After 45 years in business, the underwriter of homes for millions of Indians is moving in with its 28-year-old banker offspring. The joint-family arrangement makes sense for both Housing Development Finance Corp. and HDFC Bank Ltd. Mortgages will get more competitive as lenders come under pressure to peg interest rates to benchmarks not in their control, such as the central bank’s repo rate. Besides, since India’s 2018 mini-Lehman moment, regulators have frowned upon too-big-to-fail monoline financiers lacking access to cheap and assured banking liquidity.

The announcement that HDFC Bank will make an all-stock offer for 100% of parent HDFC has attracted attention because of the size: The $60 billion transaction is the world’s second-biggest so far this year. The enthusiastic investor response to the long-speculated deal suggests that the market capitalization of the bulked-up bank may push toward the $200 billion mark, rivaling China Construction Bank Corp., which is the fourth-largest in the world.

Assuming no assets are shed during consolidation, the balance sheet will top 25 trillion rupees ($340 billion). While that’s half the heft of government-controlled State Bank of India, it’s still a big a number for a private-sector bank of relatively newer vintage. HDFC Bank came into being during the 1990s remaking of India’s Soviet-styled economy. For an international size comparison, divide the rupee value of the expanded firm’s assets by 22 — the value of the dollar tweaked for purchasing power parity. A $1 trillion bank in a nation with $10 trillion in PPP-adjusted gross domestic product ranks ahead of Wells Fargo & Co., which has a $2 trillion balance sheet in the $23 trillion U.S. economy.

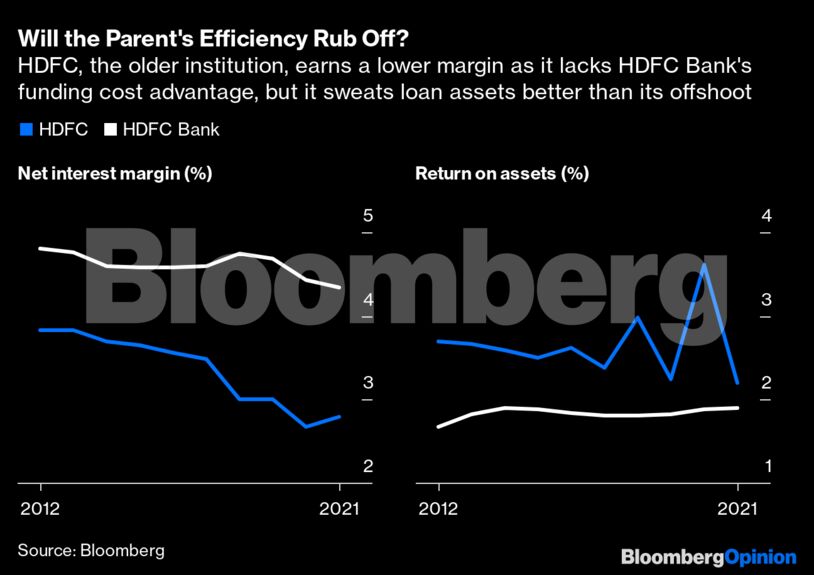

HDFC Bank’s Chief Executive Officer Sashidhar Jagdishan is confident that the acquisition won’t sacrifice flexibility. “Elephants can dance as well,” he says. But sloth has become an issue at the bank. In late 2020, the Reserve Bank of India slapped it with an eight-month ban on digital launches and new credit cards because of frequent technology outages. Thanks to its low-cost deposits, net interest margins have held in the 4% range, whereas for HDFC, the mortgage financier, they’re 1.5 percentage points lower and falling for a decade. Yet, the bank earns a slightly lower return on assets than the 2%-plus garnered by its more efficient parent. As the CEO of the expanded entity, Jagdishan must cut costs and revamp the tech. He also has to make the bank more relevant to Gen Z customers, who want banking to be as intuitive as food-delivery apps.

The older mortgage-finance institution is no digital champion. But it prides itself on its asset quality. Small-ticket home loans to the salaried middle class are usually a safe credit risk for everyone, but HDFC’s 77-year-old Chairman Deepak Parekh, who’ll step down after the merger, also has the reputation of being an unerring collector of lumpy project loans to builders.

Those wholesale loans juice up returns on assets, but they are vulnerable to credit shocks like the one triggered by the collapse in September 2018 of the infrastructure financier IL&FS Group. Following that debacle, Dewan Housing Finance Corp. became the first specialist monoline lender to enter an in-court bankruptcy process with an RBI-appointed administrator at its helm. Later, the central bank wrested control of Reliance Capital Ltd., former tycoon Anil Ambani’s finance firm.

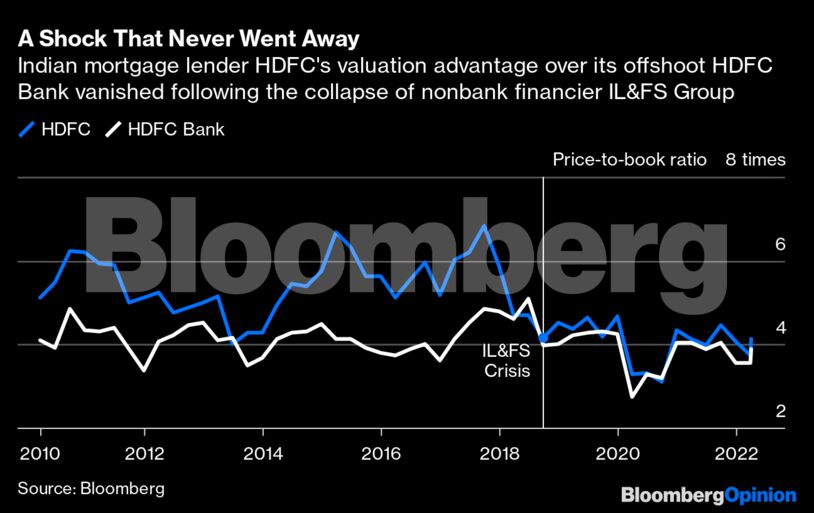

Policy makers would like systemically important lenders to become licensed depository institutions with access to central bank liquidity taps. It seems that’s what investors also want: HDFC’s historical valuation advantage over HDFC Bank has almost disappeared since the IL&FS crisis.

More than half of India’s homebuyers are HDFC customers. That dominance can only shrink as external pricing benchmarks make it easier for borrowers to compare rates from banks and switch. Still, HDFC Bank’s strong franchise in low-cost current and savings accounts could provide a stable home for the parent’s mortgage as well as wholesale lending. Besides, cross-selling banking products to home-loan seekers will give Jagdishan an additional lever against rivals like ICICI Bank Ltd., which is turning a new leaf after a disastrous run of dodgy corporate lending.

For a long time, any new foreign investor coming to India carried an initial shopping list of two stocks: HDFC and HDFC Bank. That was because of the duo’s reputation for good corporate governance and sleek execution. Indeed, no deposit-taking institution in the world is trusted more by savers and enjoys bigger cachet with investors than HDFC Bank. But all that’s in the rear-view mirror. Banking in India is changing. The so-called Unified Payments Interface, a six-year-old public utility, has revolutionized smartphone-based payments. As the two HDFC elephants start their dance, they must be careful — not just of other banks, but of fintech rivals trying to set the tune for both lenders and borrowers. –Bloomberg

Also read: Mortgage financier HDFC Limited all set to merge with HDFC Bank, shares soar