Mumbai: India delayed the introduction of tough new accounting rules for the second year running, in a move that will spare the country’s banks from adding another layer to the $190 billion pile of bad loans on their books.

The Reserve Bank of India said late Friday that legislative amendments needed to implement the new Indian Accounting Standards are still under consideration by the government. “Accordingly, it has been decided to delay the implementation” of the rules “until further notice,” the RBI added in a statement on its website.

The new rules — based on the IFRS9 standards created in the aftermath of the financial crisis — were supposed to kick in at the start of the new fiscal year that starts on April 1, after being delayed last year. According to Fitch Ratings’ local unit, India’s state-run lenders would have had to increase provisions by as much as 1.1 trillion rupees ($16 billion) in the fiscal first quarter ending June 30 if the rules had gone ahead.

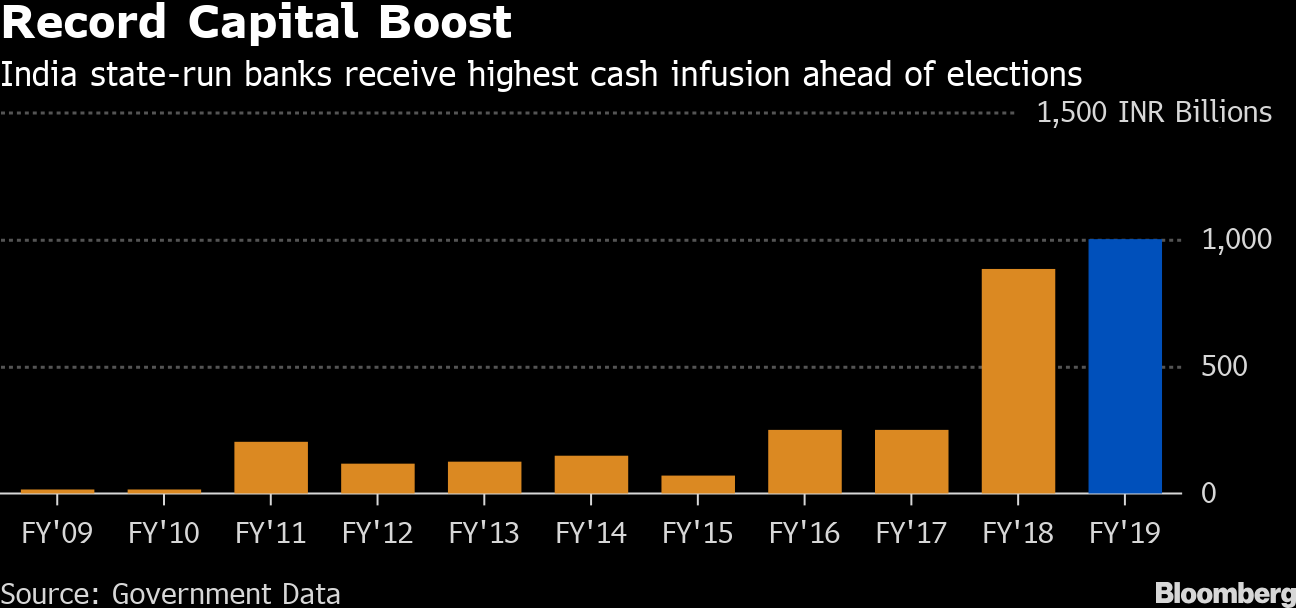

That would have forced public sector lenders to raise “substantial” amounts of extra capital, beyond the estimated 1.9 trillion rupee infusion already committed by the government for the two-year period to the end of this month, Fitch’s India Ratings & Research said in a report last month.

Last April, the RBI delayed the implementation of the new standards a few days into the start of the current fiscal year, citing the need for legal changes and more preparatory work by the country’s banks. The new accounting standards would require banks to make provisions when they judge that a loan is likely to sour, rather than waiting for the borrower to start missing payments.

The impact on Indian banks as a whole would have been less this year than last, said Parthasarathi Mukherjee, chief executive officer of Lakshmi Vilas Bank Ltd., speaking before news of the RBI’s latest deferral. Indian banks have taken hefty provisions and write-offs in past years, and there are early signs that asset quality is improving, Mukherjee said.

“The system has overall mostly seen through its challenges on asset quality,” said Mukherjee.

Also read: Rupee’s advance seems to be causing some discomfort for RBI

One hopes Shri Mukherjee’s assessment is accurate. With the problems in the NBFCs, consumer spending, the last pillar propping up the economy, is beginning to sag. Huge pile up of unsold vehicles is just one visible sign of the slowdown. Once the marigold garlands and showers of rose petals are done with on the evening of 23rd May, some Michelin starred chefs should be invited to take over the kitchen.