")

India has recently achieved a significant milestone by reaching a 20 per cent ethanol blending target, a year ahead of schedule. This accomplishment represents a deliberate policy success, as the blending production capacity increased 18-fold over a decade, reducing crude oil imports and providing farmers with an additional revenue source.

However, this achievement is accompanied by certain implications, particularly concerning grain. The same agricultural cycle that now contributes to nearly one-fifth of India’s petrol supply has also experienced significant volatility in food prices, with an 11.5 per cent inflation spike followed by deflation within 28 months. With the potential return of El Niño in 2026, it is pertinent to consider whether India’s progress in energy security has inadvertently compromised its food security, especially at a time when such security is crucial.

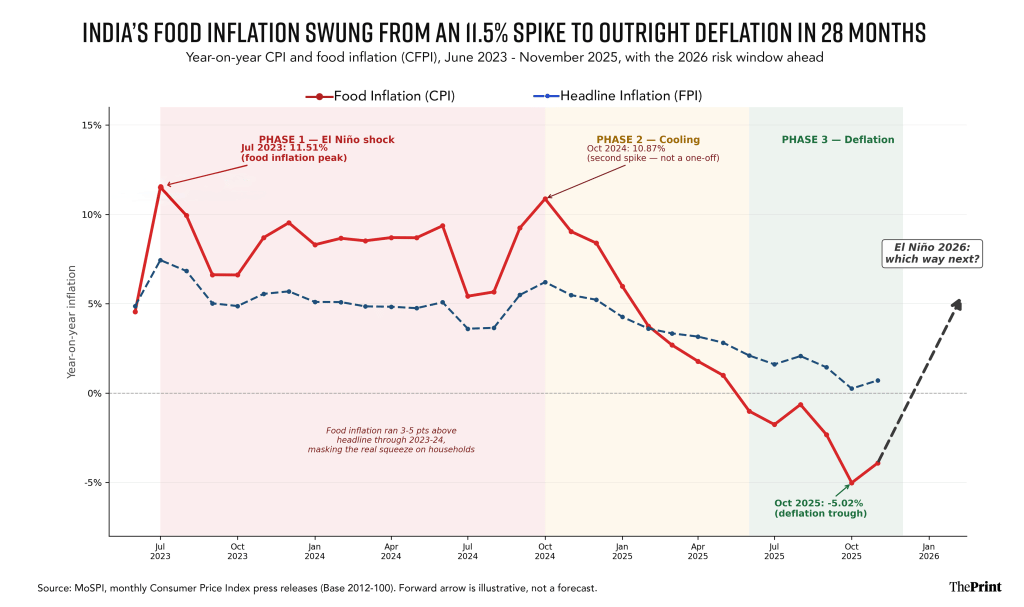

28 months, 3 personalities

Food inflation in India has exhibited characteristics akin to three distinct economic phases. The first phase was marked by the 2023 El Niño shock, during which food inflation surged beyond 11 per cent in July, consistently exceeding the headline Consumer Price Index (CPI) by 3-5 percentage points throughout the year. The second phase appeared to offer relief until October 2024, when a second spike to 10.87 per cent occurred, indicating that this was not an isolated incident but rather a recurring, climate-related pattern within India’s food economy.

The third presents an intriguing scenario: by October 2025, food inflation had decreased to -5.02 per cent, a deflationary trough that, while seemingly positive, typically indicates an overcorrected supply response. This response is characterised by farmers and traders hastily offloading stock following two years of price volatility, rather than signifying enduring stability.

The chart’s projection into 2026 candidly reflects the prevailing uncertainty: with El Niño conditions re-emerging, it is challenging to predict the future trajectory. A system that has fluctuated from +11.5 per cent to -5% within less than two and a half years lacks substantial spare capacity. It remains vulnerable, being one favourable monsoon away from a recurrence of the 2023 scenario. Notably, as the next chart illustrates, the supply buffer that mitigated the initial shock has itself undergone transformation.

Also read: Bengal budget formally ends state’s long fight with Centre. Betting big on double-engine

The ethanol story is a food-security story too

India’s achievements in clean fuel and its fluctuations in food inflation are interconnected phenomena, which can be understood through the economic principle of derived demand.

Maize and rice aren’t just food crops any longer; they are also inputs into two distinct downstream markets: food consumption and fuel production. Economists categorise this situation as joint inputs fulfilling competing derived demands. The demand for ethanol manifests in the grain market not as a direct demand for ethanol, but as a demand for maize, indistinguishable from the demand originating from flour mills or poultry farms. These two markets are interconnected through a common input, such that a disruption in one, such as a blending mandate requiring additional feedstock, can inadvertently constrain supply in the other market.

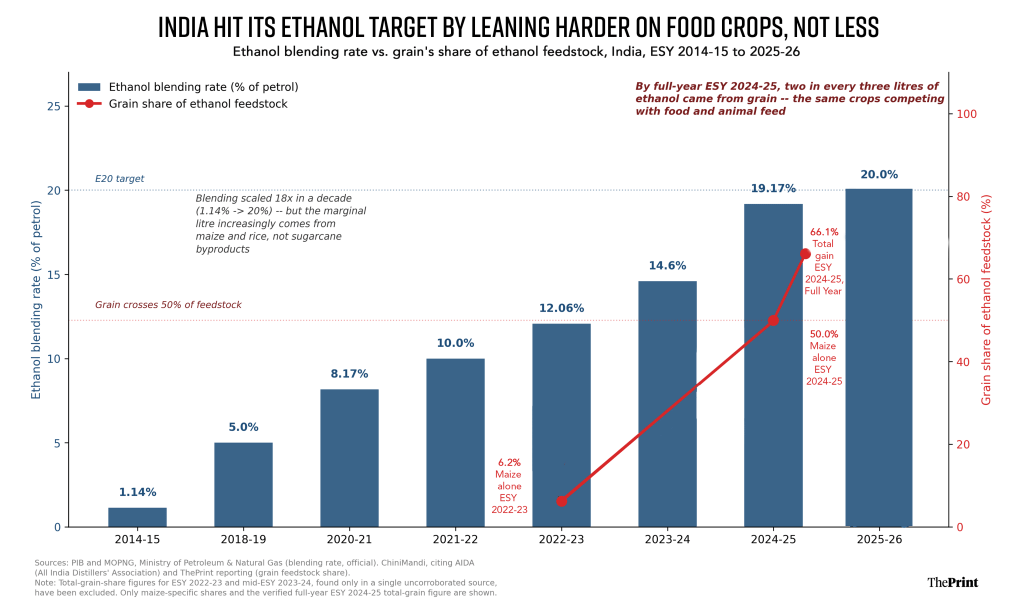

The data indicate a real-time tightening of this wiring. In the Ethanol Supply Year (ESY) 2022-23, maize constituted merely 6.2 per cent of ethanol feedstock. By the complete ESY 2024-25, maize alone had increased to nearly 50 per cent, while the total grain-based feedstock, comprising maize and rice, accounted for 69 per cent of the supply, up from 59 per cent the previous year. Nearly seven out of every 10 litres of ethanol blended into India’s petrol last year originated from crops that also supply the country’s kitchens and its poultry feed.

This development is a natural and almost inevitable outcome of rapidly scaling blending: sugarcane molasses alone could not have supported a programme expanding at this pace, necessitating the use of grain to bridge the gap, as a well-functioning input market should. The average blending for the entire year reached 19.24 per cent, just shy of the 20 per cent target it surpassed months later.

The derived-demand link explains the significance of this situation for inflation management. When food prices surged in 2023-24, standard strategies proved effective because India could rely on supply-side flexibility, such as releasing stocks, expanding acreage, and allowing market adjustments. This flexibility assumed that grain supply responded solely to food demand. Today, a significant portion of that supply is pre-committed to a secondary derived demand, fuel blending, before any price signal from the food market influences a farmer’s decision-making process. Grain committed to a distillery’s offtake contract is considerably less elastic than grain held in a government buffer stock.

This situation is not attributable to any individual’s fault; it is the inherent friction of two well-intentioned policies simultaneously drawing on a shared input. Recognising this early is precisely what constitutes effective economic management.

The solution

The positive aspect is that this issue is a resolvable design challenge rather than a fundamental flaw in the ethanol programme. India has demonstrated its capability to rapidly transition feedstock sources, as evidenced by its shift from sugarcane dependency to grain within a few years. The same institutional capacity should now be directed towards second-generation ethanol, utilising agricultural residue, crop stubble (currently burned rather than utilised), and dedicated non-food energy crops cultivated on marginal land unsuitable for grain production.

A moderate, time-limited increase in incentives for second-generation ethanol capacity, combined with a ceiling on grain-feedstock that is relaxed only as residue-based capacity becomes operational, would enable the blending target to increase without a corresponding rise in food-grain dependency.

The second component involves sequencing rather than retrenchment: a contingency mechanism that temporarily relaxes grain-based ethanol procurement during years identified as El Niño risk, similar to India’s current management of export bans and buffer-stock releases. This approach incurs minimal costs in typical years and provides substantial insurance during critical periods.

India does not need to choose between fuel production and food security. It must complete the diversification process it is already equipped to implement, but at a pace faster than the next El Niño event. By optimising sequencing, the 20 per cent blending target ceases to be a latent vulnerability and becomes what it was always meant to be: a sustainable advancement on both fronts.

Bidisha Bhattacharya is ThePrint Consulting Editor (Economics) and an Associate Fellow, Chintan Research Foundation. She tweets @Bidishabh. Views are personal.

(Edited by Saptak Datta)