The Reserve Bank of India’s Monetary Policy Committee (MPC) has been reconstituted with new external members appointed by the central government. The upcoming MPC meeting will be keenly watched for the new members’ views on policy rate and stance.

Monetary Policy Committee: the specifics

The Reserve Bank of India Act was amended in 2016 to provide for a flexible inflation targeting framework in the country. The amendment also provided for a statutory framework for a Monetary Policy Committee to make decisions about the policy rate to achieve the inflation target. As per the provisions of the amended Act, the MPC consists of three internal and three external members. The internal members are the Governor of the RBI as the chairperson, the deputy governor in-charge of monetary policy and one officer of the RBI to be nominated by the Central Board of the RBI.

The three external members are to be appointed by the government. The law requires that the external members should have knowledge and experience in the field of economics, banking or finance or monetary policy. The external members are appointed for a term of 4 years, with no provision for reappointment.

Also read: US Fed’s rate cut is likely good news for India. It may also help temper RBI’s stance

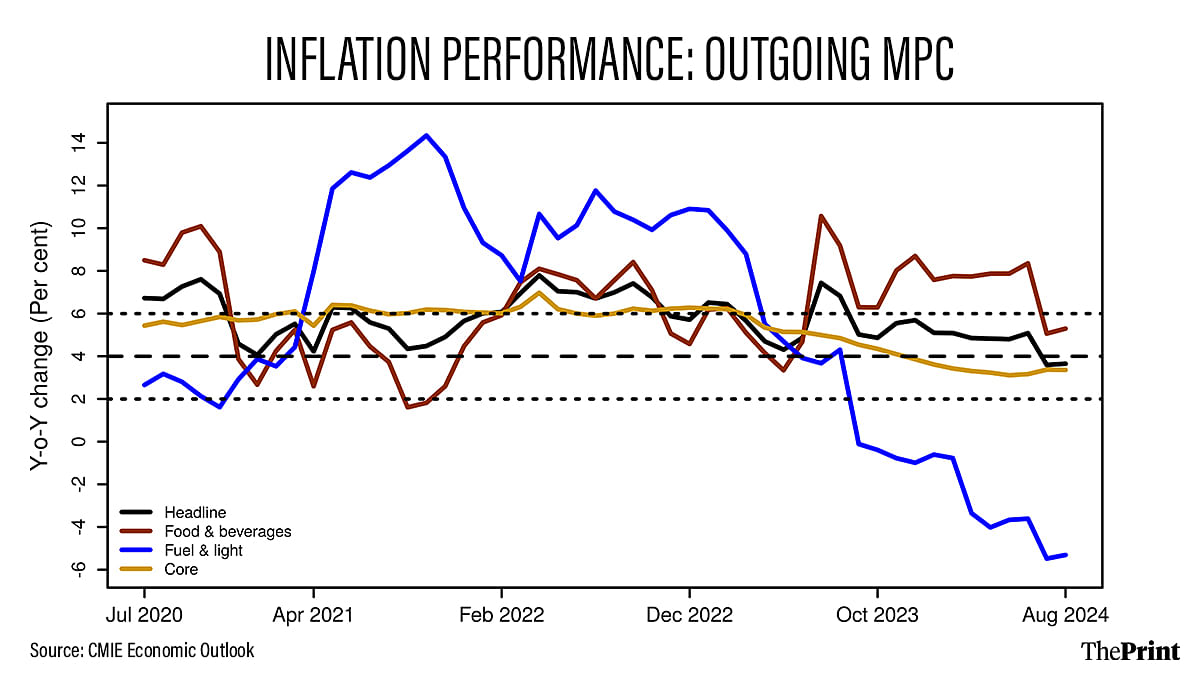

Inflation performance during the tenure of the outgoing MPC

How has the outgoing MPC fared in achieving the inflation target? This was the second MPC since the inception of the inflation targeting framework. It was constituted in October 2020. It first met on 9 October, 2020, and the last meeting was on 8 August, 2024. During its tenure, the economy was subject to multiple shocks.

The first few months of the second MPC was marred by inflation breaching the upper threshold of 6 percent due to the Covid pandemic related disruptions. After a brief moderation in 2021, inflation rebounded in 2022, due to rise in global commodity prices in the aftermath of the Russia-Ukraine conflict.

During the tenure of the second MPC, the RBI officially could not achieve its inflation target. According to the RBI Act, the RBI is deemed to have failed in its inflation targeting objective, if the headline CPI inflation falls below 2 percent or exceeds 6 percent for three consecutive quarters. This condition materialised in 2022, when inflation breached the upper threshold of 6 percent for three quarters from January to September 2022.

The elevated levels of food, fuel and core inflation kept inflation elevated in 2022. In 2023, inflation moderated due to easing of fuel prices and core inflation. It is only in the last two months that inflation eased below the 4 percent mark.

Diversity of opinion & dissent

One of the key strengths of a committee-based monetary policy process is that it brings diversity of views and perspectives in the decision-making process. In particular, the external members of the MPC are expected to bring diverse opinions to the table, thus enhancing the decision-making process.

In the MPC setting, the decision is made on the basis of votes by the members of the MPC. Members can dissent against the resolution. The dissent can be on the policy rate as well as on the stance. The first instance of dissent on the policy rate in the MPC with outgoing external members happened on 30 September, 2022.

On the stance, there have been instances of reservation as well as outright dissent. In the last two meetings, the two external members—Prof Jayanth R. Varma and Dr Ashima Goyal—voted against the unchanged policy rate. They were in favour of a cut in the policy rate. They also voted against the withdrawal of accommodation stance and instead voted to change the stance to neutral. The dissenting members contented that growth is below potential and a sustained high real interest could dampen growth with a lag.

There needs to be greater deliberations on the growth-inflation trade-off, on India’s potential growth, and the trajectory of real interest rate and when it could become a dampener to growth. Hopefully, there would be more discussions and debate on these nuanced issues in the new MPC.

What has changed since the last MPC?

Globally, major central banks have commenced their rate cutting cycle. In addition to the US Federal Reserve and the European Central Bank (ECB), Bank of Canada, Swiss National Bank, Sweden’s Riksbank and the Reserve Bank of New Zealand, to name a few, have also announced policy rate cuts.

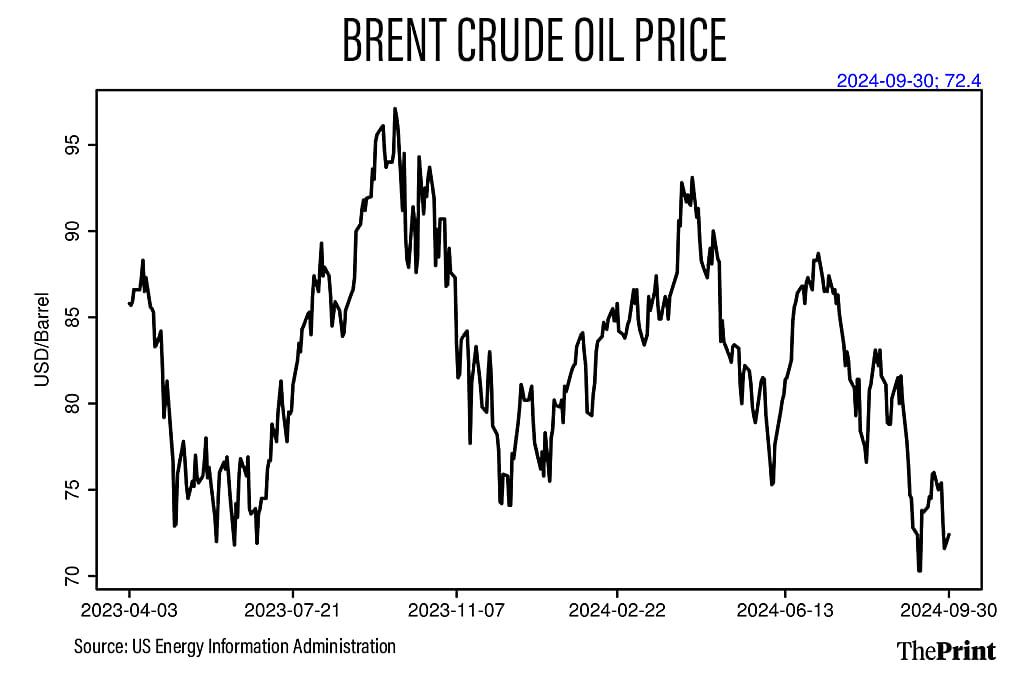

In addition to the rate cuts by global central banks, two significant developments will likely shape the deliberations of the new MPC. One, crude oil prices have witnessed a decline in September to around USD 70-73 a barrel. Stronger supply outlook and weak global demand as well as the escalation of the Iran-Israel conflict are likely to keep the crude oil price volatile. Trajectory of global crude oil prices is a critical input in the RBI’s inflation outlook.

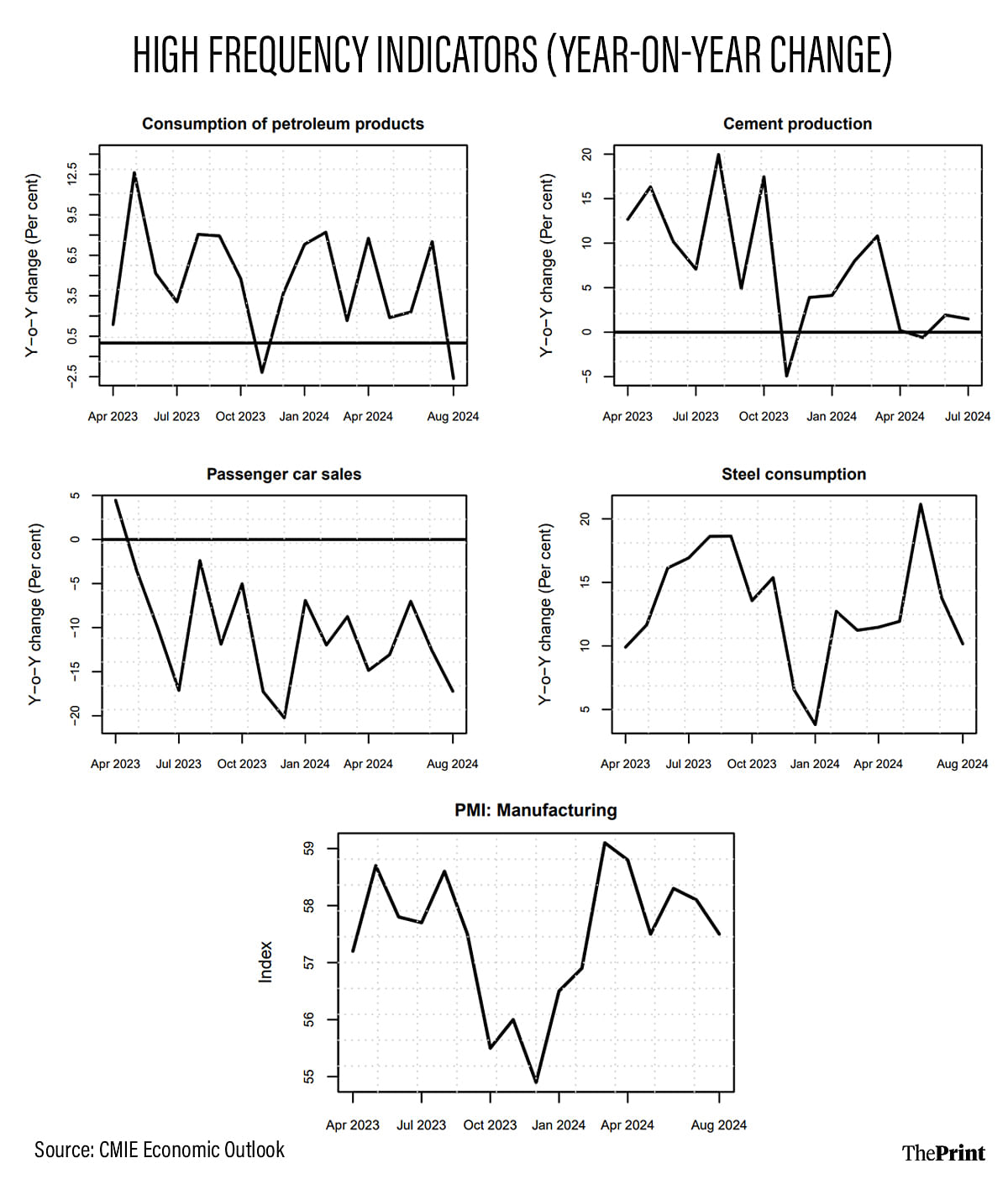

Second, there are signs of slowdown in various high frequency indicators, pointing to softer growth. Passenger car sales, cement production, steel consumption and consumption of petroleum products show weaker growth in recent months. The Manufacturing Sector PMI—a key gauge of manufacturing sector activity—has been ebbing since June due to lower growth in output and new orders.

The key drivers of growth in bank credit—personal loans and services—also witnessed moderation in August. While the overall non-food bank credit growth was roughly unchanged at 15 percent, excluding the impact of the HDFC bank merger, personal loan growth moderated to 16.9 percent in August as compared to 18.3 percent a year ago. The slowdown in personal loans is largely due to decline in credit card debt.

Credit to services witnessed a sharper slide to 15.6 percent from 21 percent a year ago, due to lower credit to the NBFC segment. While part of the slowdown can be due to regulatory tightening measures announced by the RBI last year, the easing of credit growth is perhaps also a signal of weak urban discretionary demand.

The outlook on inflation and growth amid an uncertain global environment and changing macro landscape will be keenly watched in the next week’s reconstituted MPC meeting.

Radhika Pandey is associate professor at National Institute of Public Finance and Policy (NIPFP).

Views are personal.