The V-shaped economic recovery that India’s policy makers obsessed over in 2020 did eventually materialize. It won’t be repeated after this year’s Covid-19 carnage.

To see why, start with the fading momentum. Government statistics released Monday showed 1.6% growth in gross domestic product from a year earlier in the March quarter, before a deadly second wave of infections. But this expansion, an improvement over the 0.5% rate in the previous three months, is a statistical artifact. A better metric is seasonally adjusted quarter-on-quarter growth, which Capital Economics calculates at 0.7%, a sharp — though largely expected — slowdown from 9.5% in the December quarter. (The figures aren’t annualized.)

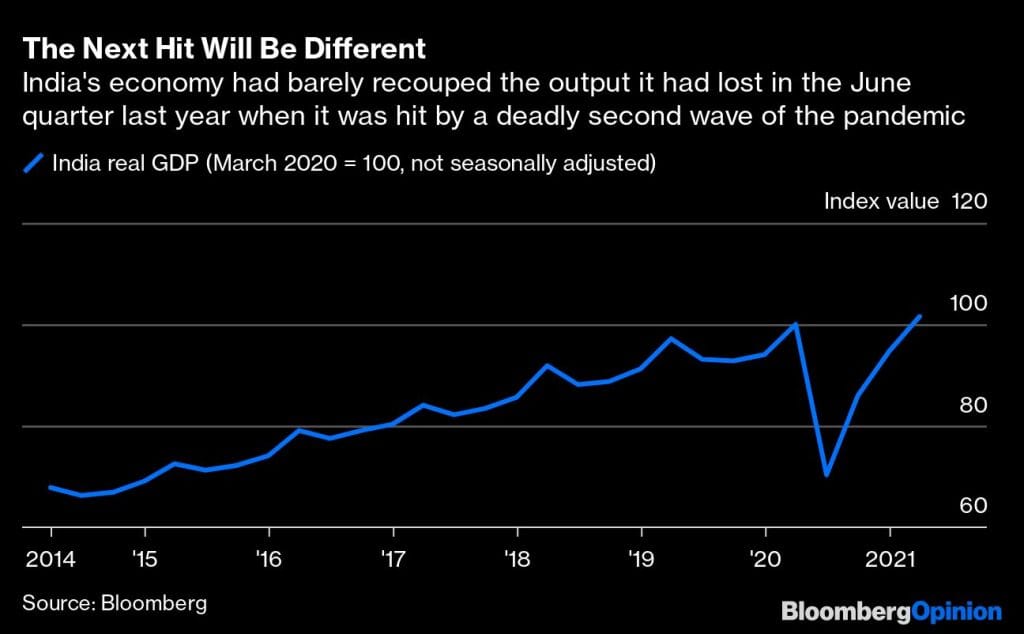

With production losing steam, overall output still caught up with its level the previous year, when India was just entering a stringent national lockdown. That disruption caused a brutal 24.4% loss of GDP in the June quarter that took the economy nine months to recoup. That’s not a perfect V-shape, but close enough.

Don’t expect the same this time. During the current surge in cases, there have been only local restrictions on physical activity. That’s making some analysts optimistic about the resumption of growth that will inevitably occur when the coronavirus fully recedes. Yet there are several crucial difference from last year that could make it harder for India to bounce back.

Take the intensity of the pandemic. Officially, India recorded about 14 million new cases and 116,000 deaths between February 1 and May 15. But according to a study by University of Michigan and other researchers, a more reasonable estimate may be 380 million infections. (Imagine the entire U.S. population — and about half of Mexico — catching Covid-19 in 3 1/2 months.) The real fatality count, according to the same paper, is closer to 700,000, and climbing.

The staggering scale of the tragedy suggests that medical expenses, which in India mostly come out of patients’ pockets, will have depleted household savings. With high fuel taxes crimping family budgets, it’s reasonable to expect consumers to spend cautiously even when they can go out freely. The slow pace of vaccination — a little more than 3% of the population is fully inoculated — will make people wary of a third wave.

Unlike last year, the disease has spread. Infections in metropolitan centers are receding, but they’re still stubbornly high in outlying districts. Alongside fading growth momentum and private health expenditure crowding out discretionary spending, pressured rural wages will be the other reason to rule out a quick revival. As Sunil Kumar Sinha, principal economist at India Ratings and Research Ltd., a unit of Fitch Ratings Ltd., explains, carpenters, blacksmiths and vehicle repairmen, as well as construction, transport and storage workers in villages, require high levels of physical contact. Many poor families may not even have healthy adults to take advantage of a 15-year-old program of guaranteed community work, where the government pays the wages. Despite record agricultural production, rural demand could remain muted.

Finally, India’s current strategy for demand revival is flawed. There’s no sign of a meaningful income-support program to put purchasing power in the hands of battered households dealing with double-digit unemployment even without a national shutdown. Meanwhile, savers are being forced to accept deposit interest rates that are barely covering half of their inflation expectations.

In other words, India is witnessing a huge shift in resources away from the ultimate providers of labor and capital, and toward borrowers: companies and the government. The central bank recently handed over a $14 billion dividend check, much larger than expected, to the Finance Ministry. The money will come into the banking system as the state spends it and further squeeze retirees’ interest income when their children are struggling in the job market and commodity inflation is accelerating globally.

Retail investors piling into equities even when the real economy struggles is not prosperity, but an optical illusion. As finance professor Ananth Narayan, a former Standard Chartered Plc banker, notes, large negative real rates heighten “risks of asset price and general inflation, widening inequities, and eventual external imbalances.”

With growth firming up in the rest of Asia, several countries will slowly start raising interest rates before the Federal Reserve. To preserve financial stability, India needs to think about joining them. Not chase dreams of yet another V-shaped recovery.- Bloomberg

Also read: Second Covid wave’s economic impact won’t be large, CEA KV Subramanian says