The cost of a real-world oil cargo is dropping fast as buyers back away, in a dramatic reversal from last month’s bidding frenzy despite the ongoing closure of the Strait of Hormuz.

The sharp retreat provides a counterintuitive backdrop to warnings that the oil market is barreling toward a crisis point — possibly in a matter of weeks. Still, traders cautioned that the calm may be shortlived, raising the risk that physical prices soar again as the industry relies on stopgap measures that can’t fill the gap indefinitely.

An easing that began in the second half of April accelerated over the last week. Premiums of major North Sea grades, which are used to set the global benchmark Dated Brent, have plunged by as much as 90% over the past month to almost prewar levels. Several cargoes for West African and Mediterranean CPC crude for prompt delivery have even traded at small discounts to the benchmark. While prices broadly are still indicative of a tight market, they’re now within a normal range seen in recent years, before the Iran war removed more than 10% of global supply.

Some traders suggested last week that buyers have held back as the US and Iran seemed closer to a deal, wary of paying elevated prices ahead of a crash if the Strait of Hormuz reopens. Others said that oil refiners are increasingly adapting to a world where the bulk of the Middle East’s crude is locked inside the Gulf — operating on a just-in-time basis for crude supplies, drawing down inventories, reducing run rates, or getting supplies from more distant producers.

Brent futures jumped above $105 a barrel on Monday after US President Donald Trump rejected Iran’s latest response to his proposal to end the war, while a drone strike on Sunday briefly set a cargo vessel ablaze off Qatar.

The US in particular has sharply ramped up exports, while the top oil buyer China has been selling cargoes of crude into global markets in an unusual move, Bloomberg reported on April 22. Its imports have dropped sharply — adding to downward pressure on physical prices.

Read columnist Javier Blas on China’s slumping oil demand

“The physical oil market in general isn’t pricing the catastrophic tightness,” said Neil Crosby, head of research at Sparta Commodities SA. But that’s due in part to import-reliant buyers in Asia getting by on the “bare minimum” of crude supplies, he said.

Millions of barrels remain trapped in the Persian Gulf and there’s little sign of a fast resumption of tanker traffic. But a week into the new monthly trading cycle, there’s no evidence of the kind of scramble to secure cargoes seen in the opening weeks of the war, according to more than a dozen traders who spoke to Bloomberg News.

Global oil markets have been able to tap into a number of buffers to temper or delay the impact of the closure of the Strait of Hormuz: Oil markets were well supplied going into the crisis, governments have announced a record release of strategic stockpiles, Saudi Arabia and the United Arab Emirates are exporting crude via pipelines and also sailing some tankers through the strait, while other exporters like the US and Brazil have sharply ramped up shipments.

At the same time, global oil consumption has dropped sharply — in part because of forced reductions due to fuel supply shortages in parts of Asia or Middle Eastern petrochemical plant closures, and in part as a result of surging prices.

Eyewatering Premiums

While prices remain at elevated levels, the eyewatering premiums that traders were bidding for immediately-available barrels have largely disappeared. A cargo of West Texas Intermediate Midland sold at a premium of just $1.50 a barrel Friday in the Platts pricing window that helps set the North Sea benchmark, down from $22 in April.

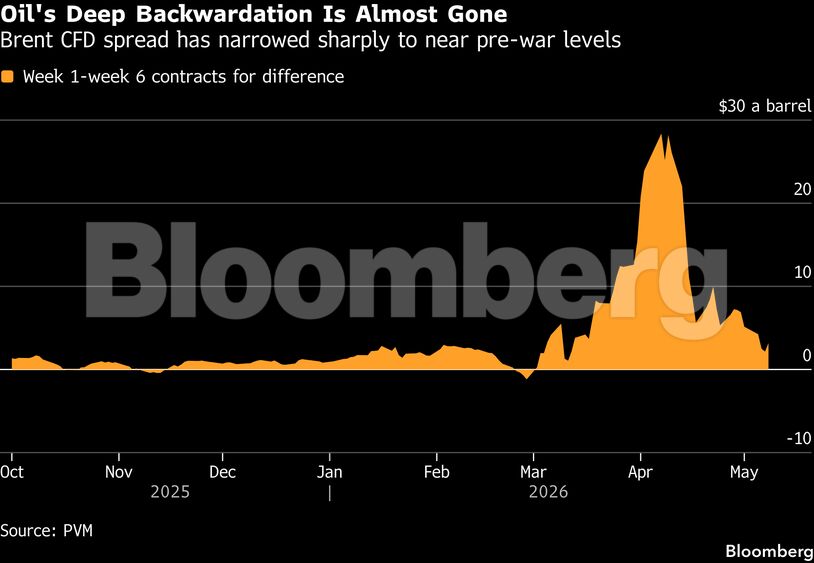

The steep backwardation, in which more-immediate derivatives fetch premiums over later-month ones due to a tight market, has also narrowed sharply. The six-week spread in Brent contracts for difference — derivatives that allow traders to hedge physical cargo prices — shrank to $2.15 on Thursday, compared with about $28 a month ago.

Oman crude, one of the few Middle Eastern grades still fully accessible to the global market because cargoes don’t have to traverse the Strait of Hormuz, sold late last month for a premium of about $15 a barrel to the Dubai benchmark, said traders who spoke on condition of anonymity. The premium was pegged at over $7 a barrel on Friday. Equivalent cargoes traded around $60 above the same marker earlier in the war.

With exports from the Persian Gulf still severely disrupted, this decline is the result of a behavior change among refiners, primarily in Asia.

They have found some replacements for Middle Eastern supplies, for example from the US and Latin America. The bigger driver has been a reduction in their purchases of oil — they are processing less crude into fuel and drawing down their inventories instead of seeking fresh supplies. And any procurement being done is for dates far more prompt than normal.

For the Dubai crude market, trading has shifted to dates so prompt that typical benchmark-setting mechanisms for supplies two months ahead have become devoid of activity — adding to the appearance of depressed prices even as the market is still dealing with unprecedented scarcity.

While the lower premiums for physical crudes are welcome news for refiners, their actions will prove to be a temporary fix if Hormuz doesn’t reopen soon. The cyclical nature of the refining industry means upward pressure on premiums could return in the coming months.

Europe’s spring maintenance season is due to wrap up soon, potentially reviving demand for June cargoes, according to the traders, who asked not to be named as they’re not authorized to speak publicly. In Asia, crude-processing rates in Japan and South Korea are slowly climbing after falling early in the war, according to Crosby.

Eventually, inventories will dwindle and if refiners want to keep fuel flowing to customers they will need to acquire more crude in a market that’s lost a billion barrels of supply.

“The question is how long this lasts and how much of a problem do we build?” Shell Chief Executive Officer Wael Sawan said on a conference call on Thursday. “We’ve drilled a hole, a billion barrels worth of a hole, and we’re going deeper and deeper.”

This report is auto-generated from Bloomberg news service. ThePrint holds no responsibility for its content.