In this episode of Cut The Clutter, Shekhar Gupta explains the economic concerns behind Prime Minister Narendra Modi’s appeal to cut gold purchases, fuel use, foreign travel and fertiliser consumption, linking them to rising import bills, forex pressure and a widening current account deficit.

Here’s the full transcript, edited for clarity:

Prime Minister Narendra Modi’s appeal to cut gold purchases, fuel use and foreign travel comes amid rising pressure on India’s foreign exchange reserves, driven by soaring crude prices, record gold imports and weakening foreign investment inflows.

For the past couple of days, the Prime Minister has been speaking. He is messaging, and his messaging is basically along four axes. These four axes are gold, fuel consumption, foreign travel and fertilisers. In fact, he has gone to the extent of saying that farmers should use 50 percent of the fertilisers they have been using and should go organic.

You cannot go organic so suddenly. We also know that Sri Lanka decided to go organic. It did not quite work out. Nevertheless, we have to understand where he is coming from.

First of all, the four items: gold; fuel, which effectively means crude oil because crude oil then becomes diesel, petrol, kerosene and everything else; travel, meaning foreign travel, which consumes foreign exchange and is translated as spending under the LRS, or liberalised remittance scheme; and fertilisers.

The LRS is something the BJP government started in its later years because it felt more confident about India’s foreign exchange reserves. It also wanted to give people in India confidence, and the rest of the world confidence, that India was not so starved of foreign exchange.

Since then, that scheme has continued. It is the scheme through which Indians travelling overseas spend. Indians can also invest overseas. They can buy assets overseas. They can also spend on education. That is under the LRS basket.

So what am I doing today? First of all, I am trying to explain to you, with data, where this concern is coming from under these four heads, or over these four baskets. Number two, what is it that is compounding this problem for him? And third, what is the upshot of all of this? Because, finally, the upshot is the current account deficit.

The current account deficit then has to be financed, for which the government has to go and either buy dollars in some way or spend out of its reserves. The result of that is a drawdown on your foreign exchange reserves. That is the brief summary of what I am going to say.

Now let us go over it item by item.

Gold first. Why did the Prime Minister say, “Do not buy gold for a year, even for weddings”? Nobody will listen, particularly for weddings. People will buy it. And, funnily or sadly, depending on which side you are on, gold is a commodity where even price is not a nudge. Which means, if the price goes up, people do not buy less gold. As the price goes up, maybe greed comes in and people think gold will go up further, so let us buy a bit more.

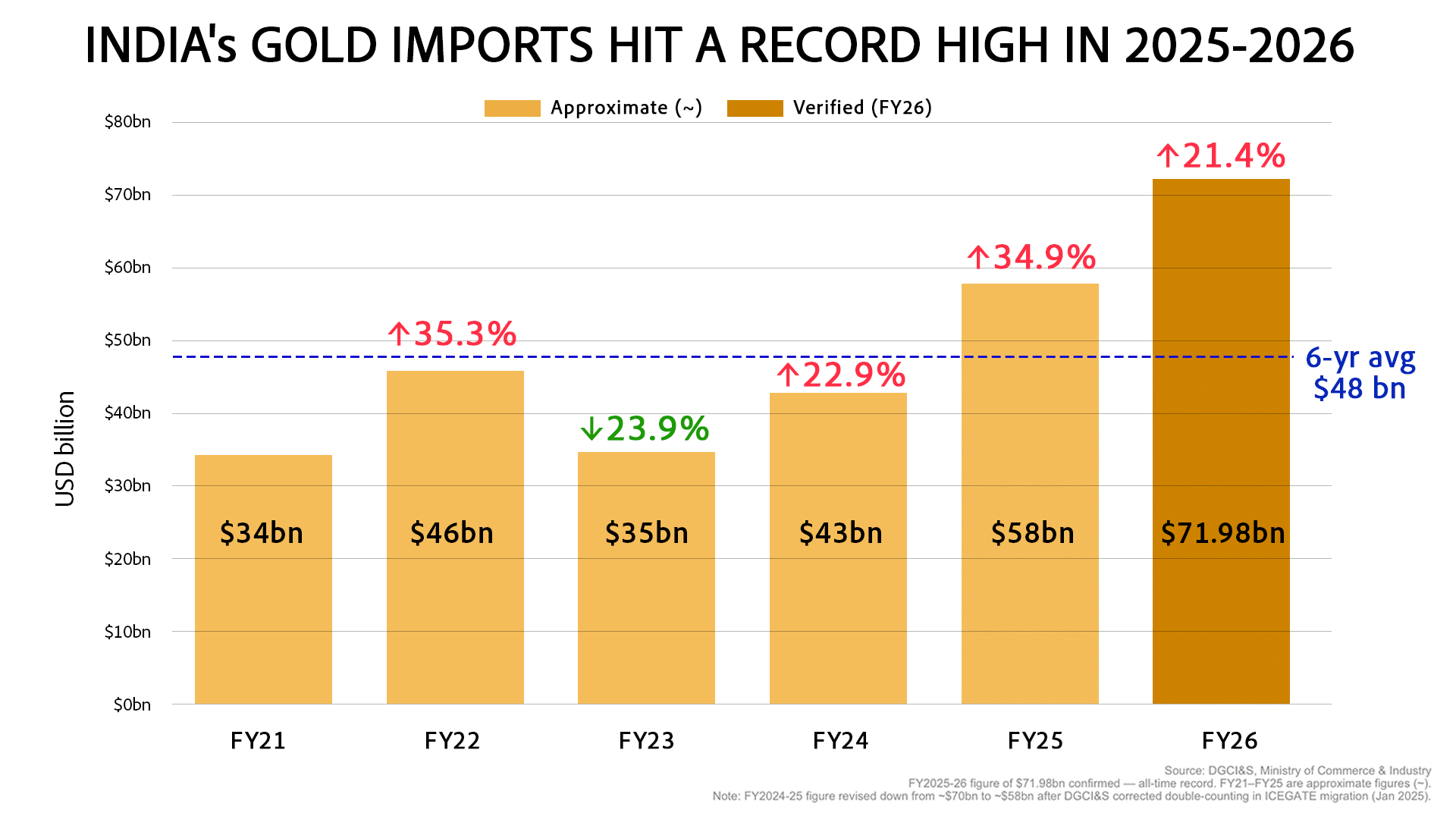

So see what has been happening with India’s gold imports. India imports almost all of the gold it consumes. Almost all. India is also the second-largest consumer of gold, or buyer of gold, in the world after China.

See how India’s gold imports have gone.

Financial year 2020-21 — that is 2021, the Covid year — India did not import that much gold by its own standards. Still, it was $34 billion. That was a year of negative economic growth, substantially so, and yet India imported $34 billion worth of gold.

The next year it went up to $46 billion, which means an increase of 35.3 percent, as India’s economy picked up a little bit.

Then the next year it came down, and I will tell you why. It came down to $35 billion, and the reason is that was when the government increased the import duty on gold from 7.5percent to 12.5 percent.

So the import came down a little, by 23.9 percent. Let me also tell you that from then on, confiscation of gold from smugglers and incidents of gold smuggling also started going up.

Then the following year, financial year 2023-24, gold imports again went up by 22.9 percent to $43 billion.

Financial year 2024-25, again there was a boom and an increase of 34.9 percent to $58 billion.

And this year, the financial year that just ended, 2025-26, our imports of gold have gone up to $71.98 billion, let us say $72 billion.

Now why did I say that gold is a commodity where price does not seem to affect people in terms of curbing purchases? In fact, pricing on gold has the opposite nudge. Usually, when the price of something goes up, people say, “All right, it is too expensive. Let me not buy now. Let me buy less. I will buy next year.” With gold, people do not believe price will ever come down. When it is going up, they think it will go out of my reach, so let me buy and collect now.

So last year, for example, in 2025-26, a lot of households bought more gold because they thought it was going up and up and up. We have done several episodes of Cut The Clutter on how everybody was buying gold. There was a run on gold and on silver, and also central banks across the world were stocking up on gold because of geopolitical uncertainty.

It was in the same year that, because gold was going up, gold ETFs — exchange-traded funds — also became fashionable.

Remember, when a fund house sells you gold ETFs, they have to buy a matching amount of physical gold to pay back in case you call your money. They are not the government. The government issued sovereign gold bonds in 2016. It did not keep any gold. It did not buy any gold and keep it because they are the government; they can do what they want. Since then, they have been changing the tax rules, etc., to try and protect themselves, or try to limit the damage that the scheme has done.

But a fund house has to keep that much gold. Now RBI has given fund houses a little bit of leeway to also buy gold futures, which effectively comes to the same thing. So all this additional gold has been bought in the process.

India’s gold imports have gone up to $72 billion this year, 24 percent over the previous year, which was 35 percent over the preceding year, which was 23 percent over the still preceding year, which in turn was a little bit lower than the year preceding that, financial year 2022, because of the increased duty.

So today, gold imports are $72 billion in the financial year that has just gone past. And as we speak, there seems to be no let-up either in gold purchases or in the purchase of gold ETFs. That has got the government worried that if Indians keep on buying more and more gold, how are we going to find the dollars? Because all the gold is imported. In fact, the largest amount of gold we import is from Switzerland, and then from many other countries — South Africa, the UAE, etc.

Second, come to fuel. Why the worry on fuel? Why is the Prime Minister saying use pooled cars, use public transport, work from home if possible? And this sounds very drastic because the situation has changed dramatically within the past three months.

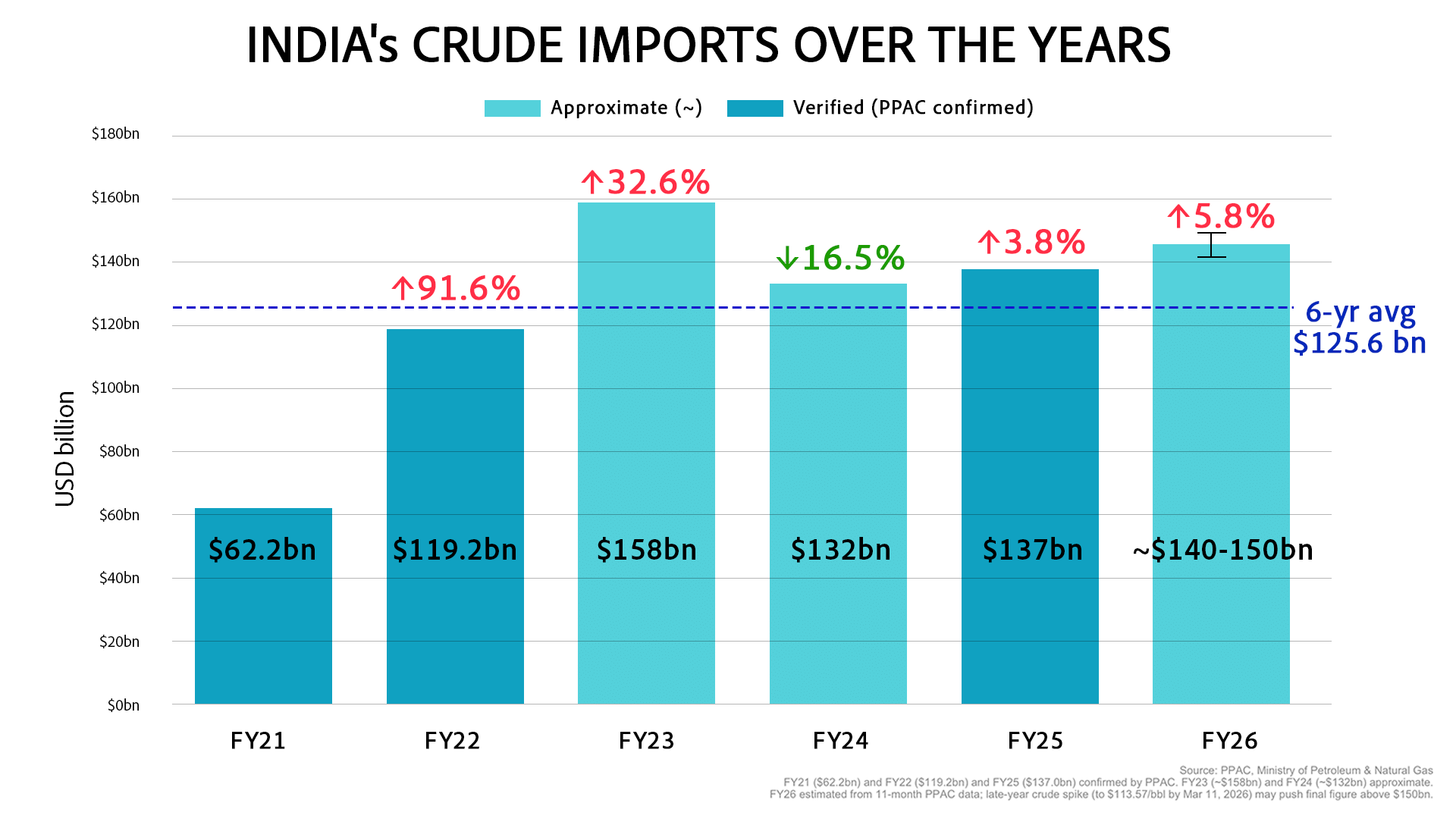

I will give you some data. See this graphic. It tells you India’s crude imports. Again, India imports 85 percent of its hydrocarbon needs, crude and gas. Look at the amount of imports every year.

2020-21 will be an abnormal year. That was the Covid year, year of lockdown, year also of sizable negative growth, so that does not quite apply. Still, we have it there for comparison: $62.2 billion worth of crude.

The next year this went up by 91.6 percent, only 92 percent because the economy opened up. We were no longer working from home, we were going to work, and the economy was booming: $119.2 billion worth.

The next year, boom year again for the economy, it went up by 32.6 percent to a total of $158 billion. Keep counting these billions, because ultimately I will be netting off other billions. These are billions being spent. I will also be netting this off against billions that come in. These are billions that are going out, and then you will see what happens.

What do you get under the bottom line? Financial year 2023-24, that is 2023-24, crude imports in value came down because that is when India started to get the full benefit of cheaper Russian crude, and Russian crude became a very large component of Indian imports. So India’s crude imports, by value, came down, not by volume: by value, India’s crude imports went down by 16.5 percent to $132 billion.

The next year, again 2024-25, it went up to $137 billion, up by about 4 percent. By volume, it kept on rising, but once again we were getting cheaper Russian oil and also global oil prices were moderate. That continued until March 11 of the last financial year. Until March 11, India’s crude basket was between $62 and $70 per barrel, and then on March 11 suddenly it went up to $113-plus. That big a difference came up almost overnight.

Frankly, if you look at all this, that is the word of caution that should have come from the government right then, because a war had started and we knew the consequences of the war. And second, the government should have upped fuel prices right then. That is something we have been saying editorially: please do not wait for elections to take place. This is something that has to be done in the national interest. India is running up these deficits. Foreign exchange is running out. RBI is struggling.

If you postpone a hard decision, it does not soften the impact of a calamity. What we are seeing right now in energy markets is a calamity.

That is the warning Uday Kotak also gave, speaking at the CII, where he said the oil shock has still not hit us because many countries already had stockpiles. Refineries had stockpile of crude, which has been consumed. The real impact of the oil price rise will be felt now.

Last year, 2025-26, India’s total crude oil imports in dollars were about $150 billion. So this has gone up from $137 billion to $150 billion, and that is only after about five weeks of increased prices because of the war. But see what is happening now. If these prices continue, or even if prices settle down at around $90 or $100, then this bill could go up to $170-180 billion. And who knows — if prices remain at $110 and above, as they are now — up to $200 billion.

That will punch a very big hole in India’s current account situation, or India’s foreign exchange situation. That is foreign exchange earned versus foreign exchange spent, because all the energy purchase is in foreign exchange.

So, gold I explained to you; crude I explained to you. This makes us understand why the Prime Minister is saying buy less gold, ideally buy no gold, and also conserve fuel.

Number three: why is he telling people to travel less? Now I told you that Atal Bihari Vajpayee, in his last years — that was the Shining India year — India had had three good quarters of growth, and India, which was always used to being very short of foreign exchange, suddenly had a fair bit of foreign exchange. It was a comfortable situation.

So Vajpayee, Jaswant Singh, Yashwant Sinha, people like them said: let Indians feel good. Why should they go and line up at the Reserve Bank of India for every little expense? Give them a certain amount that they can spend or invest overseas. And that is how LRS, or the Liberalised Remittance Scheme, started.

Before that, I will tell you, when I was going to Pakistan, Afghanistan to cover the wars there, or the Gulf War, or the breakdown of the Soviet Union, or wherever, for a foreign story, I had to go to RBI with an application signed by my editor to ask for foreign exchange. For every country or zone there was a limited amount of foreign exchange allocated. That means you could take that much and no more.

So going to a neighbouring country, it was $165, which means you had to pay for everything — your hotel, your car, your tips, your food, everything — out of that $165. If you were going to Europe, it was about $250.

I will tell you, it was impossible to function as a full-time journalist like that. Nevertheless, we did manage because those were the restrictions.

And if you were going to the Soviet Union, it was very complicated because you only got some of your allocation as dollars. The rest you got in what was called convertible rupees. Theoretically, those rupees could be converted like dollars into rubles in the Soviet Union, where the street price of the dollar was maybe 20 times, 30 times, 50 times the bank price of the dollar. It was a mess. Nobody was able to use that money. Even the hotels would not take those travellers’ cheques of convertible rupees.

It was a big struggle.

All of that was over with LRS. LRS, over time, became quite popular.

And what has happened since then is that whenever India becomes a little short of foreign exchange — although India has been increasing its foreign exchange reserves — whenever India feels a little stressed, they put some sand in the wheel of LRS. Usually, it is by putting tax collection at source. This is different from TDS, tax deduction at source, because tax deducted at source goes to the government. It is gone; it is tax paid. TCS is just collected by the government. At the end of the year, when you file your tax returns, you can take credit for this tax.

So effectively, this tax is paid back to you. Initially, 5 percent tax was put on LRS so that government would keep an easy database. There was a little friction in the process, some sand in the wheel, so people would think, “5 percent will get stuck later.” The Modi government took it to 20 percent to deter people. At that point, for some time, there was a little deterrence. It came down, but then people got used to it, and LRS and foreign spending by Indians have gone up.

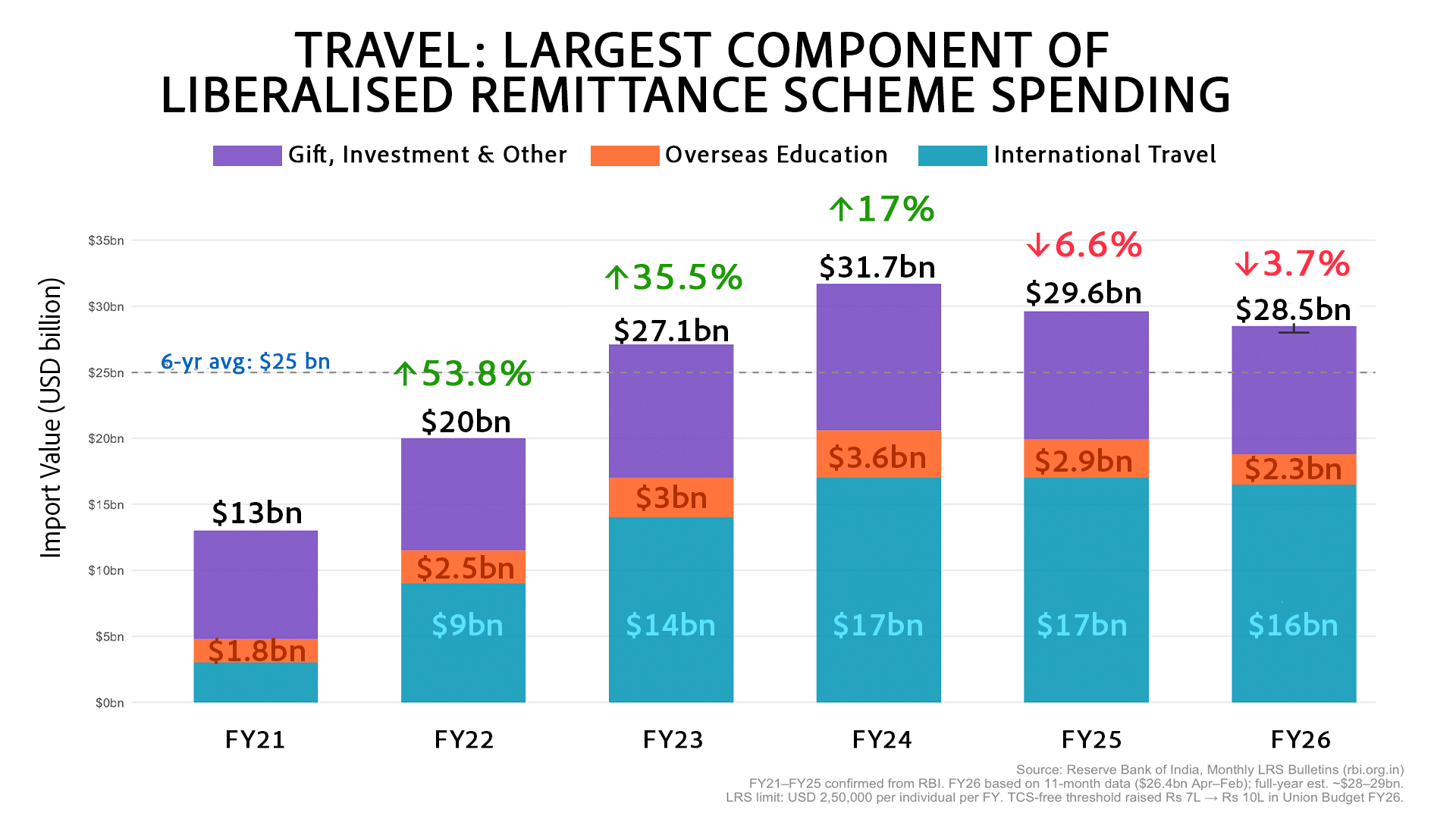

See the trend on this graphic. Once again, 2021 is only $13 billion under LRS. You would expect that because that was the year of Covid. Then next year it has gone to $20 billion, then $27 billion, then $31 billion. It peaked in financial year 2023-24 because that is the year the government put 20 percent TCS.

Now you would have thought 20 percent TCS means people will spend less money overseas to buy bonds, mutual funds, homes, etc., or for education. But no, the opposite happened, because when the government put this tax there were protests. Then the government delayed it, deferred it to October. So a lot of people then thought: we do not know what the government will do tomorrow, so let us quickly go out and spend money. And it is in that rush that LRS spending, or LRS outgo, became the highest.

In fact, it has not been equalled even in the last financial year. 2023-24 was $31.7 billion. Then the next year was $29.6 billion. This year, the year that just ended, it was about $28.5 billion.

Yet, for the government, it is $28.5 billion of foreign exchange gone out, of which about 3-4 percent goes out for education, some for medical treatment, and a lot for asset creation. Maybe the government does not mind it so much if Indians create assets outside, or maybe they do. However, that is one category.

The largest category of spending under LRS is not the mutual funds or properties that Indians are buying in London or Dubai or Lisbon or wherever. It is actually travel. So go back and see on your graphic, and you will see in a different colour the proportion that travel accounts for.

Again, forget 2021 because nobody was travelling in that year. But in the years following that, travel has constituted the largest single component of LRS spending.

Last year it was $16 billion. The year before it was $17 billion. The year before, in 2023-24, it was again $17 billion, because this was also when there was a post-Covid travel boom. People now felt confident and free and thought they could go out. Also, this was the year when Indian stock markets and mutual funds had a boom. The Sensex got to 73,000, and a lot of Indians felt the wealth effect and thought they could spend. And that is how foreign spending and foreign travel went up.

Now the Prime Minister is worried that if this continues, from where will RBI find the dollars to fund it? Because people will go to the bank and ask for dollars. Will RBI keep taking money out of its reserves, or will it let the rupee weaken?

At this point, as we talk, I read from various estimates that RBI, net net, ends up spending from its reserves. It is not exactly spending. It is basically converting its dollars into rupees, about $5-6 billion per week. If that goes on through the year — remember, a year has 52 weeks — that would create a big problem otherwise as far as India’s foreign exchange reserves are concerned.

India is nowhere near the crisis of 1991. Anybody who says so on social media etc. is not talking the truth. At this point, India has reserves to fund about 11 months of imports. A crisis emerges when your reserves are below three months of imports.

At the same time, India is a cautious country. India is also a country which has many plans, many ideas, and nobody knows how long this crisis will go on. So it is better to cover your risks now.

However, once again I would say that at least on fuel, the government should have started at least two months earlier. They did not, obviously for electoral reasons.

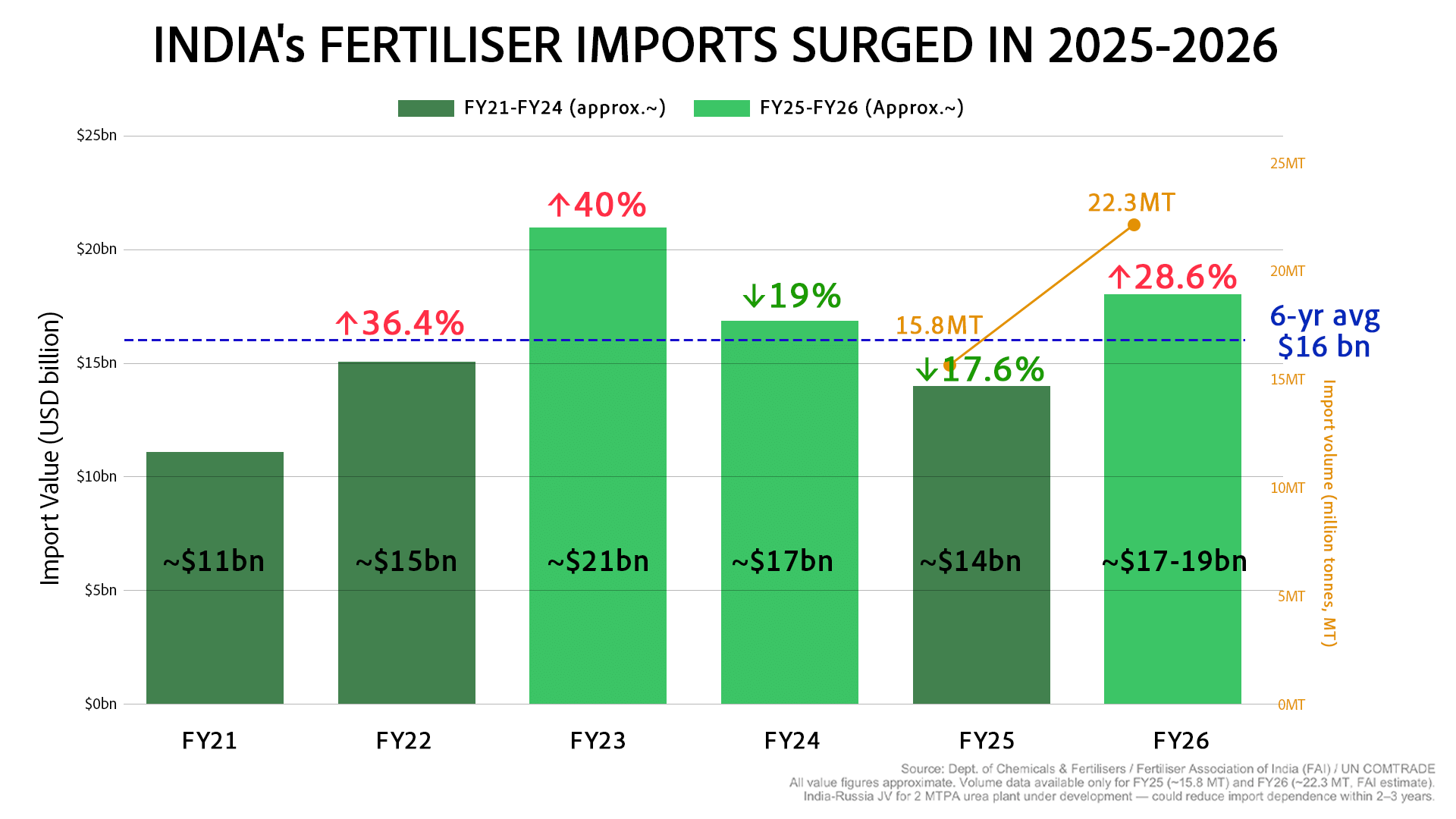

Now why the nudge to farmers to use less fertilisers? Once again, see the chart, and it tells you how India’s fertiliser consumption has trended. Forget 2021. $15 billion worth of fertilisers we imported in financial year 2021-22, $21 billion. It went up to a peak in 2022-23. Remember, that is also a function — we are not talking volumes, we are talking value. It also went up because that is when global crude prices went up because of the Russia-Ukraine war, and also fertiliser supplies were under stress from Ukraine, Russia and from other providers as well. So that year fertiliser prices were high. It went up to $21 billion.

Then the following year, sort of closer to normal, $17 billion. And then the effect of cheaper Russian crude came in, so $14 billion. Last year it was $17 billion. And the estimates for this year, because crude prices have gone up so much, and fertiliser prices have gone up per se, plus fertilisers are in short supply, so you will have to bid for what is available, the estimates now are about $22 billion.

Now, alongside this, two more problems have come in.

One is the FDI issue. India is getting a lot of FDI. Even this financial year, 2025-26, India has got about $90 billion of FDI. But that is inward FDI; FDI has come in. At the same time, there has been a lot of repatriation. Many MNCs which set up businesses in India have done IPOs and taken their money out, because that is why they came. They came to make money.

Also, many Indian companies have invested overseas, so that is outward FDI. You then net off inward incoming FDI with outward FDI or repatriation and see what you are left with.

If you see financial year 2025-26, and you can see every other year, and you can see the trend, in financial year 2023-24 net FDI was about $10 billion. In 2024-25, that is when larger repatriations have started, net FDI is negligible. It is only $0.35 billion, which is really a rounding error, or an accounting error, or pocket change.

And then finally, in the year just concluded, 2025-26, net FDI is just $6.26 billion. We still have something in the plus, but just about $6.26 billion. India can do a lot better than that. India needs to do a lot better than that if India has to balance its current account. That is a very small amount because usually what happens is when you have a trade deficit, you make it up by way of capital receipts, which is net FDI or net FPI inflows. If that goes down, then it becomes that much more challenging for a country to balance its account.

That is the problem India is having right now because if net FPI is almost zero right now, in spite of a lot of FPI coming in — FPI actually is a completely different situation — it looks like the FPI inflows have completely collapsed. And see the numbers there, and these are quite alarming.

In FY 2021, the Covid year, we still had a plus $6 billion net FPI. Net FPI, debt and equity: what that means is people who came and bought your shares and your bonds, and people who netted off against people who sold them and took their money out — $6 billion plus.

FY 2021-22 is minus $20 billion. That is because in that year a lot of people sold their equity, probably because global equity prices were going up, particularly in America, and they moved money there.

Equity investments: plus $19 billion in 2021, minus $17 billion in 2021-22, and now minus $4 billion in 2022-23. So there is an improvement.

Debt: minus $13 billion in 2021, minus $3 billion in 2021-22, now minus $1.5 billion. You net off equity and debt, so you have a total deficit of $5.5 billion on account of foreign portfolio investors in 2022-23.

Then you have the boom year in 2023-24, when Indian markets are doing very well, and that is when, from minus $4 billion, your equity investments from foreign portfolio investors have gone up to $20.8 billion. Your debt investments have gone up from negative $1.5 billion to plus $20.8 billion. That much money is coming in, which means your total inflows from foreign portfolio investors are $41.6 billion. This was a great year.

By next year, Indian equities have started tiring out, as we know in 2024-25, so inflows are minus $5 billion in equities, but still debt is robust at $31.1 billion, and we have a positive balance of $26 billion.

This has changed dramatically in 2025-26, and for the worse. Equity investments are minus $16.5 billion, which means many more people have taken out their money than have brought it into India. Foreign portfolio investors at this point have lost interest in India, as every expert — forget expert, every data point tells you so.

So India has lost. Net net, $16.5 billion has gone out, has been pulled out by foreign portfolio investors in equity. Debt has got a little bit of money. Net net, India has lost $14.8 billion from its reserves on account of foreign portfolio investors losing interest in India.

This reversal in 2025-26 is quite stark, in fact, and quite worrying. This is something that probably needs policy attention. There is no point cursing the foreigners and saying that if FPIs do not come to India, we do not care; we have our Indian investors, they will take their SIPs.

The fact is that the Indian middle class, which has been buying SIPs for two years, has hardly made any money on their SIPs. It is still keeping the faith, but one, you cannot count on it forever. Maybe they will start switching to gold, as some of them seem to have done lately. And second, it is not even fair to them.

Now let me try and explain this as a non-economist — an absolute non-economist effort — although I have been helped with data, research and also graphics by Dr Bidisha Bhattacharya, who is our consulting editor for economics and writes a column, Economics with an X, that you read and watch every week.

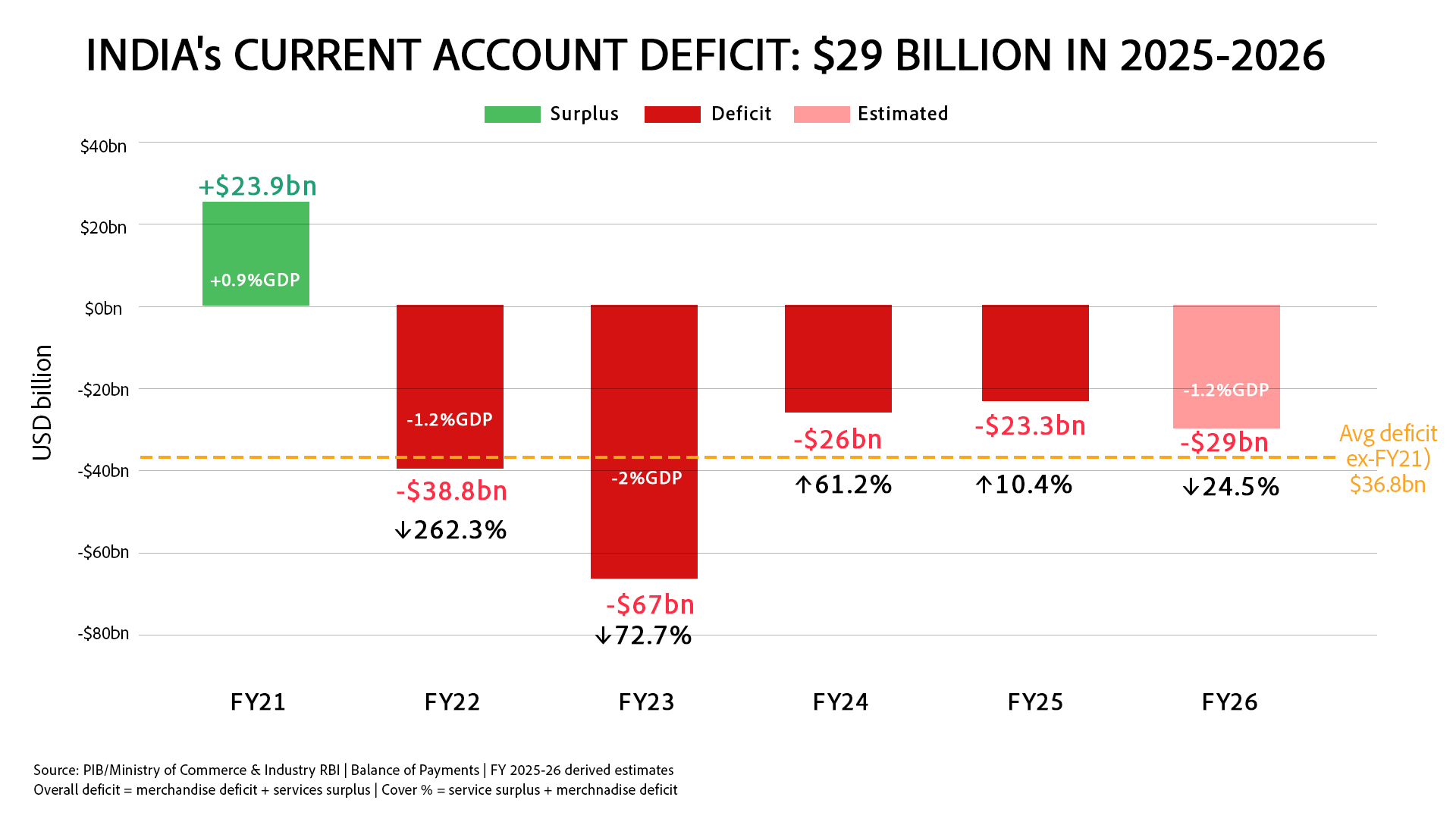

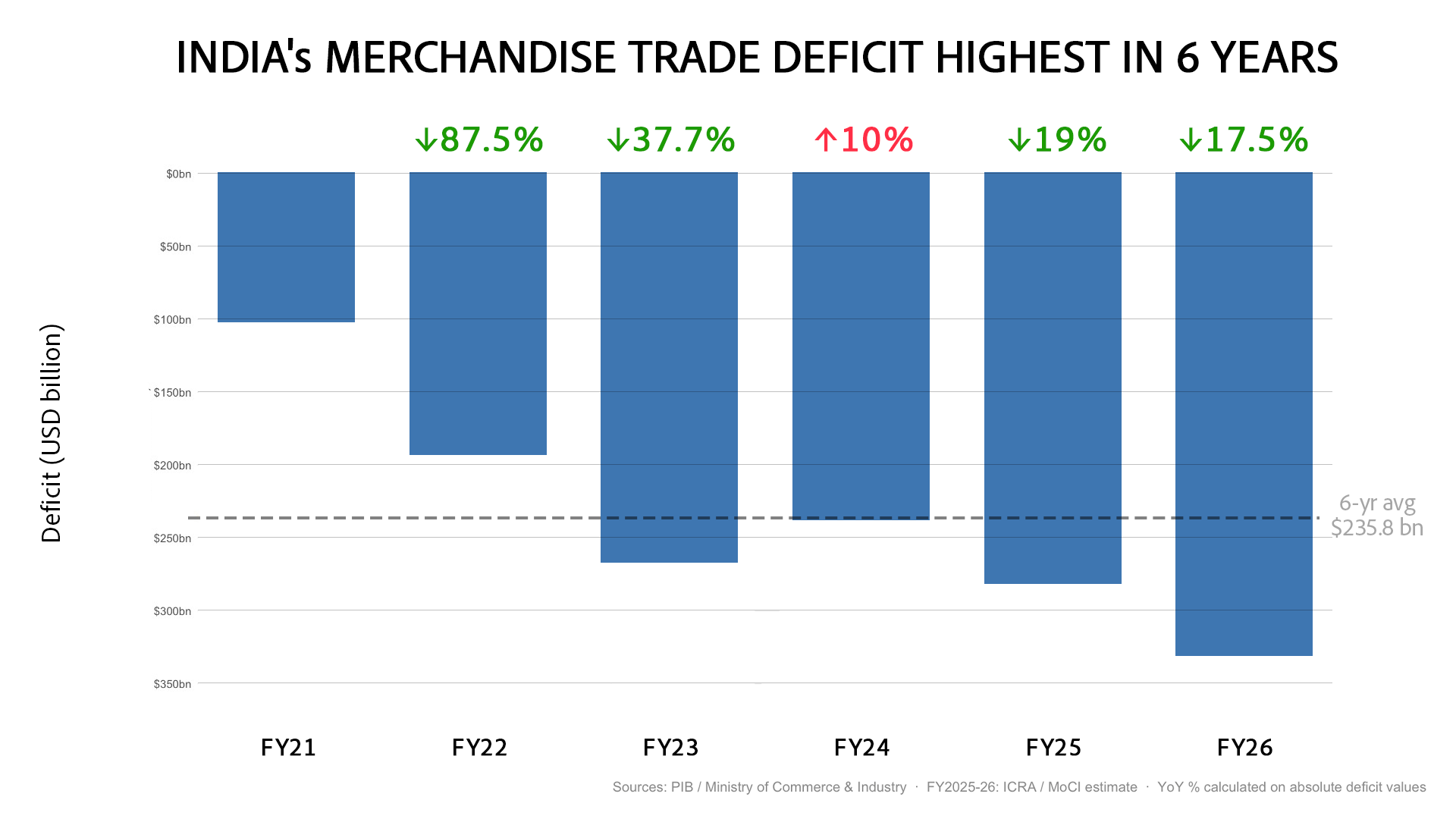

Look at this data and look at this graphic. This tells you merchandise trade deficit. These are goods, commodities, products that you buy from overseas, you import, and that you export. What is the net situation? The net situation is that India almost always has a negative balance on merchandise trade.

Covid year, of course, it is very little because we imported very little. We also did not export that much, but we imported very little. Consumption was down. The next year it went up, and went up again. The merchandise trade deficit became the highest in financial year 2022-23 so far, mainly because that year I suspect the crude prices globally went up.

The next year it improved a little bit. The next year it improved a little bit. It was still about $240 billion — not small change — of merchandise trade deficit. And yet it got worse in 2024-25, and 2025-26, the year that just passed, we got our worst number ever: an all-time record, but a dubious record, of a merchandise trade deficit of $333.2 billion.

What happens when you notch up a merchandise trade deficit, and it has been happening to India forever? India does not have a crisis? How come 1991 is not back with us?

That is because India has built a big business in services. So a lot of our merchandise trade deficit is made up for by services. Check therefore this graphic.

What this graphic tells you is, number one, the big thick bars are your merchandise deficit. Then in green, underneath the bar, you have figures that tell you the surplus that you have from services trade. So you import some services, you also export services. That is always in surplus.

It also gives you the percentage of the merchandise deficit that your services export surplus covers. So in 2021, the Covid year, it covered about 86.7 percent. So in the Covid year we almost were even-steven on our current account.

The next year it covered 55.6 percent. Then next year, 54 percent. Then 68.4 percent because we had a boom in services exports in financial year 2024-25, 60.7 percent.

You will also see the numbers of your services export surplus. And even in a tough year like 2025-26, when we have notched up a merchandise export deficit of $333 billion-plus, more than 57 percent has already been neutralised by our services trade surplus.

So please, for heaven’s sake, when we talk about manufacturing, yes, talk about manufacturing. India needs a lot more manufacturing. India needs to reduce that merchandise trade deficit. But also give a little bit of applause to your services industry, which is making up for a lot of that deficit.

Then what happens? You see your current account deficit, and then you see all the other money that comes in. You see salaries. People earn salaries from overseas. You also see remittances.

India gets almost $140-150 billion in remittances from people working overseas. A lot of them are from the Gulf. In fact, 40 percent of all our foreign remittances come from the Gulf. That can be under strain as well if the war resumes in the Gulf.

All of those remittances and other incomes — remittances are a big income. Big income in the sense that dollars come into India. Convertible currency comes into India. All of that then makes up for a lot of the deficit.

At the end of the day, last year, 2025-26, India was left with a current account deficit of $29 billion. The previous year it was $23.3 billion. The year before that, in financial year 2023-24, it was $26 billion. And the year before that, $66-67 billion. Remember, that was the year when oil was very expensive. And this year, if anything, it promises to be, or threatens to be, even more expensive than that.

So, at the end of everything, after your services export surplus, remittances, etc., you are still left with a deficit. That is your current account deficit. And that is what then RBI funds by dipping into its reserves.

I do hope that all of this gives us an idea of where the Prime Minister is coming from. Why is he so concerned as to almost raise an alarm, or multiple alarms?

That said, I will conclude with a little bit of humble opinion.

Number one, the four things that he has talked about. Gold: gold for Indians is an emotional thing. It comes from the heart, not from the head. And in fact, if they get the sense that there is going to be a bigger global economic crisis or an Indian crisis, unfortunately, they will run more towards gold, not away from it. Whatever the wisdom in what the Prime Minister is saying, that is the way we Indians think.

Number two, fuel. Just as with gold, price rising does not work as a nudge to buy less. With fuel, the opposite applies. With fuel, price is a good nudge to reduce consumption. Fuel prices should be increased. There is no issue in increasing fuel prices. If crude goes up, if the raw material goes up, if inputs go up in price, then my pump price also has to go up. It has to be passed to the consumer. Unlike the UPA, we do not expect this government now to create some innovative oddity like oil bonds, which basically means stealing from our next generation to subsidise ourselves. So fuel prices will be a good nudge, and fuel prices should go up. All elections are also over. Although this government should not have waited for elections, they should have done the right thing by the economy. But they should do it now.

Number three, fertilisers. I do not think you can tell farmers immediately to consume less fertiliser. Again, that is a reform that has been in the works, and it works in fits and starts. This is the time to work on that reform for judicious use of fertilisers and also for changing crop patterns to make them more sensible and more market-friendly. That will take time. But a crisis is a good time to begin.

And as far as spending overseas is concerned, I will not be surprised if the government throws some more sand in the wheels. But remember, when you add taxes, tariffs or duties on gold to a certain level, beyond a certain level, it starts gold smuggling. That is what created the Dawood Ibrahim phenomenon.

And it is a story that I have told you before, but I will tell you now. When Dr Manmohan Singh opened gold imports, I had my colleague Sheila Bhatt set up a phone call with Dawood Ibrahim. I used to work in India Today then. And I, with great delight, told him.

He said, then he said, then he said — just for effect, it was going on at that point — with a touch of irony. But the fact is that higher taxes on gold imports will create arbitrage for smuggling. And similarly, any onerous restrictions on Indian spending overseas will then create an incentive for hawala and illegal transfer. So the government has to be very careful, but it has to do all the right things.

It also has to think about why FPIs have given up on India. It has to attract FPIs back.

And finally, before you tell Indians not to travel overseas, what have we done to get foreign tourists into India? India’s foreign tourist arrivals have been going down. We have rarely touched our pre-Covid levels in India.

And if you see the government people talking, they seem to suggest that we have enough internal travel. Indians are travelling, planes are full, hotels are full. Why do we need foreign tourists?

We need foreign tourists because, number one, they bring foreign exchange. Number two, as they come in, Indian tourism infrastructure — from aviation to buses to taxis to everything — will expand. And third, tourism creates more jobs than almost any other activity.

Those are areas India has to focus on, on the positive side. There is no point saying we do not care about foreign tourists. We do not care about FPIs. We have to care about all of them. India needs both.

India needs some self-denial on the part of citizens. That is what the Prime Minister is asking people to do. But at the same time, India needs the government to go out and find solutions to this problem. And some of those solutions are entirely virtuous.