New Delhi: Utsav Kumar, a resident of East Delhi, has been struggling to shake off his iPhone obsession. He waits every year for the latest version and buys it. Last month, he borrowed Rs 40,000 from the app KreditBee at a high interest rate of 22 percent to buy the latest iPhone 16.

“I can’t get rid of my obsession with the iPhone. I buy it every time it is launched, but it is not possible to buy an expensive phone with a salary of 25,000 in a private job, so I take money from instant loan apps,” said 24-year-old Utsav as he sat home swiping on his new phone. He has to pay Rs 48,800 across 12 instalments.

He cares not about the exorbitant interest rates these non-banking financial companies (NBFCs) charge, but the amount of credit which is easily accessible. Till 2022, he used digital lending apps to take loans and paid back all the money with the help of his family, but this year, he fell into the trap again.

Utsav recounted that as the launch date of the new iPhone drew closer, he was unable to work out a plan for buying it this time. But then, he began seeing ads for loan apps on Instagram and Facebook, and found KreditBee. The digital landing application claims that it offers the disbursal of loans ranging from Rs 10,000 to Rs 5 lakh in 10 minutes and that it is “trusted” by over 14 crore Indians.

An Instagram ad for another NBFC, Hero Fincorp, reads: “Get an instant personal loan up to 5 lakhs. Rate of interest starting from 1.58% per month and 19% per annum.”

On one end of the spectrum of the customers of NBFCs are Utsav and others, who take huge loans to feed their fascination for expensive items. On the other are those who have to borrow to make ends meet. Rising household expenses, financial instability and personal needs end up forcing people to seek high-interest loans and spend their entire monthly salary on repayment.

Dinesh Kumar Yadav, a government school teacher from Uttar Pradesh’s Jaunpur, is currently repaying Rs 45,000, amounting to about 95 percent of his salary, to various instant loan apps, such as KreditBee, Poonawala Fincorp and Chinmay Finlease, every month.

The 35-year-old had borrowed Rs 72,000 from KreditBee at an interest rate of 32 percent, and Rs 1 lakh from Poonawala Fincorp at 28 percent. From the latter, he got only Rs 92,000 as the rest was deducted as processing fee. All instant loan apps usually charge two-four percent of the loaned amount as processing fee. He is repaying Rs 5,774 to KreditBee, and Rs 10,046 to Poonawala Fincorp in monthly instalments.

“My wife had to undergo IVF (in vitro fertilisation) treatment which required a lot of money, so I borrowed from these apps this year. I pay the money every month, but this time, I missed one instalment and the recovery agents harassed me. They even called my relatives,” said Yadav. The money from the apps went into building a house, too, besides other expenses.

Yadav said that instant loan apps are addictive. “But they cannot be blamed completely because the common man is often unable to manage his finances, and is then forced to take loans at high interest rates.”

ThePrint reached out to spokespersons of loan apps KreditBee and True Balance for a comment on the trends and the interest rates offered by them, but no response was received.

Also Read: Individuals, businesses are increasingly defaulting on microloans. Both lenders & borrowers at fault

RBI’s stance

Unsecured loans, which are given out by banks and NBFCs without collateral to back them up, have been a matter of concern for the Reserve Bank of India for a while now. In November last year, after several statements by policymakers about the sharp rise in such loans, the RBI took steps to make it more expensive for banks and NBFCs to give them out. The rationale was that making it more expensive to give unsecured loans will make it costlier to take them, and thus deter such borrowing.

This seems to have worked to some extent, with the growth in unsecured loans slowing down since then, but it hasn’t managed to discourage a large number of people determined to finance their consumption expenditure via debt.

In fact, a few weeks ago, RBI barred four NBFCs, including two microfinance institutions, from sanctioning and disbursing loans for charging exorbitant interest rates from borrowers, under Section 45l(1)(b) of the RBI Act, 1934. These are Chennai-based Asirvad Micro Finance, Kolkata-based Arohan Financial Services, New Delhi-based DMI Finance, and Bengaluru-based Navi Finserv.

“Unfair and usurious practices continued to be seen during the course of onsite examinations as well as from the data collected and analysed offsite,” said RBI in its statement announcing the action. The ban was implemented from 21 October.

On 8 October, RBI Governor Shaktikanta Das also cautioned NBFCs, expressing his concern over high interest rates, processing fees and penalties.

“It is important that NBFCs, including MFIs (microfinance institutions) and HFCs (housing finance companies), follow sustainable business goals, a compliance first culture, a strong risk management framework, a strict adherence to fair practices code and a sincere approach to customer grievances,” said Das, adding that the NBFC segment has registered “impressive growth” over the last few years.

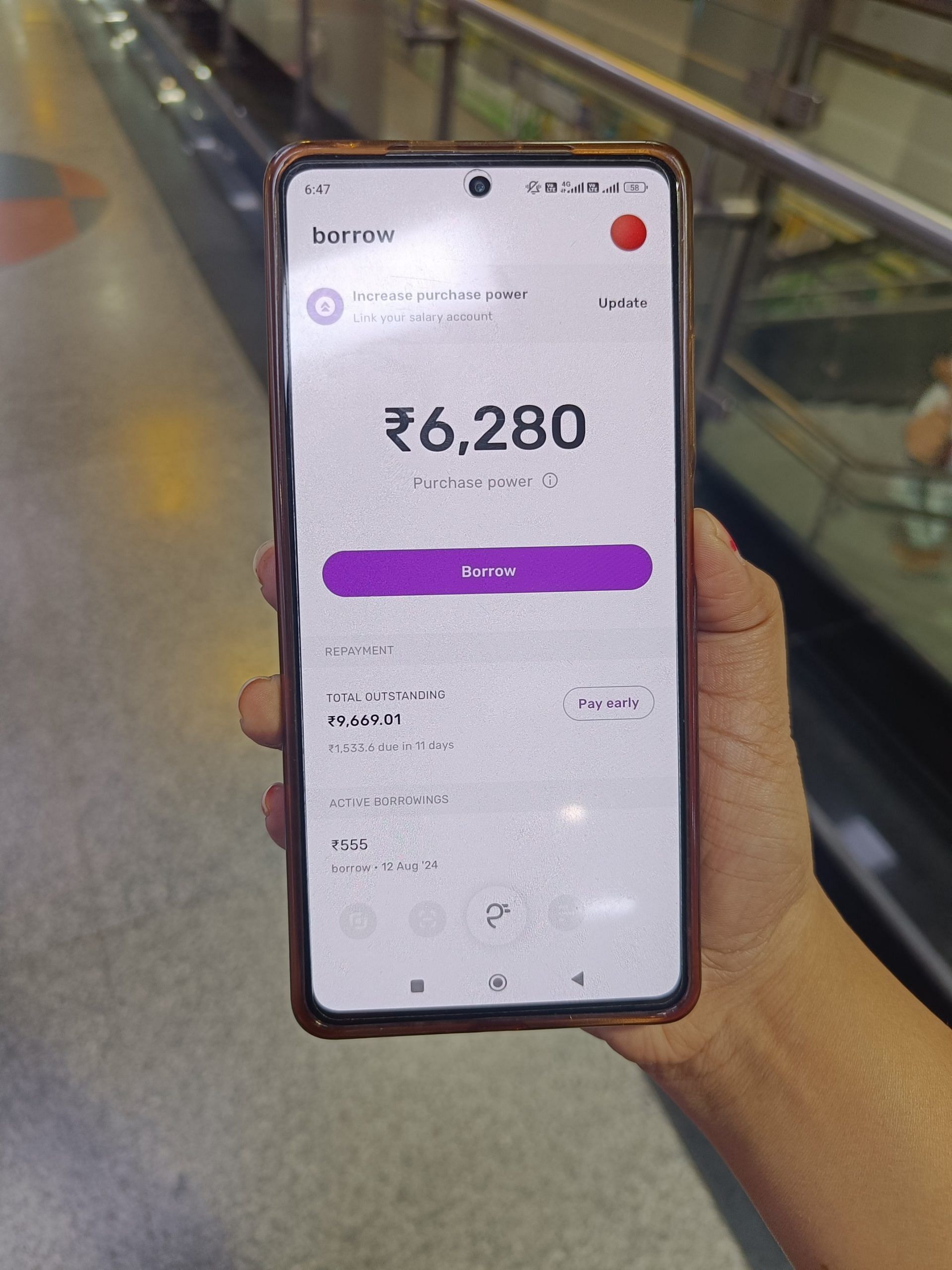

Like Utsav, there are thousands of borrowers in the country who took loans from digital lending apps registered as NBFCs to fulfil their wishes. In most cases, the capital is small, ranging from Rs 10,000 to Rs 50,000, but the interest rates can go as high as 40 percent with additional processing fees.

ThePrint has previously reported how thousands of people are troubled by threats and harassment by loan recovery agents, a problem exacerbated by the proliferation of instant loan apps that offer money at a click.

According to a study conducted across 17 Indian cities by Home Credit India Finance Private Limited, titled How India Borrows 2024, the most common types of loans taken by lower middle-class customers are consumer durable loans and personal loans, often driven by the desire to improve lifestyle.

“These aspirational customers seek material goods and entrepreneurial ventures to enhance their lifestyle and provide better opportunities for their families,” the study said. It also showed that purchasing smartphones and home appliances became the leading reason for borrowing, rising sharply from 1 percent in 2020 to 37 percent in 2024.

ThePrint spoke to several borrowers from Uttar Pradesh, Uttarakhand and Delhi, who took loans in the last six months. The common thread joining most of them was shopping for smartphones and other expensive items. Many of them were under the age of 40. Some were unemployed. In many cases, borrowers sought loans from multiple apps.

Also Read: Not just risk to banks, RBI’s curbing unsecured lending to rein in shady recovery practices too

Goa trips, birthday parties & financial distress

Manoj Kumar Singh, who hails from Bareilly in Uttar Pradesh and now lives in Delhi, has borrowed from over 15 platforms in the last three years, both banks and lending apps, like Mobikwik, True Balance and KreditBee, with loans ranging from Rs 20,000 to Rs 30,000.

He began using instant loan apps in 2021, and since then, he has paid around Rs 50,000 as interest every month, he said.

Manoj said that his household expenses are high and his salary does not cover them, so he has to take loans from different platforms. In June, he borrowed Rs 30,000 from True Balance at the interest rate of 18 percent with additional processing fee. He has to pay instalments of Rs 3,000 each as instalment for 12 months.

“The way inflation has increased, the salary has not. It has become difficult to run the house and with all this, the loans from apps continue,” he told ThePrint, adding that high interest loans are the only option. “I take a loan from one place and pay the instalment of the other, and the money that is left covers the household expenses.”

But last year, he lost his job in the transportation sector and was jobless for around six months, which made matters worse. “The recovery agents started harassing me. I used to get hundreds of calls everyday from different places and they used to abuse me,” Manoj said.

However, within a month of losing the job, he found Kunal Kumar, a Delhi-based YouTuber who helps borrowers being harassed by recovery agents by informing them of their rights. Watching the videos helped him navigate the situation better, he said.

Nitin, a resident of Uttarakhand’s Pauri district, borrowed Rs 40,000 from Navi Finserv in February at the rate of 18 percent with 3 percent additional processing fee. He is repaying Rs 48,000 in 12 instalments.

“I needed money due to domestic problems and I was not doing well work-wise. One day, I saw an ad on Instagram and I applied and got the loan in 10 minutes,” said the 35-year-old. He added that most people get trapped because they get the loan so quickly. In April, he took another loan of Rs 20,000 from KreditBee at the rate of 22 percent.

Nitin said that if banks gave small loans easily, one would not have to use private apps. “Besides taking PAN and Aadhar card, videography is also done before these apps give out loans. Using the same video, recovery agents threatened me for several days and sent altered photos to my relatives, due to which I was troubled for several days. I even had suicidal thoughts,” he told ThePrint.

In Pauri, many others are falling into the clutches of loan apps. Incidents of cyber crime are rising, too, as many fraudulent apps have entered the space. In February, the Narendra Modi-led government had informed the Parliament that Google had suspended or removed more than 2,200 fake lending apps from its Play Store between September 2022 and August 2023.

Sumit Singh, 20, took a loan of Rs 10,000 from True Balance at 32 percent interest rate to celebrate his birthday. He spent around Rs 4,000 on new clothes and the rest on the party. This was the first time he took a loan and did not inform his parents.

“I am a student at Delhi University and have no means of earning. My friends are waiting for the party,” he said, adding that many of his friends use the apps too.

Sumit’s friend Ankur Gupta, who is from Rajasthan, also took loans from three different apps.

“My parents send me 15,000 for monthly expenses. In Delhi, I spend more than that. To meet those needs, I have taken loans, and I pay instalments by saving some money,” said Gupta, who recently bought a new phone after taking a loan. He said that a number of students at the university, who hail from other parts of the country, tend to meet their expenses this way.

Muskan Kaushik, a resident of Delhi’s Shahdara area, borrowed Rs 25,000 from Slice to fund a trip to Goa in July.

“The plan to go to Goa was sudden, and my salary had not been credited then, so I took a loan, which I have to repay in nine months,” she said. She has taken several such loans previously, at rates of more than 20 percent.

Kaushik said that she used the borrowed money for tickets, clothes and hotel bookings.

“The apps come in handy in difficult times because it is difficult to get money from anywhere else so quickly, but they have risks too, if you are unable to repay the money on time,” she said.

The profusion of loan apps and NBFCs offering small loans and the growth of the overall microfinance industry has started to pose some problems to the financial system as well.

As ThePrint reported earlier this month, defaults among microfinance borrowers are rising, driven by both borrowers and lenders. Borrowers, banking analysts said, take multiple loans, spreading them across several lenders, and use one loan to pay off another. Often, the cumulative amount that’s been borrowed becomes too great to pay back, leading to defaults.

On the lenders’ side, the analysts pointed out, NBFCs are not undertaking robust checks on the creditworthiness of borrowers, driven by the impulse to lend more rather than lend responsibly.

(Edited by Mannat Chugh)

Also Read: Cousin took a loan but couldn’t pay it back? As recovery agents run amok, even you aren’t safe