The coronavirus pandemic has raised deficit spending to new heights. Federal debt held by the public is expected to reach 100% of gross domestic product this year, effectively returning to the levels of World War II.

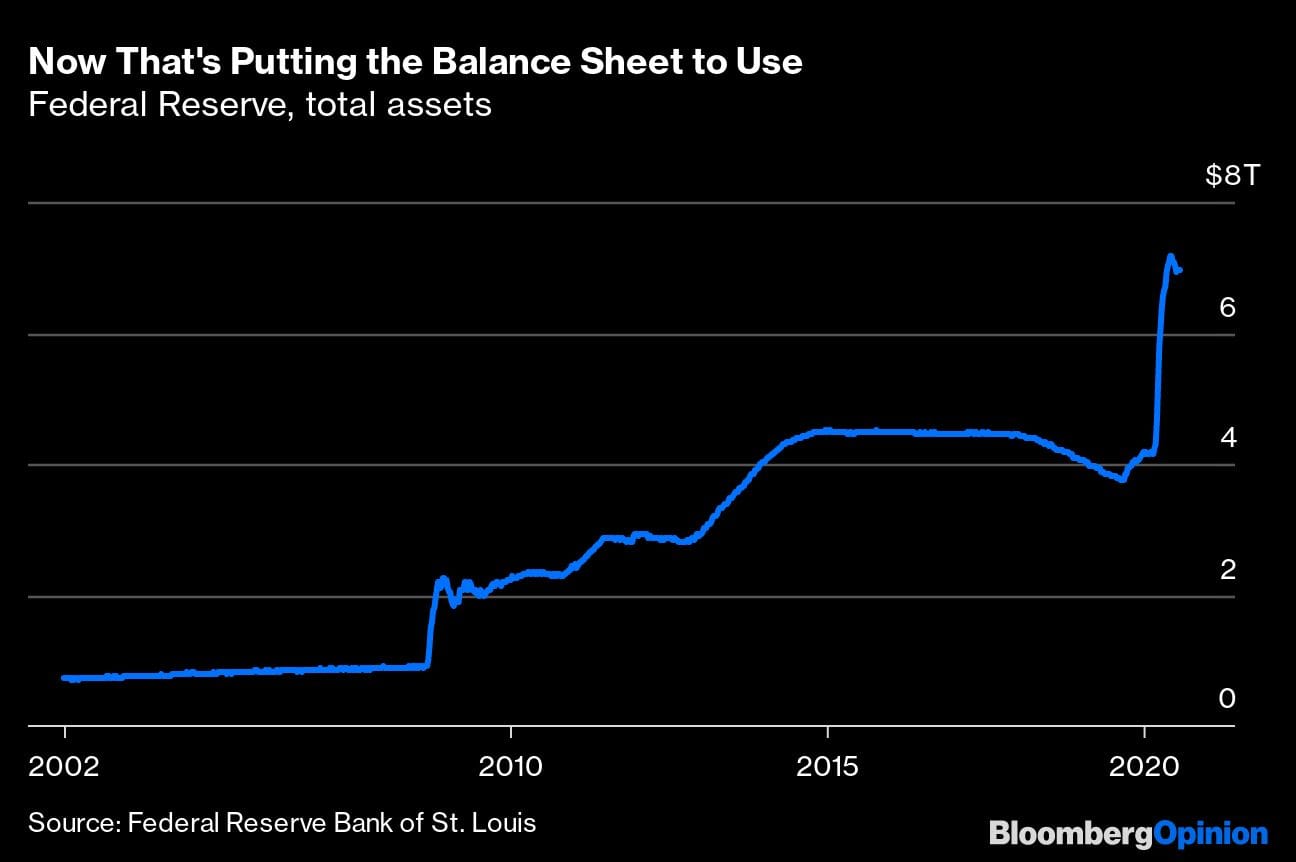

The Federal Reserve, meanwhile, has also taken unprecedented action, increasing its total assets from about $4 trillion at the start of the pandemic to about $7 trillion now:

The big question is when, if ever, this aggressive government action starts to incur negative consequences, such as rapid inflation. Macroeconomists should be investigating this question vigorously. But so far, interest in the question has seemed strangely muted among mainstream academics.

Before the financial crisis of 2008, the dominant academic model of the business cycle held that there was a tradeoff between inflation and unemployment — a new version of what’s known in economics as the Philips Curve. By managing interest rates, mainstream theorists argued, the central bank would navigate serenely between the rocks of inflation and the shoals of unemployment. There was not much room for government debt in that model.

The 2008 recession seemed like it might present a huge challenge for this paradigm, but most macroeconomists met the challenge by simply patching up the old models. They shoehorned in a financial sector, and allowed that when nominal interest rates approached zero, fiscal stimulus along with quantitative easing would have to be brought in.

But that still left the question of what the limits of stimulus and QE would be. Mainstream economists realized that because the government can use monetary policy to lower interest rates and even finance government borrowing directly, there would never be a real risk of sovereign default; if private investors stopped buying Treasuries and rates started to rise, the Fed could pick up the slack. The only real constraint on government action was the possibility of inflation, if the Fed created too much money.

But when would inflation kick in? Economists’ only answer was, basically, that it would happen at some point. Some economists fretted that QE was about to cause rapid inflation, even writing an open letter to former Fed chairman Ben Bernanke warning him to stop QE. But Bernanke didn’t stop, and inflation never came. The Bank of Japan engaged in an even more vigorous program, buying up an appreciable fraction of the country’s stock market. But inflation never consistently reached the bank’s 2% target.

The failure of inflation to materialize in response to enormous fiscal and monetary stimulus in the 2010s should have prompted vigorous activity among academics to try to figure out why. But oddly, it didn’t. A few scholars suggested that low interest rates were actually deflationary, but this idea never caught on. Most macroeconomists, if they bothered to address the question at all, simply assumed that at some point inflation would pick up, and that developed countries simply hadn’t reached that point yet. So far, the coronavirus pandemic looks like a repeat of the financial crisis in this respect; despite unprecedented deficits and monetary expansion, markets expect inflation to be below target for the next decade.

But inflation undeniably happens sometimes, in some places. Venezuela and Lebanon have both recently experienced hyperinflation, with the former reaching an annual rate of more than 130,000%. The economic consequences are devastating — even worse than a sovereign default. The question is why, and where, and under what conditions hyperinflation happens, and how it can be stopped.

Instead of spinning theories that effectively just say that hyperinflation will happen at some unknown point, macroeconomists could look at countries that do experience hyperinflation, or come close but manage to avert it. They should use these historical and international examples to learn lessons about when and where and why this sort of catastrophe happens, and how it can be prevented. But the seminal work on hyperinflation continues to be economist Thomas Sargent’s 1982 paper “The End of Four Big Inflations.” This paper, in addition to being four decades old, draws all its examples from Central European economies in the aftermath of World War I — very different circumstances than the economies of today.

New work on hyperinflation is urgently needed. One key question is whether runaway inflation happens slowly enough that the government can reverse course in time, or whether it’s instantaneous and catastrophic. Another question is whether direct monetary financing of new government borrowing is a trigger for hyperinflation. A third is whether and how capital flight is involved. A fourth is how the type of government spending changes whether markets expect deficits to be temporary or permanent. There are many other important questions besides these.

If academic macroeconomists continue to largely ignore this question, and focus on the models and ideas and questions that they were working on before coronavirus, it will represent a quiet but enormous failure of the discipline, just as significant as the profession’s inability to see the 2008 crisis coming. With academics AWOL on the question of how much the government can safely spend and how much the central bank can safely print, policy makers, businesspeople and financial market participants will turn to poorly articulated theories, old nostrums, political agitators, gut instincts or the raving of random Twitter users. – Bloomberg

Also read: These are the world’s most miserable and least miserable economies of 2020

I am requesting to our Prime minister & our finance minister to use the land and buildings of the close PSUs at Durgapur and Asansol area of West Bengal. For boost up the economy and generation of employment it is necessary to encourage big private business houses to install morden industry in this unused land.