How have the Modi government’s budgets fared in the last 10 years? One way to answer that question would be to compare them with those of the previous governments. But another way would be to evaluate the Modi budgets inter se. The latter exercise could be more useful in the current context. Since not much has changed in the Modi government after the last general elections (even the top budget team in the finance ministry has remained the same!), it would be instructive to assess how the budgets of the last 10 years looked at basic fiscal governance issues and how these could be an important pointer to the kind of Budget that Finance Minister Nirmala Sitharaman is likely to present on July 23.

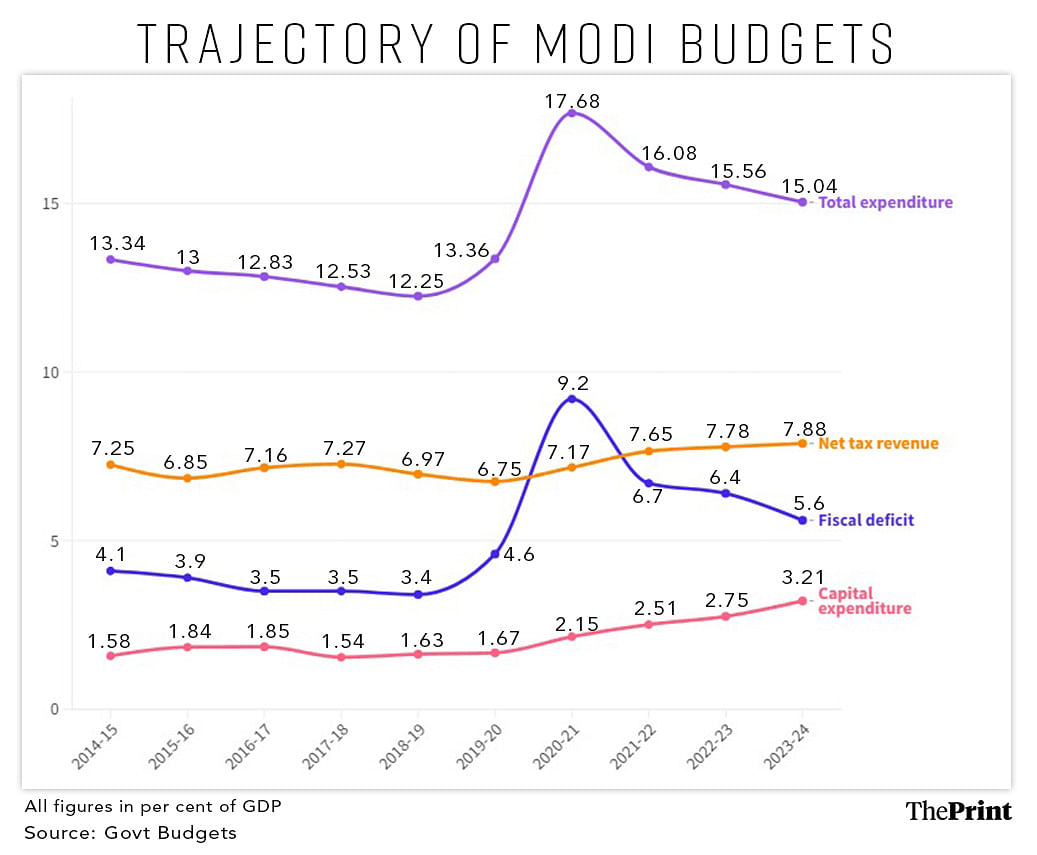

Let us begin with the size of the government. The total expenditure of the Union government in 2014-15 was as large as 13.34 per cent of gross domestic product or GDP. Over the next four years, this was brought down to 12.25 per cent of GDP by 2018-19. Notably, this reduction was achieved through a welcome squeeze on revenue expenditure, while capital expenditure remained broadly unchanged during these five years at between 1.5 per cent and 1.8 per cent of GDP.

The pre-Covid year of 2019-20 and the Covid year of 2020-21 saw an understandable spike in government expenditure to 13.4 per cent and 17.7 per cent of GDP, respectively, fuelled largely by a rise in revenue expenditure and a small increase in capital expenditure. But what ignited hope was the government’s decision in the following three years to steadily reduce its total expenditure to 15 per cent of GDP by 2023-24.

This decline had two reassuring features. The government’s capital expenditure rose sharply from 2.1 per cent of GDP in 2020-21 to 3.2 per cent of GDP in 2023-24, helping to revive growth at a time when the beleaguered private sector was in no position to increase investment. Simultaneously, its revenue expenditure declined from 15.5 per cent to 11.8 per cent in the same period. This was a commendable achievement. Not only did the government’s total expenditure come down, but even its quality improved.

The key question that Ms Sitharaman has to wrestle with while formulating the Budget for 2024-25 is whether she can further reduce government expenditure. Ideally, she should go in for a sharper cut in revenue expenditure, which will allow her to further boost capital expenditure. Her interim Budget for 2024-25 had proposed a capex increase to 3.4 per cent of GDP, with revenue expenditure sliding to 11.1 per cent of GDP. Even if capex has to go up to 3.5 per cent of GDP (a rise of over 20 per cent over what was spent in 2023-24), then the revenue expenditure has to take a bigger hit, perhaps down to 11 per cent of GDP.

But there will be major challenges. Such rationalisation would mean sizeable cuts in various welfare programmes of the government, including its subsidy schemes. Last year, Sitharaman managed to slash the total subsidies bill sharply to 1.5 per cent of GDP, against 2.14 per cent in 2022-23. The scope for a further cut in subsidies in 2024-25 is extremely limited.

There are already demands on the finance minister to increase the allocations for PM Kisan and Mahatma Gandhi National Rural Employment Guarantee Scheme (MGNREGS). Coalition politics is bound to extract a higher price in terms of increased allocation to a couple of states whose ruling parties are supporting the Modi government at the Centre. Even after taking into account the extra surplus transfer from the Reserve Bank of India (RBI), amounting to almost 0.4 per cent of GDP, containing expenditure growth will be a formidable task.

Note that the government’s fiscal deficit for 2023-24 is already down to 5.6 per cent of GDP. If Ms Sitharaman retains her interim Budget target of 5.1 per cent for 2024-25, the extent of fiscal consolidation at half a percentage point of GDP would be lower than what was achieved last year. This will also mean that she has to effect a sharper cut in deficit by 0.6 percentage point to reach the 2025-26 target of 4.5 per cent. This year, she has the benefit of the RBI surplus transfer bonanza, which may not be available to her in 2025-26. Clearly, it will make more sense to implement a sharper cut in fiscal deficit to 5 per cent or 4.9 per cent of GDP this year, to make her task in 2025-26 less onerous.

But with higher expenditure demands on the exchequer on account of welfare schemes, what is the way out for the finance minister? She has no option other than relying on improving revenues. Net tax revenues for the Centre have been rising slowly after the Covid impact — from 7.2 per cent of GDP in 2020-21 to 7.88 per cent in 2023-24. In addition, the composition of tax collections has become less regressive, with the share of direct taxes surpassing that of indirect taxes since 2021-22. The worrying signs are that non-tax revenues continue to languish below 1.5 per cent of GDP for the last four years, and the share of disinvestment receipts has not only been declining over the last two years, but there are also question marks over whether serious disinvestment attempts would be made this year or the next.

Yet, it seems Sitharaman’s first Budget in the third term of the Modi government will have to rely more on raising higher revenues. If there is increasing pressure to raise allocations for welfare schemes, making a further squeeze on revenue expenditure difficult, if the pace of fiscal consolidation needs to be slightly sharper, and if no compromise is made on the much-needed rise in capital expenditure, the finance minister will have to focus more on steps towards raising more tax as well as non-tax revenues and outline a more ambitious disinvestment plan. How these goals are achieved, of course, will be known in just about two weeks from now.

AK Bhattacharya @AshokAkaybee is the Editorial Director, Business Standard. Views are personal.