")

Contrary to popular narrative, the world is not deglobalising. Services trade as a share of global GDP reached an all-time high in 2025, improving upon its previous record of 15.2 per cent of global GDP in 2024. Goods trade volumes continued to grow—and also grew as a share of global output in 2025—despite being buffeted by US tariffs and elevated economic uncertainty.

Yes, it has become harder to trade in a more fragmented world. But despite the noise and uncertainty, the world benefits from trade, which is why traders continue to keep the shipping lanes humming and supply chains continue to adapt.

And the agile nations continue to grow. According to the latest WTO figures, Vietnam’s goods exports grew by an astonishing 17 per cent in 2025, reaching $473 billion. For the first time (barring a Covid-19 disruption year), Vietnam—a country of 100 million people—exported more goods than India, whose exports, at $445 billion in 2025, grew by less than 1 per cent.

This statistic alone tells us that India could and should be exporting much more.

Our new paper, just published by the Centre for Social and Economic Progress, shows precisely this. By “Letting the Elephant Dance,” India can unleash $516 billion of additional goods exports. If realised, this would more than double current goods exports.

Is this feasible in today’s world? It is both feasible and necessary. India’s share in world goods exports was only 1.8 per cent in 2024. China’s share was 14.6 per cent. So there is room to grow, with the “China plus one” diversification space providing a significant opportunity.

It is also necessary because India’s biggest development challenge remains the creation of more and better-quality jobs. The labour-intensive manufacturing sector can provide millions of formal, wage-paying, export-linked jobs in apparel, footwear, toys, furniture, food processing and light engineering. In fact, we estimate that the missing exports could support about 24 million new jobs, direct and indirect. These missing jobs are equivalent to about 68 per cent of 2020 export-related employment.

Our analysis identifies three major constraints holding back India’s goods exports: Protection, an elevated exchange rate, and weak integration into global value chains.

Also read: The double whammy India faces—External crisis & fiscal strain

Mapping the constraints

The first concern is protection, a deep-seated issue in India. Average tariffs have been creeping up over the last decade, and, as of 2024, were as high as 16.2 per cent. Although India’s average tariffs declined somewhat after 2022, they are still higher than they were in 2010, and remain significantly higher than those of major competitors like China (average 2024 tariff 7.5 per cent), and Vietnam (9.5 per cent).

In addition to tariffs, there has been a surge in Quality Control Orders (QCOs) since 2019. While QCOs are meant to safeguard public health and safety, in practice they have tended to act as non-tariff barriers to imports. Between 2019 and 2024, the number of QCOs rose from 88 to 765, with about half of them applying to key intermediates and capital goods. As of end 2023, 8.6 per cent of product lines were covered under QCOs.

Protection not only raises consumer prices, it also acts as a tax on exports. Consistent with this, India’s goods exports to GDP ratio has in fact declined over the last decade. Even on the broader measure of total exports (goods and services), the ratio has fallen from a peak of 25.4% of GDP in 2013 to 21.2% in 2024.

The second concern is the exchange rate. The relevant indicator here is the real effective exchange rate (REER), which measures the rupee value against key trading partners after adjusting for inflation differences. India’s excellent performance in the services sector, along with strong remittances, tends to keep the REER more appreciated than it would otherwise be. This hurts labour-intensive manufacturing exports, where intense global competition keeps margins very thin.

Our calculations show that the earnings of the Information and Communication Technology (ICT) sector alone have raised the real value of the rupee by about 3 per cent in 2023.

These findings are not negated by the recent depreciation of the rupee against the dollar. Our calculations relate to the long-term impact of ICT export earnings on the rupee value.

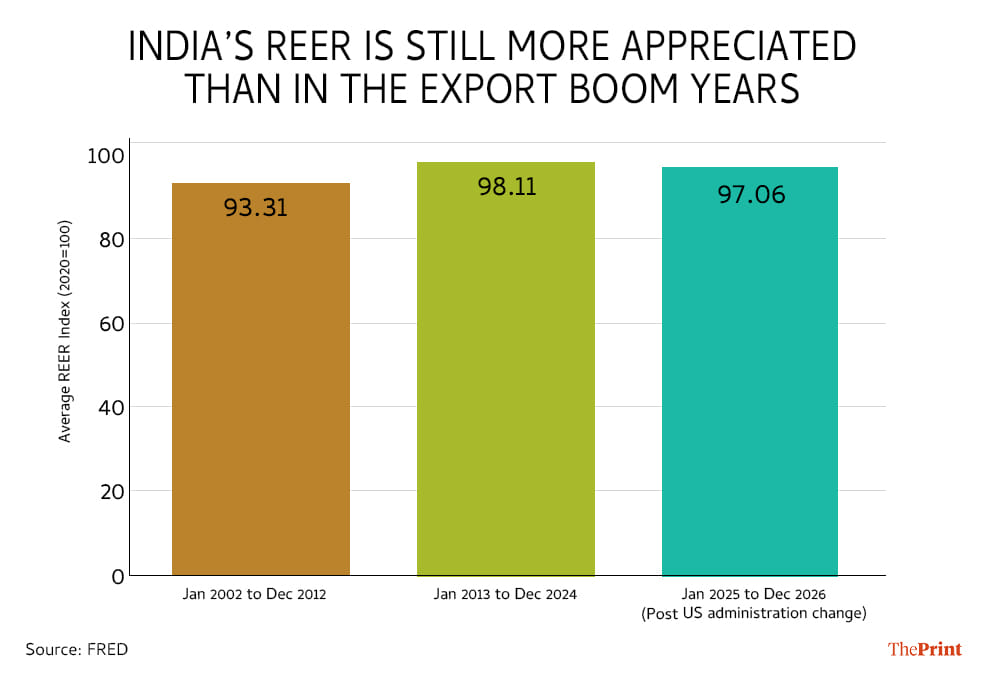

It also bears mentioning that despite concerns about the rupee’s recent decline, the current REER index remains higher than the range observed during the export boom period of 2002-2012. Figures from the FRED database show that the REER rose steadily from an average of 97.6 in 2018 to 103.6 in 2024. By comparison, the REER average during the export boom years was 93.3, versus an average value of 97.1 during Jan 2025 to March 2026 (see figure).

The third concern relates to global value chains (GVCs). GVCs amplify trade volumes, aid technology transfer and support product diversification. India’s policy environment has limited its integration into GVCs: Foreign value added in India’s exports peaked in 2012 before declining thereafter. This limited GVC participation, in turn, truncated the positive feedback loops that GVCs generate and deprived India of deeper manufacturing opportunities.

Also read: The problem with India’s exports isn’t just Trump tariff. It’s the PCI

Tariff roadmap to East Asia pivot

This diagnosis suggests a practical way forward for India to more than double its goods exports over time. We have four suggestions.

First, rationalise tariffs and standards. India should publish a white paper on trade policy that sets out a clear tariff roadmap, firmly links QCOs to transparent safety and quality objectives, and sets out the rationale where protection needs to be maintained (such as in food security and core technology).

Second, sign high-ambition market-access agreements. Deeper FTAs with individual countries and major trading blocs can help mitigate the fragmentation of an increasingly inward-looking global trading order. FTAs preserve market access, anchor within stable institutional arrangements and support integration into global production networks. A major step was taken toward this in January 2026 when India and the EU signed an FTA that had been nearly twenty years in the making.

Third, focus on an export-enabling macroeconomic environment and trade facilitation. India should avoid REER overvaluation, while preserving macroeconomic stability. The current correction in the rupee value should in fact be seen as an opportunity for export growth and a trade reset. Combined with predictable and duty-free access to imported inputs, a more competitive exchange rate would particularly benefit the low-margin, labour-intensive manufacturing sectors.

Fourth, execute a neighbourhood and East Asia pivot. Deepening trade corridors with China, Pakistan, and Bangladesh could help unlock a substantial part of India’s unrealised trade potential. More generally, a pivot towards East Asia is long overdue.

Sanjay Kathuria is co-founder of the Trade Sentinel, a visiting senior fellow at the Centre for Social and Economic Progress, visiting professor at Ashoka University, and nonresident senior fellow at the Institute of South Asian Studies. His X handle is @Sanjay_1818.

Baran Pradhan is former Research Analyst, Centre for Social and Economic Progress.

TG Srinivasan is co-founder of the Trade Sentinel, and visiting senior fellow at the Centre for Social and Economic Progress. His X handle is @tgsv.

Views are personal.

(Edited by Theres Sudeep)

Although the title said “how”, the body contains what and where, not “how”. What Vietnam is exporting is the imported Chinese goods.

Always felt opting out of RCEP was a mistake. The condition of the economy as it now appears after 28th February is the result of conscious policy choices made – in several cases, NOT made – over the last twelve years. Make in India not succeeding, sluggish manufacturing exports, directly linked to protectionism, high import tariffs, not undertaking serious reforms, power sector for example.