")

Japan should technically be in trouble if every conventional economic rule is taken into account. The nation is experiencing growth of less than 1 per cent, a declining population, an ageing workforce, and a public debt level that ranks among the highest globally. In textbook macroeconomic theory, such a combination typically signals stagnation, inflationary pressures, or worse.

However, Japan today presents an economy characterised by near-full employment, increasing wages, and a stable domestic demand—a scenario that not only defies expectations but also subtly questions the foundational assumptions of these expectations.

The most compelling evidence of this challenge to conventional rules is found in Japan’s labour market, where the divergence between theory and reality is most pronounced at this point. The International Monetary Fund (IMF), in its latest Article IV consultation, observes that labour shortages have reached their highest level since the early 1990s, with firms across various sectors struggling to recruit workers.

Unemployment remains close to 2.5 per cent, while wage growth has attained multi-decade highs. Within any standard analytical framework, such a labour market would typically be expected to lead to overheating, rendering Japan an intriguing subject for economic analysis.

A labour market that refuses to overheat

If a labour market is characterised by such tight conditions, one would anticipate inflationary pressures to emerge, suggesting that Japan should be experiencing persistent economic overheating. This expectation is grounded in the Phillips Curve, which explains that low unemployment rates lead to increased wages, subsequently driving inflation upward.

However, Japan’s current situation complicates this relationship. Although wages are rising, labour is scarce, and domestic demand is strong, inflation remains moderate and is projected to stabilise around the Bank of Japan’s 2 per cent target.

If the Phillips Curve does not behave as anticipated, the relationship between employment and inflation may not be as mechanistic as traditional economic models suggest. Japan’s economic structure helps explain why: productivity improvements, cautious consumption behaviour, and institutional credibility mitigate the transmission from wage increases to price inflation.

The broader implication is significant, even in a scenario closely resembling a textbook case of labour scarcity, economies may not respond in a linear manner. Should one of macroeconomics’ most enduring relationships begin to weaken, the framework used to interpret economic stability must adapt accordingly.

Also read: RBI is going out of its way to compensate fraud victims. It doesn’t have the mandate

Policy normalisation without instability

Should inflation remain controlled despite tight labour markets, the next challenge pertains to policy, where Japan is subtly redefining expectations. Following decades of highly accommodative monetary policy, the IMF now recommends a gradual increase in interest rates, reflecting confidence in domestic demand and wage growth. This transition is already in progress, with monetary accommodation being withdrawn in a measured manner.

While rate hikes typically pose a risk of destabilising fragile economies, Japan’s experience suggests a different outcome. Economic growth has been sustained, domestic demand remains robust, and policy normalisation is occurring not as a reaction to crisis, but as part of a deliberate transition. This stability has persisted despite global disruptions, including fluctuations in energy prices driven by geopolitical tensions in the Middle East.

This serves as a reminder that Japan’s resilience is not a result of isolation but rather of its structural robustness. At the same time, fiscal policy is shifting towards targeted support and long-term sustainability. If an economy characterised by high debt and low growth can tighten policy without disruption, the presumed correlation between vulnerability and these indicators becomes considerably less certain.

Also read: India’s MSMEs are stuck in a crisis-rescue cycle. They need steady liquidity flows

Slow growth, strong outcomes

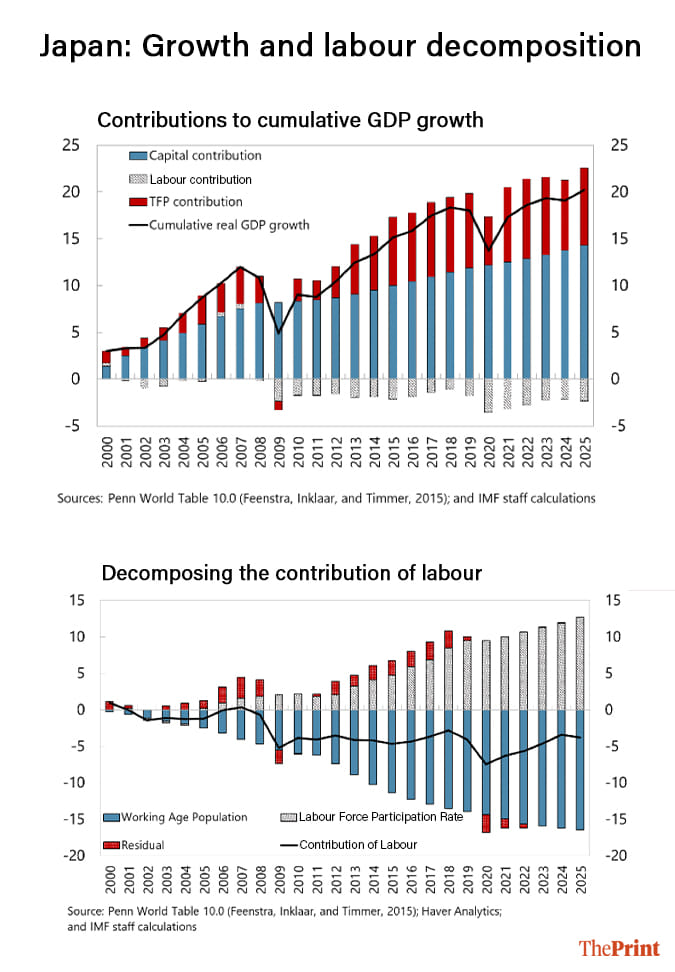

If policy normalisation can occur without inducing instability, then economic growth itself becomes a less reliable indicator of economic health. Japan’s economy, projected to expand at approximately 0.8 per cent, operates above its potential, supported by strong domestic demand and increasing wages. Its approach to demographic decline, through enhanced female workforce participation, extended working lives, and automation, demonstrates adaptation rather than decline.

If a reduction in the workforce does not result in economic contraction, then efficiency and institutional robustness must be compensating for the lack of scale. Japan’s current account surplus remains strong, primarily driven by income from its extensive overseas assets, estimated at approximately $3.7 trillion. If an economy can maintain prosperity with a smaller population and slower growth, the notion that expansion is the primary measure of success begins to look increasingly inadequate.

In the context where economic growth is no longer the sole indicator of success, Japan provides an insightful perspective on potential future trajectories. Economies such as India are currently experiencing an expansionary phase, driven by demographic factors and increasing consumption. However, this phase is not indefinite. Over time, as populations age and productivity becomes the primary driver of output, growth naturally slows, shifting the focus from acceleration to stability.

If this transition is indeed inevitable, Japan’s experience should be viewed not as an anomaly but as a precursor. It illustrates that an economy can maintain resilience even as growth moderates, provided that its labour markets, institutions, and policies are appropriately adapted. If the future of many economies aligns with this trajectory, the pertinent question becomes not how long growth can be sustained, but how effectively economies prepare for the subsequent phase.

Despite perceptions that Japan is underperforming, characterised by slow growth, rapid ageing, and high debt, it continues to exhibit stability and resilience. This suggests that the issue may not lie with Japan itself, but with the assumptions used to evaluate it.

The weakening of traditional economic relationships, such as the Phillips Curve, alongside the capacity to normalise policy without crisis, indicates that economic success is more complex than conventional metrics suggest. Recognising this complexity positions Japan not as an exception requiring explanation, but as a model asking to be understood.

Bidisha Bhattacharya is Consulting Editor (Economy) at ThePrint. She tweets @Bidishabh. Views are personal.

(Edited by Saptak Datta)