Every business involves taking risks, but farming is inherently riskier given India’s low irrigation coverage that makes it very sensitive to variability to weather conditions, especially rainfall that causes droughts or floods. Only 49 per cent of farming land was under irrigation in 2015-16, with a wide variation across the crops. The loss of production due to crop diseases as well as volatility in agriculture output prices remains high, resulting in variability in farm incomes. One way to cope with the risk in farming is to take crop insurance.

Unseasonal heavy rains have been causing death and destruction in some parts of India recently. Overall, however, we have been lucky as a nation for the past three years with monsoons. It is a rare occurrence for the South-West monsoon (during June-September) to be normal for three years consecutively. The rainfall has been normal this season or above normal in the preceding two years. With the non-farm economy suffering badly due to the Covid pandemic, the agriculture sector with 3.6 per cent growth saved the Indian economy from plunging even more.

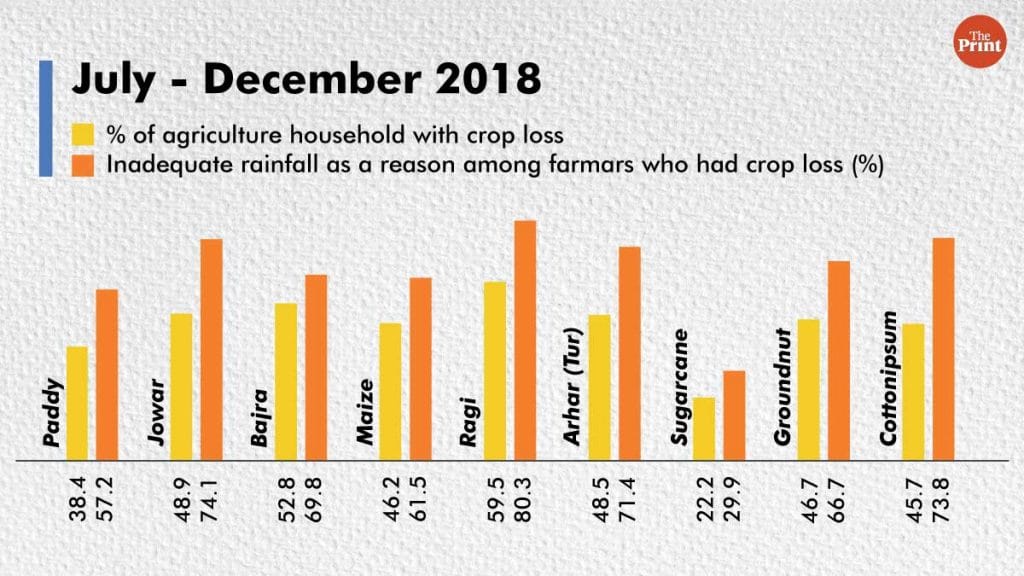

The last time we had a below-normal South-West monsoon was in 2018 when it was 9 per cent below the long-period average. Data recently released shows that from July to December 2018, more than 40 per cent of farmers faced losses in several crops. In a vast majority of the cases, the primary reason was deficient rainfall or drought, followed by a crop disease (Figure 1).

Figure 1

But the adoption of crop insurance remains low in India despite the high risk and multiple efforts by government agencies. The cropped area under insurance was 26 per cent in 2018-19 compared to the government of India’s target to bring 50 per cent of the area cropped under insurance. This is despite an overhaul of crop insurance schemes by the Narendra Modi government in 2016 when it introduced the Pradhan Mantri Fasal Bima Yojana (PMFBY) as well as revisions to the existing schemes such as Restructured Weather Based Crop Insurance Scheme (RWBCIS) and another revamping last year of both the schemes.

Also read: NSS survey on farmers is a mid-term report card of Modi’s promise, with ‘fail’ written over it

Are insurance claims settled?

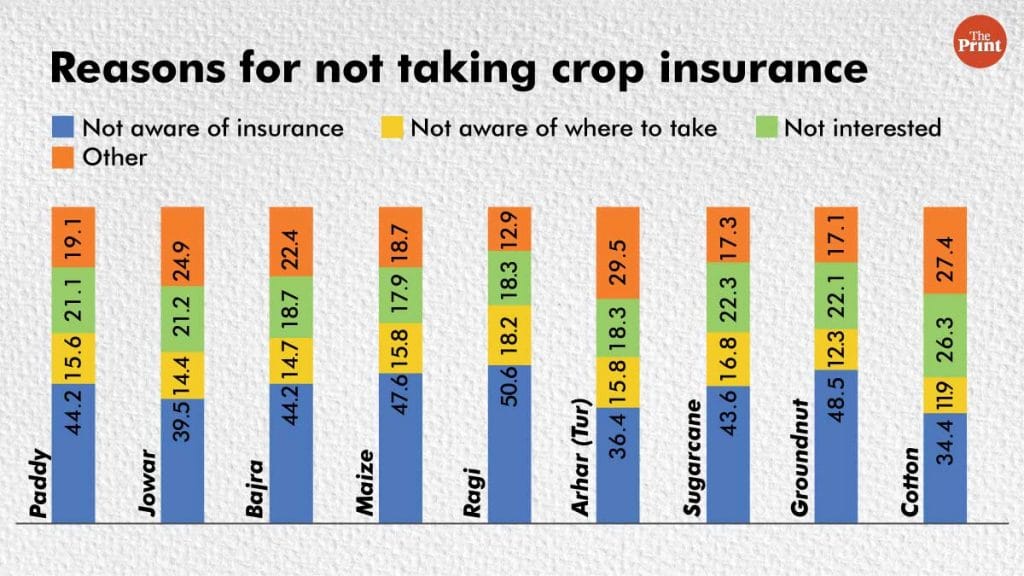

There are several reasons for the low adoption of crop insurance with the primary reasons being ‘not aware of crop insurance’ and ‘not interested’ (Figure 2). This is even when more than half of the agricultural households that insured beyond the mandatory requirement at the time, experienced crop loss in jowar, maize, ragi, arhar, moong, groundnut, soyabean and even coconut from June to December 2018.

Figure 2

The key question is this – even if we make farmers aware of crop insurance and convince them that there is a need for insurance, does it make sense for them to buy crop insurance or would they still remain uninterested?

Buying any insurance – crop, health, accident – is rational on the part of the purchaser if an insurance claim is processed and settled on time. There is little incentive to take out insurance cover if many claims get rejected. What does the data show in terms of claim settlement for crop insurance?

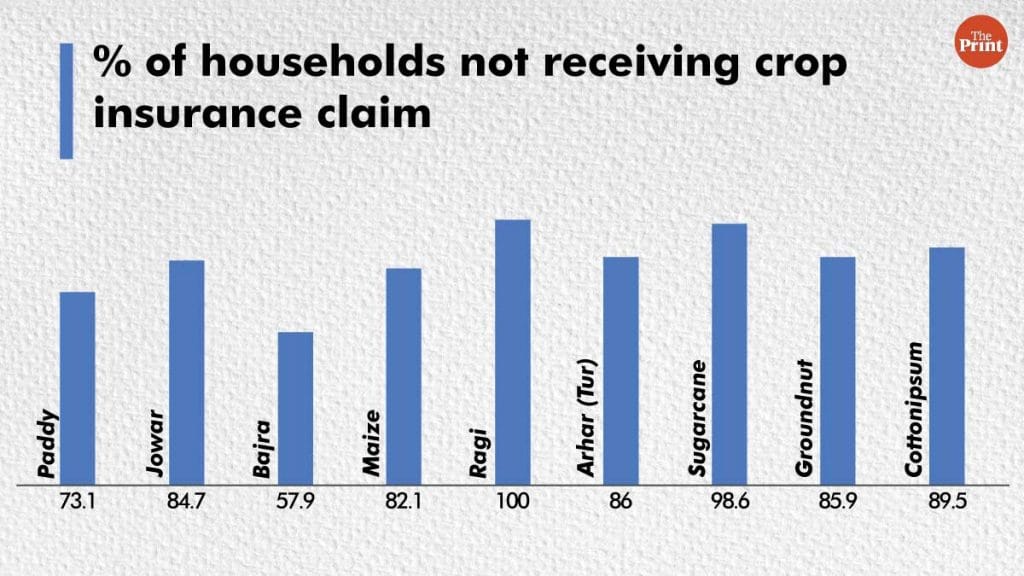

Until last year, for all farmers who took loans on their Kisan Credit Cards, the insurance premium amount was deducted mandatorily from their loan amounts. Some farmers insure their crops separately and not as a part of taking agricultural credit. Among such farmers who insured additionally, during the second half of 2018, depending on the crop, between 70 and 100 per cent of farmers who made an insurance claim for crop losses did not receive the compensation (Figure 3). The best-case scenario was of Bajra farmers, 42 per cent of whom received the insurance they claimed.

Figure 3

If farmers suffer the loss and do not receive insurance compensation, it is a waste of premium payment. During good farming years, there isn’t a need for a claim and during a bad year, the claim is not settled. Even under mandatory PMFBY, while the percentage of claim settlement is higher, the delays in payment have been significant. Recognising the delays in settling the claims and non-payment, the government of India made PMFBY voluntary from 2020 even for farmers who take crop loans from formal institutions.

Also read: Indian farmers need a new distress index. Just suicide data won’t do

Endless delays, no payment

What are the reasons for such dismally low insurance claim settlement? The crop insurance claims are not rejected because they fall outside the coverage of the scheme or documents are lost by farmers. Almost all claims are rejected because of ‘other’ reasons. The other reasons relate to how the crop insurance schemes are structured, funded and implemented.

In recent years under PMFBY, there have been delays on the part of the state governments to pay their share of the premium subsidy. Under the scheme, the central and state governments provide subsidies on insurance premiums, which the governments pay to the insurance company. It was then decided that the states that delayed the release of premium subsidies to concerned insurance companies beyond a prescribed time limit, would not be allowed to implement the scheme in subsequent seasons. In fact, states such as Gujarat, Andhra Pradesh, Telangana, Jharkhand, West Bengal and Bihar left the scheme, citing the high cost of the premium subsidy, defeating the objective of raising the farm insurance cover.

Another reason is the delay of payments in the settlement of claims by insurance companies. To curb that, the government of India instituted a penalty interest of 12 per cent on insurance companies if they delayed settlement of claims beyond ten 10 days of the prescribed cut-off date. Among other reasons for rejections/delays in claim settlement include the delays in assessing the yield and disputes between the insurance companies and state governments over the yield data.

Irrespective of the reason, unless a higher percentage of claims is settled and payment is made on time, a rational decision on part of farmers is not to waste the premium money. Acknowledging the urgent need to fix this issue, the Standing Committee on Agriculture carried out a detailed evaluation of the PMFBY in its report released last August and the Modi government has recently constituted a working group, as per media reports, to roll out a revamped PMFBY from the Kharif 2022 season.

Making crop insurance work well is one of the key ways to insulate farmers from volatility in farm incomes and make farming sustainable, especially as India moves ahead with reforming the agriculture sector. The report of the newly constituted committee, its recommendations, and eventually successful implementation, hopefully, will take us in the right direction.

Vidya Mahambare is Professor of Economics, Great Lakes Institute of Management, Chennai. Sowmya Dhanaraj is Assistant Professor of Economics, Madras School of Economics. Views are personal.

(Edited by Neera Majumdar)