The Reserve Bank of India’s latest proposals on non-banking financial companies, or NBFCs, mark an important shift in thinking at the RBI. They attempt to align regulation with risk by shrinking the scope of regulation at the bottom and expanding supervision at the top.

However, the scale of this change is more modest than it appears. It stops short of confronting a more fundamental question: Why regulate non-deposit-taking NBFCs at all?

The question matters because NBFCs are central to India’s credit architecture. A disproportionate share of riskier, small-ticket, and last-mile lending—whether to MSMEs, informal households, or first-time borrowers—happens through NBFCs rather than banks.

Firms such as Muthoot Finance, with its gold-backed lending model, or Bajaj Finance, with its consumer durable financing and digital credit products, have demonstrated how NBFCs can expand access to credit. They have innovated on underwriting and distribution in ways that traditional banks have not. Questions of regulation, therefore, have a direct bearing on their ability to scale.

How large is the deregulation, really?

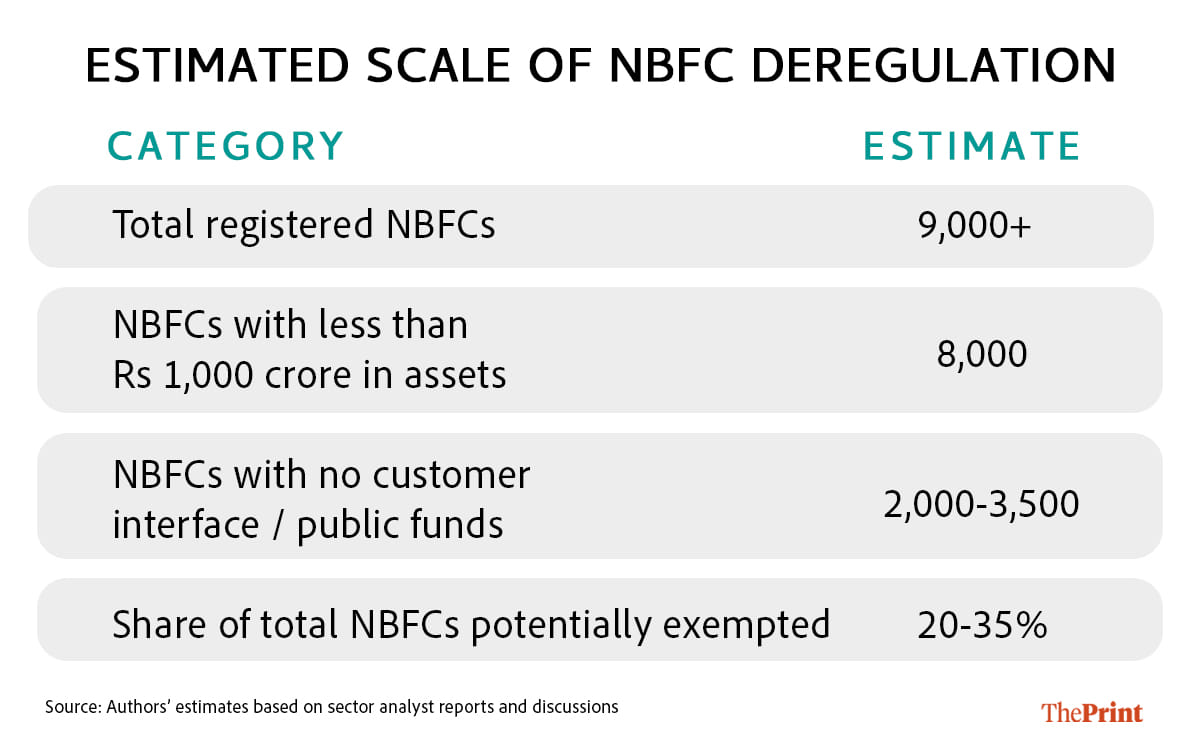

The RBI’s first proposal, effective this month, seeks to exempt NBFCs from registration if they meet three conditions: (i) no customer interface, (ii) no public funds, and (iii) assets below Rs 1,000 crore.

At first glance, this appears to be a significant deregulation. But in practice, the entities that will drop out are a relatively narrow class—primarily, corporate treasury vehicles, group financing arms, and small to medium-sized holding companies. These are, in effect, “invisible” NBFCs. They are internal financing arms within a manufacturing or real estate group that move capital across subsidiaries but have no interaction with external borrowers or depositors. Equating these invisible NBFCs with companies such as Muthoot Finance or Mahindra Finance obscures a basic distinction in the system. These entities do not lend to the public or raise funds from it. Exempting them is sensible and was long overdue.

A large number of small NBFCs are, in fact, customer-facing. Consider a small NBFC financing second-hand commercial vehicles or tractors in a district market, or one providing small-ticket loans to local businesses. These firms may have assets well below Rs 1,000 crore, but they interact directly with borrowers. They continue to fall within the RBI’s current regulatory purview.

The scale of the recent deregulation can be understood through a rough estimate of the distribution of NBFCs in India.

Even at the upper end of estimates, the proposal would remove only about a third of NBFCs from the regulatory net. More importantly, these entities account for a negligible share of total assets and systemic risk. In other words, the reform reduces the number of regulated entities, but does not materially change the distribution of risk within the system.

The current proposal retains an asset threshold of Rs 1,000 crore for exemption. Yet, there is no clear first-principles justification for this. If an entity does not intermediate funds between savers and borrowers, the case for prudential regulation is weak, unless it is systemically important (which we deal with later).

This suggests that the RBI has recognised the problem of overbreadth, but has only partially addressed it.

Also read: Why Tesla, Mercedes and BMW are all playing by China’s rules now

Expanding the list of systemically important NBFCs

The RBI’s second proposal—announced earlier this month in its Statement on Developmental and Regulatory Policies—moves in the opposite direction. It proposes tightening the regulation of large NBFCs.

Currently, the RBI’s regulatory framework classifies NBFCs into four layers—Base, Middle, Upper and Top—on the basis of their assets size and the risk embedded in their business models. NBFCs in the higher layers are subject to stricter regulation compared to their counterparts in the lower layers.

The Upper Layer consists of a small set of NBFCs identified by the RBI using a combination of size, interconnectedness, complexity, and other qualitative factors. Earlier this month, the RBI proposed replacing this with a clearer rule: any NBFC with assets exceeding Rs 1 lakh crore would automatically be classified in the Upper Layer.

This has two clear advantages. First, it enhances predictability and reduces discretion. A rule-based threshold is easier to understand than a composite scoring model. Second, it aligns regulatory intensity with scale, which is a reasonable proxy—though not a perfect one—for systemic importance.

While the move toward a rule-based threshold is welcome, the choice of a fixed asset size raises concerns. In an economy growing at 6 per cent per year in real terms—and significantly faster in nominal terms—balance sheets expand rapidly. Over time, more NBFCs will cross the Rs 1 lakh crore threshold, not necessarily because they have become more systemically risky, but because the economy itself has grown. This creates two problems. First, the Upper Layer may expand mechanically over time, diluting its purpose as a category of exceptional regulatory intensity. Second, a static threshold does not capture other dimensions of risk—dominance in certain segments of lending (such as lending to transport operators or home finance), funding structure, interconnectedness, or liability profile—which may be more relevant for financial stability.

At present, the Upper Layer consists of around 15 NBFCs. Based on available balance sheet data, we estimate the number of NBFCs with assets exceeding Rs 1 lakh crore to be in the range of 12 to 20. This implies that the proposed rule may modestly expand the Upper Layer. The change is hardly transformative.

A more radical possibility

Taken together, the two proposals point toward a broader rethinking of NBFC regulation within the RBI—but stop short of fully embracing it.

If regulatory capacity is limited, the objective cannot be to supervise thousands of entities with equal intensity. Today, nearly 95 per cent of NBFCs sit in the Base Layer, while systemic risk is concentrated in a few hundred firms, and more narrowly in a few dozen. The recommendations only modestly reduce the number of firms in the Base Layer and modestly increase the number in the Upper Layer.

A first principles-based, coherent approach to regulation warrants some radical thinking.

First, India must deregulate all NBFCs below a defined threshold, based not just on asset size but also on funding profile and interconnectedness. In effect, a large share of small, non-deposit-taking NBFCs would fall outside routine prudential regulation altogether.

Second, the focus should be on the prudential regulation of systemically relevant entities, the identification of which must be based on scale—as the RBI has rightly done—but also their interconnectedness. Such an approach would align the regulatory perimeter with actual risk, rather than formal classification.

Also read: Why belief remains high among Indian Americans

Regulating less but better

A common objection to deregulating small NBFCs is consumer protection, as many of these entities interact with retail borrowers, often in less formal credit markets.

However, the RBI’s comparative advantage lies in prudential supervision, not policing retail conduct across thousands of geographically dispersed lenders. Indeed, the RBI-registered tag aggravates moral hazard by confering on thousands of small NBFCs a halo of RBI protection, while enjoying considerable leeway in the absence of actual supervision. Prudential regulation of such NBFCs is a blunt instrument for addressing consumer harm.

A more effective approach would be to rely on horizontal consumer protection laws and enforcement mechanisms, which are better suited to dealing with issues such as misselling, coercive recovery practices, and unfair contract terms. Classic examples of these are the US-based Consumer Protection Financial Board or the Financial Redress Agency recommended by the Financial Sector Legislative Reforms Commission.

The RBI’s proposals on NBFC regulation over the last five years have been largely in the right direction. The recent proposals are also important steps toward a more rational regulatory framework. They recognise that not all financial entities pose equal risks, and that regulatory resources must be prioritised.

But incrementalism has its limits. In a system where risk is concentrated in a handful of large institutions, the case for regulating thousands of small, non-systemic entities is not obvious. If a financial firm does not raise money from the public, the argument for regulating it as part of the financial system is even less clear. Financial firms exist along a spectrum—from small and local to systemically important. The real challenge for financial regulation in India is not how to regulate the entire spectrum—but how to regulate less, and do it better.

Bhargavi Zaveri-Shah is the co-founder and CEO of The Professeer. She tweets @bhargavizaveri. Harsh Vardhan is a management consultant and researcher based in Mumbai. Views are personal.

(Edited by Prasanna Bachchhav)