcy institutions could not have been the only explanation for obscuring zombies. To further explore the mechanism, we study the differential impact of both interventions across banks with varying levels of capital, and for public- versus private-sector banks. Weak banks close to their regulatory capital thresholds are more likely to delay NPA disclosure in order to avoid costly provisioning for those loans (Acharya et al. 2019). If government ownership is a proxy for political interference, then public-sector banks (PSBs) may also neglect to disclose zombies, either due to regulatory forbearance or explicit directives to protect politically important borrowers. If these hypotheses are true, we would expect the February 12th circular to have a stronger effect on weakly capitalised banks and PSBs.

Surprisingly, we find the opposite. Banks with stronger regulatory capital buffers were more likely to report zombie borrowers as NPAs after the February 12th circular. While PSBs significantly increased disclosures, the magnitude of the increase was only half that of the increase in disclosures by private-sector banks. We take these results to mean that neither the passage of the IBC nor the February 12th circular was completely effective in eliminating incentives to sustain zombies. In the first quarter of 2016 when our analysis begins, weakly capitalised banks and PSBs experienced higher exposure to zombies. The muted response among these banks therefore implies that some zombies are still lurking, or that we have not yet reached 100% reporting of zombies as NPAs. Indeed, we find that the highest percentage of zombies reported as NPAs in our sample horizon is approximately 70%.

Also read: The new risk in India Inc’s boardrooms is a five-letter word called China

Reallocation to healthier businesses

Even if the interventions did not completely eradicate zombies, they still had a significant effect. A natural follow-on question arises: what happens once zombies are disclosed and provisioned for? First, we find that credit is reallocated to relatively large, investment-grade borrowers. This suggests that there was unmet demand for credit by these firms prior to the interventions. Second, using annual financial data from CMIE (Centre for Monitoring Indian Economy) Prowess database, we find that non-zombie firms significantly increase capital expenditures relative to zombies. This was true after the passage of the IBC, and even more so after the February 12th circular. Increases in investment were strongest among investment-grade firms.

If there has ever been a time to be vigilant about zombies, it is now. Governments worldwide are taking unprecedented steps to minimise the number of inefficient business liquidations that will result from the Covid-19 crisis. India has suspended IBC proceedings for up to one year. We support measures that limit the fallout of the pandemic in the short run.

However, as the Indian economy recovers, we should be wary of zombie firms that are using the pandemic as an excuse to continue hanging on. As interventions in the past have shown, not even a complete overhaul of the insolvency regime and a strict policy on NPA disclosure were enough to unearth all zombie firms. In order to prevent further drag on economic growth, regulators should do everything they can to keep zombies from becoming further entrenched.

Nirupama Kulkarni is an applied economist and Research Director at the Centre for Advanced Financial Research and Learning (CAFRAL), which is promoted by the Reserve Bank of India (RBI).

S.K. Ritadhi is an Assistant Professor of economics at Ashoka University.

Siddharth Vij is an Assistant Professor of finance in the Terry College of Business at the University of Georgia.

Katherine Waldock is an Assistant Professor of finance at the McDonough School of Business, and holds a courtesy joint appointment with the Georgetown Law Center.

All opinions expressed reflect those of the authors and not of the RBI or CAFRAL. The analysis was conducted while S.K. Ritadhi was a Research Officer at the RBI.

This article was first published by Ideas for India (I4I).