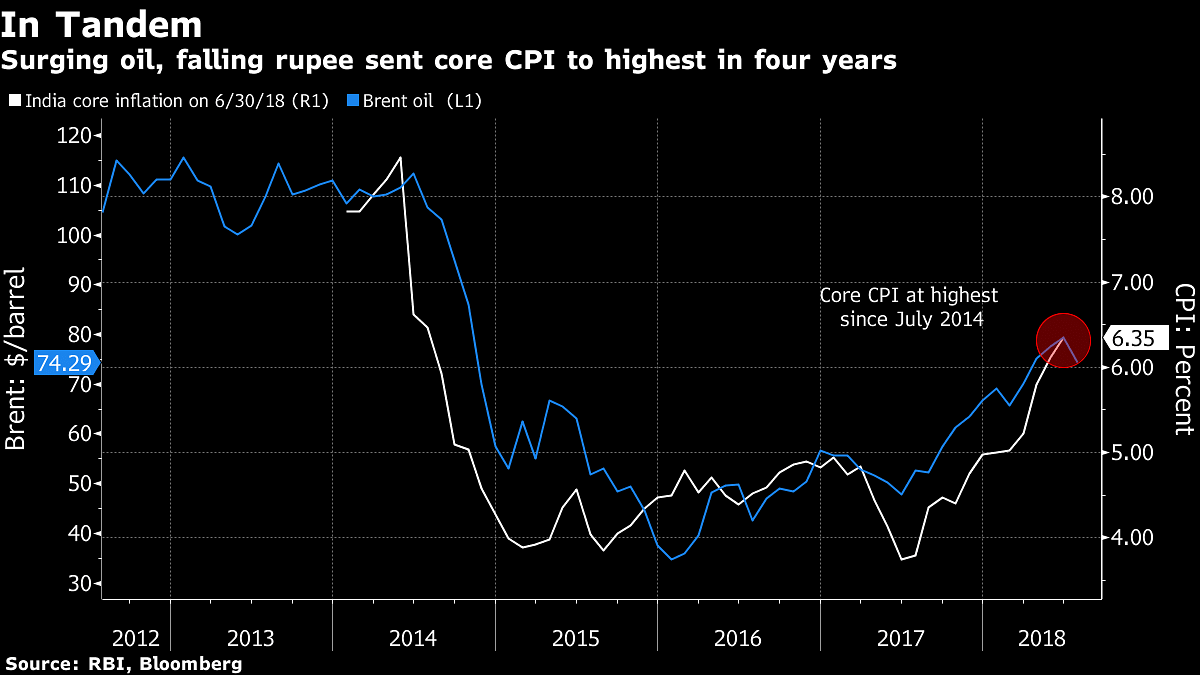

Surge in oil prices & a falling rupee are mounting pressure on the central bank to act soon while inflation keeps rising.

India’s central bank is on course to raise interest rates for a second consecutive policy meeting as it takes more decisive steps to rein in inflation and stem capital outflows.

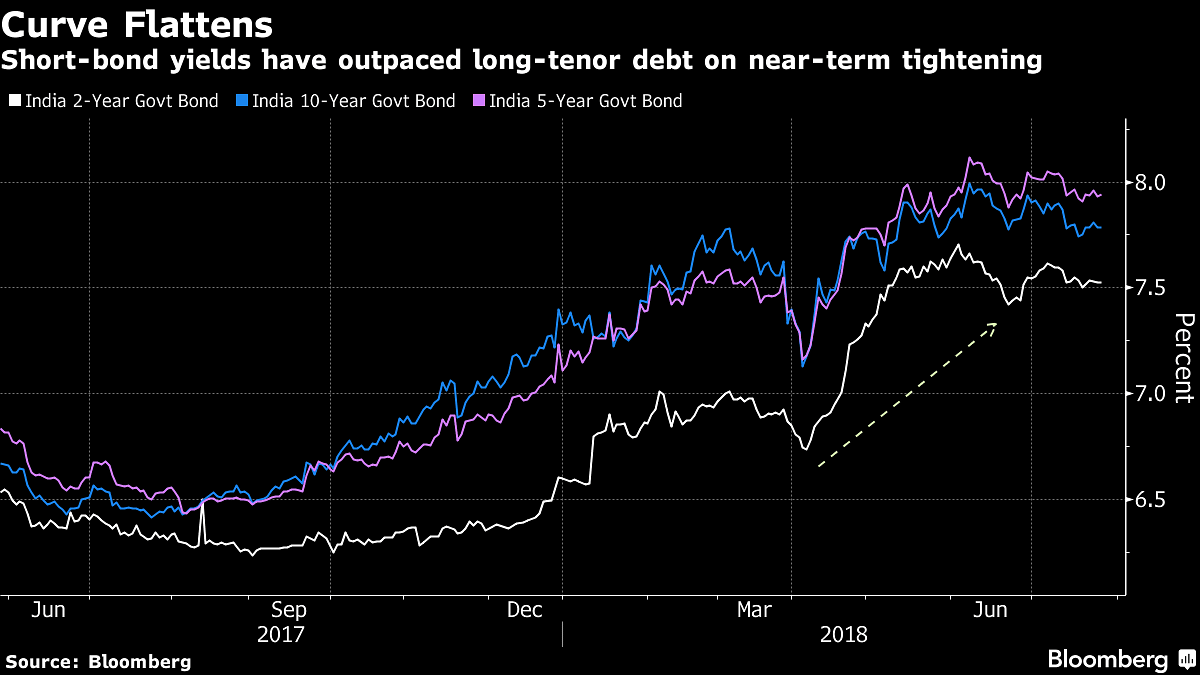

With inflation running well above the central bank’s medium-term target of 4 percent – and the outlook set to worsen as oil prices stay elevated and the currency slides – pressure is building on the Reserve Bank of India to act. Bond investors are already taking shelter in shorter-term debt amid concern this could be the start of a tightening cycle.

“It’s a great time for the RBI to hike rates because people are worried about inflation and growth numbers are looking good,” said R. Sivakumar, head of fixed income at Axis Asset Management, which oversees about $11.5 billion in assets. “By December, if growth falls off, then hiking in December or later will get more difficult.”

Bond investors and a majority of economists in separate Bloomberg surveys predict the RBI will hike by 25 basis points, taking the repurchase rate to 6.5 percent on Aug. 1. Many of them are also watching if the monetary policy committee will shift to a hawkish stance, a move that will spell more pain for bond market.

A rate move will take the benchmark to a two-year high, following June’s 25 basis-point hike. Like central banks from Turkey to Indonesia, the RBI has been propelled into action amid an emerging-market rout triggered by rising U.S. interest rates and a stronger dollar.

Domestic inflation worries are mounting: the economy is rebounding, government prices for some food crops have been raised, and fuel costs are increasing.

The yield on benchmark 10-year bonds has surged 45 basis points this year, rising above 8 percent in June for the first time in three years. Short-term yields have risen more in anticipation of further policy tightening in the near term, with money managers including Kotak Mahindra Asset Management Co. buying debt maturing in less than five years.

“The market view is that it won’t be a long rate-hike cycle,” said Arvind Chari, head of fixed income and alternatives at Quantum Advisors Pvt. “If they raise rates by 25 basis points and keep the stance neutral, markets will be okay. If they change the stance to tightening, then you’ll see bond yield going up to 8 percent,” he said.

Whether the debt selloff will continue or not depends on the message from the six-member MPC headed by Governor Urjit Patel.

What our economist says….

On stance:We expect the RBI to be mildly hawkish in its commentary on Aug. 1 — given the pickup in the latest two monthly readings on headline and core inflation were in line with expectations — and signal a data-dependent policy path.On policy:We think it’s already done enough, and expect it to hold. — Abhishek Gupta, Bloomberg Economics

A rate hike may provide some respite to the rupee, the worst-performing major currency in Asia this year, which is hovering near an all-time low. Its 7 percent drop this year has driven up the cost of India’s imports, especially oil, a bulk of which is bought overseas.

Pipeline pressures indicate inflation would remain under pressure. Data showed wholesale prices quickened to 5.77 percent in June, the highest since December 2013, while consumer prices rose 5 percent and core quickened to 6.5 percent.

While headline inflation could ease in July, Prime Minister Narendra Modi’s offer of higher crop support prices for farmers may spur the RBI to tweak its second-half inflation forecasts.

“We expect headline inflation to moderate temporarily in July, before rising toward the 6 percent mark later this year driven by higher food inflation,” economists at Goldman Sachs Group Inc. led by Nupur Gupta wrote in a recent note. “We recently added two more 25 basis points rate hikes to our forecasts for 2019, and now expect the RBI to hike cumulatively by 100 basis points between now and the end of 2019.”

Below are key Asian economic data and events due this week:

Monday, July 30: Japan retail trade Tuesday, July 31: BOJ policy decision, China manufacturing PMI, Japan and South Korea industrial production, Taiwan GDP, India fiscal deficit Wednesday, Aug. 1: RBI policy decision, Japan, Indonesia and Malaysia PMI, New Zealand unemployment data, South Korea and Indonesia CPI Thursday, Aug. 2: Japan foreign-bond buying, Australia trade, Singapore PMI Friday, Aug. 3: Australia and Japan services PMI, South Korea current account, Sri Lanka rate decision – Bloomberg