The currency has set a string of record lows, shadowing India’s optimistic world-beating economic growth.

Mumbai: The Indian rupee and bonds sunk after the current-account deficit widened to the most in five years, as an emerging-market rout raises investor scrutiny of countries with worsening balance of payments.

The rupee slid as much as 1.3 per cent Monday to a new low of 72.6738, leading losses among Asia’s emerging-market currencies. Sustained weakening has prompted authorities to ask the central bank to intervene more aggressively to support the currency, people familiar with the matter said.

“While the Reserve Bank of India has been intervening in the FX market, the size of recent intervention looks to be a lot less compared to before,” said Khoon Goh, head of research at Australia and New Zealand Banking Group Ltd. in Singapore. “The rupee’s continued decline stems from dollar strength and concerns over India’s external position.”

State-owned lenders were seen selling dollars, possibly on behalf of the central bank, around 72.50-72.65 levels in early trading, Mumbai-based traders said. The banks were subsequently not seen intervening heavily, they said. The rupee closed down 1 per cent to 72.4575 per dollar.

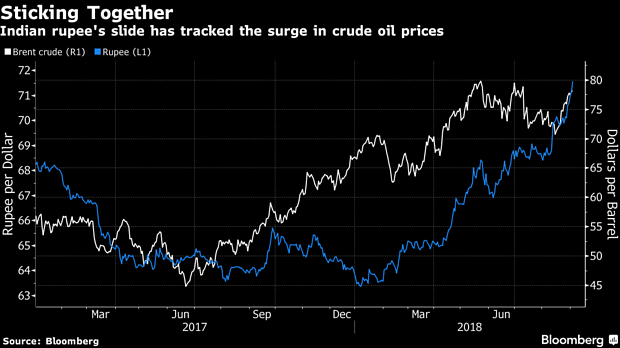

The rupee has been roughed up in the past month amid a selloff sweeping emerging markets following a rout in the currencies of Argentina and Turkey. The currency has set a string of record lows, dampening some of the optimism about India’s world-beating economic growth that sent the local stock market to record highs last month. The weakness is credit negative for companies which generate revenue in rupees but rely on U.S. dollar debt to fund their operations, Moody’s Investors Service said Monday.

The government is conscious about the rupee’s slump, and the central bank is intervening when needed, a finance ministry official said, asking not to be identified citing rules. The government may take steps, including introducing a deposit plan for overseas Indians, to stem the selloff, the official said.

Oil Shortfall

The comments helped the rupee pare the day’s losses that were fueled in part by data that showed the current-account gap widened in the June quarter to $15.8 billion The benchmark yield climbed 13 basis points to 8.16 per cent, the highest since 2014, while the 30-stock S&P BSE Sensex had its biggest drop since March.

The deficit represented 2.4 per cent of gross domestic product, more than the 1.9 per cent seen in the March quarter, according to the RBI. The worst may be yet to come as the oil import bill for the world’s fastest-growing oil user surged 76 per cent in July from a year earlier to $10.2 billion.

The gap will probably widen to 2.5 per cent of GDP for the year amid rising commodity prices and fund outflows, said Dhananjay Sinha, an analyst at Emkay Global Financial Services. He expects the rupee to weaken further to as low as 75 per dollar and sees the benchmark yield reaching 8.40 per cent.

Global funds sold $601 million of India’s bonds this month, more than the combined $459 million that they bought in July and August. Concerns over an oversupply of sovereign bonds had contributed to the selldown earlier this year, and there are little signs of relief.

The right level for the rupee is 68-70 per dollar, with 72 being “perhaps an outer limit or beyond the reasonable outer limit for depreciation,” Economic Affairs Secretary Subhash Garg told the Economic Times in an interview. “Those operators who are trying to take advantage of this contagion feeling in emerging markets may come to grief later,” he said.-Bloomberg