It is clear by now that Indian wheat production in 2021-22 Rabi season is going to be lower than the government’s second advance estimate of 16 February 2022, of 111.32 million metric tonnes (MMTs). The moot question is by how much? Also, if the production is lower, then what is the amount of wheat that the country can afford to export to meet the global wheat demand? We address these questions.

Level of wheat production in India

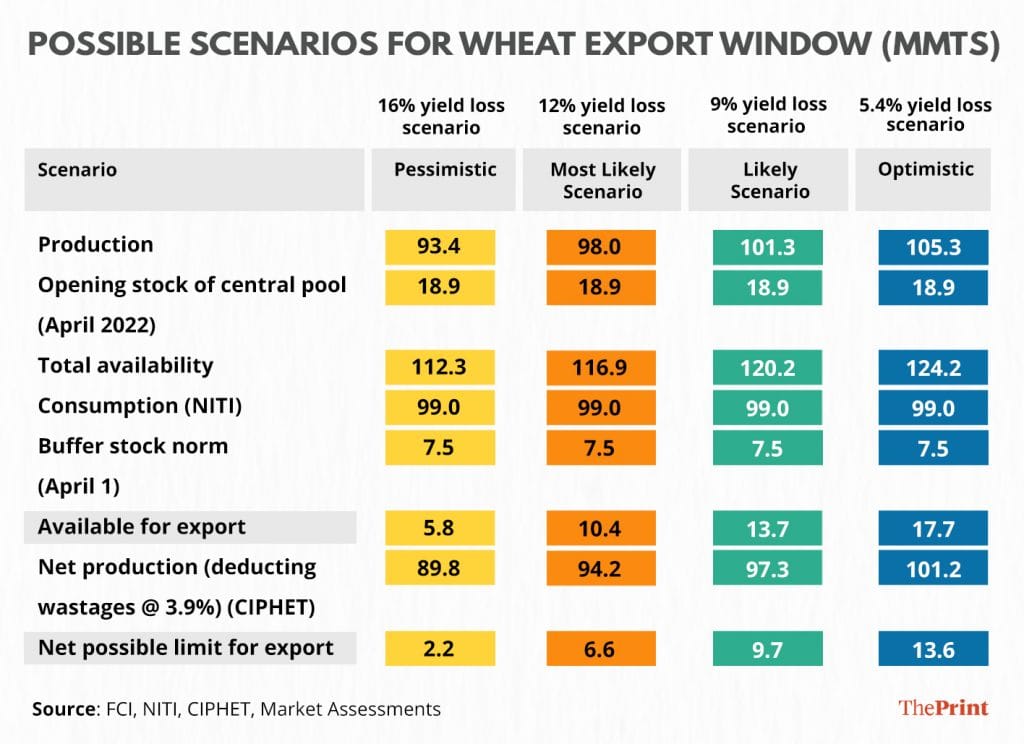

The country was expected to produce about 111.32 MMTs of wheat in 2021-22 (marketed in the Rabi marketing season 2022-23). Last year’s production was about 109.6 MMTs. As per NITI Aayog’s Prof Ramesh Chand, India’s wheat production is most likely to lie between 101.3 and 105.3 MMTs. The trade, however, pegs the current crop at a much lower end at around 93.4 MMTs – about 16 per cent lower than the second advance estimate.

Lower production and possibility of higher value realisations globally or domestically have impacted the central government’s procurement drive. As of 30 April 2022, about 16 MMTs of wheat have been procured. This is about 41 per cent lower than the 27 MMTs wheat procured last year till this time. It is feared that procurement may reach just about 20 MMTs, which is about 5 MMTs lower than the worst-case scenario projected in our previous article. Among other things, lower procurement is likely to impact the government’s ability to sell under the Open Market Sale Scheme (OMSS). This sale usually plays a critical role in scenarios of high inflation because these sales help in diffusing the building price pressures.

Also read: India’s sweet spot in hoarding wheat looks shaky. Ukraine war means new concerns for Modi govt

How does India’s wheat balance sheet look in 2022-23?

Let us start with the supply side (Table 1). As we know, the crop this year is estimated to be anywhere between 93.4 MMTs and 105.3 MMTs. We started the crop year (1 April 2022) with about 18.9 MMTs of central pool wheat stocks (there are bound to be some private stocks too, but they do not usually enter the balance sheets due to the paucity of credible data). This makes total availability about 112.3 MMTs to 124.2 MMTs.

On the demand side, as per NITI Aayog’s demand-supply projections for 2021-22, India needs about 99 MMTs of wheat annually to meet its domestic demand. In addition, the country needs about 7.5 MMTs of wheat to meet its minimum buffer and strategic norm requirement for 1 April. After keeping aside enough to meet these two needs, it appears that the amount of wheat the country has available in excess of domestic demand will range between 5.8 MMTs to 17.7 MMTs. If one accounted for wastages along the wheat value-chain (we take the CIPHET estimate of 3.9 per cent), the number would be lower (Table 1).

Table 1

Overall, from the above estimates, a plausible window for wheat export appears to be limited to about 10 MMTs. This, of course, increases with higher production.

Also read: Why India shouldn’t get carried away by wheat, rice export bonanza due to Ukraine war

Global situation and India’s window to export

As per USDA, about 772 MMTs of wheat were produced and about 199 MMTs were exported in triennium ending (TE) 2021-22 globally. India’s share was about 14 per cent and about 2 per cent respectively. Usually, Indian wheat is not competitive globally on account of higher prices. However, rising global wheat prices have made Indian wheat competitive and so its exports have been growing. India’s share in global wheat exports was 4.2 per cent in 2021-22. In TE 2021-22, Russia’s share in global wheat exports was about 18 per cent and Ukraine’s about 10 per cent in 2021-22.

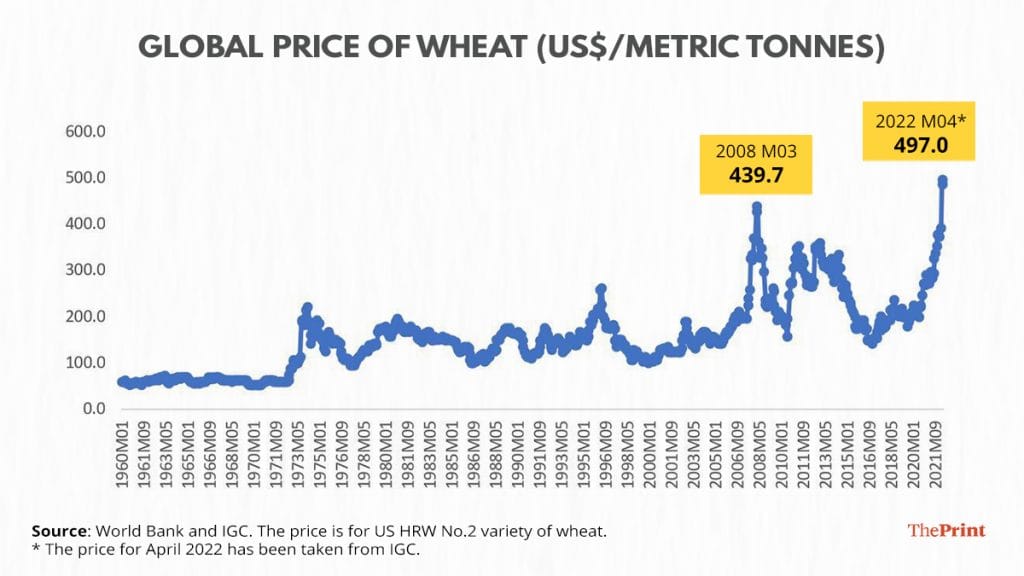

In the last year, global prices of wheat (US hard red winter No. 2 variety) have risen by 78 per cent: from $273/MT in March 2021 to about $486/MT in March 2022. Since January 2022, they have risen by about 33 per cent till April 2022 (Figure 1). In the 62 years of historical data series from the World Bank, such a level of price has never been reached, not even during the 2008 food crisis (Figure 1).

Figure 1

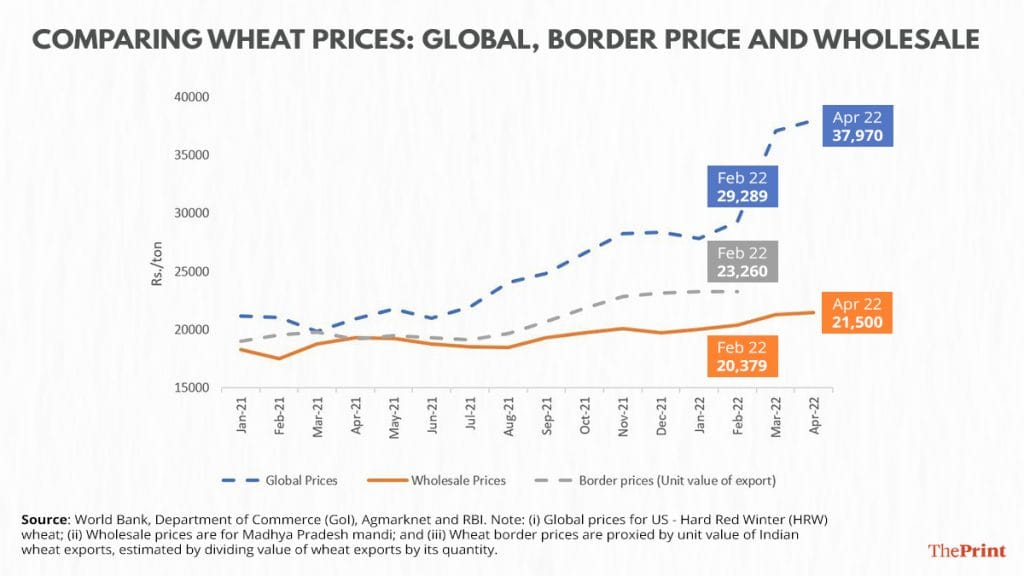

As per Figure 2, Indian wheat (unit value of exports) has been selling cheaper than global wheat prices. In rupee terms, in February 2022, while global wheat was selling at about Rs 29 per kg, Indian wheat exports were going at an average rate of about Rs 23 per kg and the price in MP’s wholesale mandi was about Rs 20 per kg. Clearly, there is an attractive window of opportunity for the export of Indian wheat today.

Figure 2: Comparing wheat prices: Global, Border Price and Wholesale

The government knows about the emerging situation of lower procurement and the possibility of higher inflation in cereals.

Since last month, the Ministry of Railways has taken three key decisions affecting the logistical cost of transporting wheat to ports: (i) it has withdrawn the Traditional Empty Flow Direction (TEFD) benefit on wheat booked for port destinations; and (ii) it has increased the wagon registration fee for wheat booked to port destinations by 10 times, from Rs 50,000 to Rs 5 lakh per rake. In addition to this, from 1 May, the booking of wheat rakes to ports for exports has also been reduced—from earlier 15-16 rakes per day on average to 9 rakes now. From wheat surplus regions, only one rake per day is permitted now.

The war between Ukraine and Russia entered its 68th day on 3 May. The multiplier impacts of the war and the ensuing sanctions on the world are still unfolding. But what is clear is that many countries, especially in western Africa and even Middle East, may be looking at among the worst food crisis in decades. India can and should help provide food security to the world. Besides, it is a good time for Indian wheat exporters and farmers to earn from high global prices. But, a caution in monitoring the situation is warranted.

The Narendra Modi government, while closely tracking the evolving situation of wheat production and arrivals, must track, inter alia, rake movements to ports and ships booked for exports and the contracts signed by the private trade for exports in future. Back in 2004-05, lack of information on private trade contracts resulted in much larger quantities of wheat exports than intended by the government, resulting in depletion of central pool stock to 2 MMTs (that was half of the buffer stock norm of 4 MMTs on 1 April 2006). This had to be followed up by imports in the following years.

A repeat of that needs to be averted.

All three authors are with Arcus Policy Research. Views are personal.