The way the cost of financial misconduct has been rising globally, a $158 million fine may seem like loose change.

However, the Securities & Exchange Board of India has delivered much more than a slap of the wrist with its disgorgement order against the National Stock Exchange of India Ltd. over an algorithmic trading scandal.

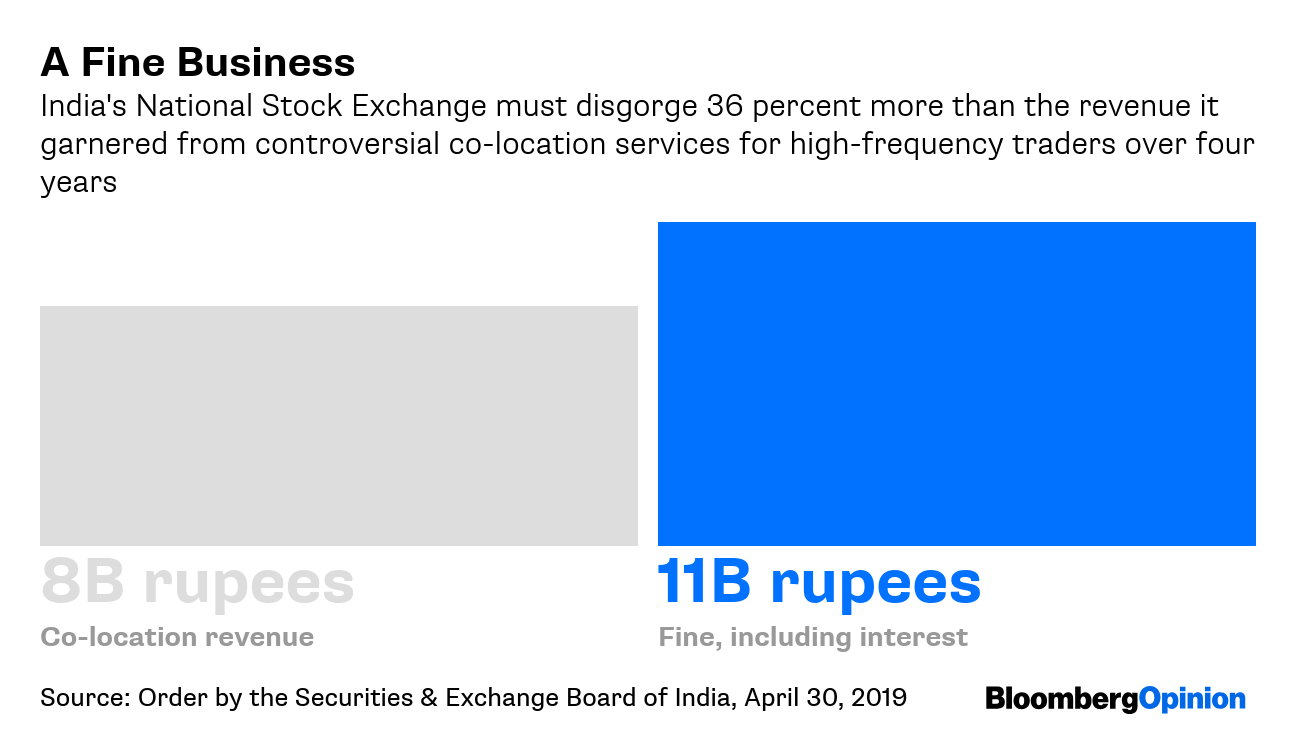

Including five years of interest at 12 percent, the 6.25 billion rupee penalty works out to 11 billion rupees, or about $158 million. That’s a fraction of the $110 billion bill Bank of America Corp. and JPMorgan Chase & Co. have run up between them in fines and settlements since 2008, according to a tally maintained by Bloomberg Intelligence.

Yet that figure is only 5 percent of the revenue that the banks have garnered in the past 11 years. By contrast, what Sebi is asking the NSE to pay is more than a quarter of its combined overall operating revenue for four years, after the regulator ruled that a high-frequency trading firm benefited from unfair market access. It’s also more than whatever money the exchange made from HFT until changing its system in 2014.

This is overkill, especially since the regulator couldn’t establish the graver charges of fraud or unfair trade practice. It all boiled down to whether the technology used by the NSE to roll out its high-frequency business provided an equal and fair trading environment to everyone who had opted to place their computers close to the exchange’s, hoping to pare microseconds when executing trades.

When I wrote about the scandal two years ago, the contents of a forensic study by Deloitte Touche Tohmatsu had just leaked. It pointed out that until 2014, when the NSE shifted to broadcasting price information simultaneously to all traders, it was giving those first to log in an advantage without randomizing the benefit. Additionally, there was a lightly used backup server, which OPG Securities Pvt. was consistently connecting to before anyone else between December 2012 and April 2014.

Also read: SEBI moves to curb excessive speculation by regulating derivatives

Further analysis failed to unearth a scam of any size, however. In a separate order, Sebi slapped a fine of roughly $2 million plus interest on OPG, assessing that to be the unlawful profit from unreasonable use of the backup server. As for NSE’s failure to ensure an equal and fair trading environment, Sebi has also asked two of the exchange’s previous CEOs – Ravi Narain and Chitra Ramkrishna – to give up a part of the pay they earned in the top job between 2010 and 2014. They won’t be able to work for a market intermediary, a stock exchange or a listed company for five years.

Current CEO Vikram Limaye should be reasonably happy, though. The fact that the the NSE wasn’t found guilty of intentionally running a rigged high-frequency market lifts the cloud hanging over its credibility. The order paves the way for the exchange’s long-delayed IPO after a six-month moratorium during which it won’t be allowed to access the securities markets.

Besides, the penalty – harsh as it is – won’t have any cash-flow implications. Even as it was taking its time investigating, the regulator had asked the NSE to set aside its co-location revenue. By March 2018, the escrow account had already swelled to about 12 billion rupees. After paying the fine, Limaye will have more cash at his disposal. But since the exchange hasn’t made any provisions for the fine, it will have to take a charge, perhaps as early as the June quarter.

Internal processes have already become more robust, but the bigger impact of Sebi’s order may be on NSE’s culture. The company achieved dominance in a short time, leaving its much older rival, the Bombay Stock Exchange, in the dust. The hubris that engendered needs to be tempered with some humility.

Investors like Goldman Sachs Group Inc. and Singapore’s Temasek Holdings Pte would have been able to exit a lot sooner had the previous management of NSE not been so contemptuous of the idea of listing its shares on the BSE. Or if they had addressed a whistle-blower’s complaint against its algorithmic trading system rather than slapping a defamation suit against Moneylife India, the website that reported the allegations of unfair access, in 2015.

That one mistake may have cost the exchange four years, and $158 million.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.